![]()

Search Market Research Report

Digital Health Market Size, Share Global Analysis Report, 2024 – 2032

Digital Health Market Size, Share, Growth Analysis Report By Component (Services, Software, and Hardware), By Technology (Telehealthcare, mHealth, Healthcare Analytics, Digital Health Systems, E-prescribing Systems, Virtual Care Platforms, Wearable Health Technology, and Remote Patient Monitoring (RPM)), And By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

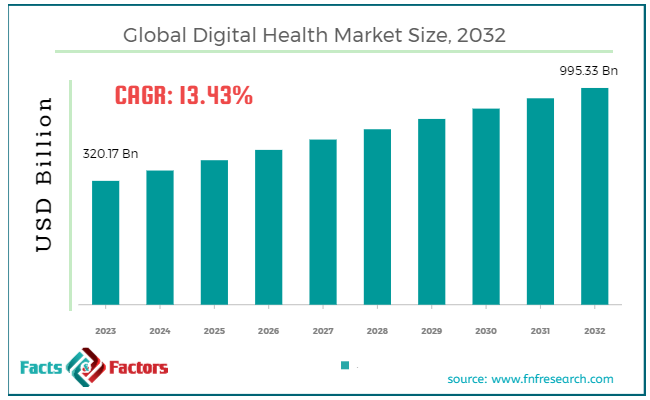

[219+ Pages Report] According to Facts & Factors, the global digital health market size in terms of revenue was valued at around USD 320.17 billion in 2023 and is expected to reach a value of USD 995.33 billion by 2032, growing at a CAGR of roughly 13.43% from 2024 to 2032. The global digital health market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

Digital health encompasses the use of digital technologies to improve health, healthcare services, and wellness. It integrates a wide array of tools such as electronic health records (EHRs), telehealth, mobile health applications, wearable devices, and artificial intelligence to enhance the efficiency and personalization of healthcare. The objective is to make healthcare delivery more accurate, efficient, and customized to individual patient needs.

The significance of digital health has been magnified by the increasing demand for more accessible and efficient healthcare solutions, rising healthcare costs, and the technological advancements that enable remote and real-time patient monitoring.

Digital health applications range from telemedicine services, which allow doctors to consult with patients remotely, to fitness trackers that monitor an individual's physical activity and vital signs in real-time. This field also includes more sophisticated technologies like genomics and personalized medicine, where treatments are tailored to the genetic makeup of individuals.

As healthcare systems around the world shift towards more patient-centered services, digital health stands as a crucial element in this transformation, aiming to make healthcare more accessible, cost-effective, and tailored to individual needs. The market's potential continues to grow with ongoing innovations and the integration of more advanced technologies, suggesting a promising future for the expansion of digital health solutions.

Key Highlights

- The digital health market has registered a CAGR of 13.43% during the forecast period.

- In terms of revenue, the global digital health market was estimated at roughly USD 320.17 billion in 2023 and is predicted to attain a value of USD 995.33 billion by 2032.

- The global digital health market growth is fueled by the rising adoption of telehealth, technological advancements, and increasing healthcare costs. Government initiatives and a shift towards personalized medicine further boost this expansion, driving rapid development in the sector.

- Based on the component, the services segment is growing at a high rate and is projected to dominate the global market.

- Based on the technology, the tele-healthcare segment is projected to swipe the largest market share of around 43.2% in 2023.

- By region, the North American region will dominate the global digital health market.

Growth Drivers:

- Cost Reduction: Soaring healthcare costs are a major concern. Digital health offers solutions like remote patient monitoring and preventative care, potentially reducing overall healthcare expenditure.

- Convenience Craving: Consumers today yearn for convenient healthcare solutions. Digital health delivers with features like telehealth consultations, appointment scheduling via mobile apps, and readily accessible health information.

- Mobile Tech Boom: The widespread use of smartphones and tablets creates a perfect platform for digital health tools and applications, making them readily accessible to a vast audience.

- Preventive Care Focus: Digital health empowers individuals to take a more proactive approach to their health. Wearables, self-monitoring tools, and personalized wellness programs all contribute to preventive care.

Restraints:

- Data Privacy & Security: Concerns about data privacy and security pose a significant challenge. Ensuring the confidentiality and security of sensitive health information is crucial for building trust with patients.

- Digital Divide: Unequal access to technology creates a "digital divide" that can limit access to digital health tools for certain populations, particularly those in rural areas or with limited resources.

- Regulatory Hurdles: The rapid evolution of digital health solutions necessitates robust regulatory frameworks to ensure the quality, safety, and efficacy of these tools. Regulatory processes need to adapt to keep pace with innovation.

Opportunities:

- Chronic Disease Management: Digital health tools offer immense potential for managing chronic conditions like diabetes or heart disease. Remote monitoring, medication management apps, and personalized support programs can significantly improve patient outcomes.

- Mental Health Care: Digital health solutions can address the growing need for accessible and affordable mental healthcare. Teletherapy platforms provide convenient access to mental health professionals, while online support groups and cognitive behavioral therapy apps offer valuable resources for patients.

- AI Integration: Artificial intelligence (AI) has the potential to revolutionize digital health by enabling advanced data analysis, personalized treatment plans, and even chatbots for initial consultations or symptom management.

Challenges:

- Physician Integration: Encouraging widespread adoption of digital health tools among healthcare providers is crucial for successful integration into existing healthcare systems. This may require addressing concerns about workflow disruption and ensuring proper training on using these tools effectively.

- Interoperability: The lack of interoperability between different digital health platforms can create silos of data, hindering information sharing and a holistic view of a patient's health. Standardized data formats and open platforms are essential for seamless integration.

- Reimbursement Models: Developing sustainable reimbursement models for digital health services is crucial for ensuring their long-term viability. Governments and healthcare payers need to adapt their models to incentivize the use of these innovative solutions.

Digital Health Market: Segmentation Analysis

The global digital health market is segmented based on component, technology, and region.

By Component Insights:

The digital health market includes three primary components: services, software, and hardware.

- Services: The services segment has emerged as the linchpin of the digital health market, accounting for around 47.3% of the market share in 2023. This segment's vitality stems from the essential role that services such as installation, ongoing maintenance, and training play in the deployment of digital health solutions. As technologies advance, they often become more complex, necessitating enhanced support services to ensure they are used effectively. Healthcare providers rely heavily on these services to streamline their operations and optimize the use of digital health technologies. This dependency is forecasted to grow, driven by the increasing sophistication of digital health solutions which require regular updates and skilled handling to maintain their efficacy and security.

- Software: Software forms the backbone of digital health, enabling the functionalities needed for sophisticated healthcare delivery. This segment accounted for around 16.5% of the total revenue share in 2023. This includes everything from patient management systems to sophisticated diagnostic tools. As digital health technologies evolve, software solutions are continually updated to incorporate artificial intelligence, machine learning, and big data analytics. These enhancements facilitate more accurate diagnostics, improved patient tracking, and personalized treatment plans, making the software segment a critical area of growth within the digital health ecosystem.

- Hardware: Hardware in digital health includes wearable devices, monitors, and other physical devices that are integral to collecting real-time health data. The importance of hardware persists, particularly as wearable technology becomes more advanced and integrated into patient care. These devices are crucial for continuous monitoring, offering insights into patient health patterns and providing data that can pre-emptively alert healthcare providers to potential health issues.

By Technology Insights:

Based on Technology, the digital health market is segmented into telehealthcare, mhealth, healthcare analytics, digital health systems, e-prescribing systems, virtual care platforms, wearable health technology, and remote patient monitoring (RPM).

- Telehealthcare: The tele-healthcare segment witnessed the highest growth globally, accounting for 43.2% of the segment's revenue in 2023. This segment's surge is primarily fueled by its ability to facilitate remote patient engagement and care, an increasingly vital component in modern healthcare. Telehealthcare stands out for its ability to manage vast amounts of healthcare data securely and in real-time, making it indispensable for population health management and emergency responsiveness. The adoption of telehealthcare is set to soar, driven by its proven effectiveness in managing chronic diseases and providing care that transcends geographical barriers.

- mHealth: Mobile health, or mHealth, harnesses the power of mobile devices to provide health services and information, making healthcare accessible from anywhere at any time. This segment is crucial for delivering personalized patient support and for expanding healthcare access to underserved areas, significantly enhancing patient engagement and compliance with treatment protocols.

- Healthcare Analytics: This technology processes and analyses health data from various sources to derive actionable insights. The sophistication of healthcare analytics allows for predictive modelling and risk assessment, vastly improving the quality and outcomes of healthcare services. As data becomes more central to healthcare, the demand for robust analytics tools continues to grow, highlighting this segment's pivotal role in future healthcare strategies.

- Digital Health Systems: These systems integrate various healthcare technologies to facilitate the efficient exchange of health information. They support the operational aspects of healthcare facilities, improving care coordination and patient outcomes.

- E-Prescribing Systems: This technology allows doctors to send prescriptions directly to pharmacies electronically, reducing the risk of prescription errors and improving the speed of patient service. E-prescribing is becoming increasingly popular due to its efficiency and the enhanced safety it brings to the medication dispensing process.

- Virtual Care Platforms: These platforms provide a digital space where healthcare providers can interact with patients through video calls, messaging, and other online communication tools. Virtual care platforms are essential for continuous patient care and support, especially for patients in remote or underserved regions.

- Wearable Health Technology: This segment includes advanced devices like heart rate sensors, fitness trackers, and sleep monitors that provide real-time insights into a person’s health status. Wearables are critical for proactive health monitoring and have become particularly popular for their ability to track and encourage healthier lifestyle choices.

- Remote Patient Monitoring (RPM): RPM systems are designed to monitor patients' health data while they are at home, using devices that can send data back to healthcare providers in real-time. This technology is vital for managing chronic conditions and elderly care, allowing for timely interventions before acute events occur.

Recent Developments:

- In July 2023, the Peterson Center on Healthcare unveiled the Peterson Health Technology Institute (PHTI). This new nonprofit organization is dedicated to independently evaluating innovative healthcare technologies with the aim of enhancing health outcomes and reducing costs.

- In May 2022, the Organization for the Review of Care and Health Applications (ORCHA) announced its participation in a new U.S. framework for evaluating health technologies. This initiative, which includes mobile apps and web-based tools used by healthcare providers and consumers, is led by the American College of Physicians (ACP) and the American Telemedicine Association (ATA) in collaboration with ORCHA.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 320.17 Billion |

Projected Market Size in 2032 |

USD 995.33 Billion |

CAGR Growth Rate |

13.43% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

AdvancedMD Inc., AirStrip Technologies, Allscripts Healthcare Inc, Apple Inc., Athenahealth Inc., BioTelemetry Inc, Boston Scientific Corporation, Cerner Corporation (Oracle), Cisco Systems, eClinicalWorks, Epic Systems Corporation, FUJIFILM Holdings Corporation, General Electric Company, Honeywell International Inc, iHealth Lab Inc, Koninklijke Philips N.V., McKesson Corporation, Medtronic, Samsung Electronics Co. Ltd., Siemens Healthcare GmbH, Validic, Vodafone Group, and others., and Others. |

Key Segment |

By Component, By Technology, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Digital Health Market: Regional Analysis

In North America, the digital health market is highly advanced, characterized by sophisticated healthcare infrastructures and high levels of technology adoption, particularly in the United States and Canada. The region's market dynamics are influenced by comprehensive regulatory support and substantial investments in healthcare innovation, which facilitate widespread use of electronic health records (EHRs), telehealth services, and mobile health applications.

Initiatives such as Medicare's support for telehealth and remote patient monitoring systems have further bolstered the market. With a compound annual growth rate (CAGR) of around 12.9%, North America continues to lead in terms of market maturity and technological advancements, driven by ongoing research, development efforts, and a strong ecosystem of health tech startups.

North American consumers enjoy a comfortable level of disposable income, estimated at around USD 43,232 per capita (World Bank, 2023). This economic strength allows for greater investment in innovative healthcare solutions. The region also boasts a highly tech-savvy population with a smartphone penetration rate exceeding 80% and rising internet connectivity. This creates a fertile ground for the widespread adoption of mobile health apps, telehealth consultations, and wearable devices.

Europe's digital health market is robust, shaped by a strong regulatory framework that emphasizes data protection and patient privacy, particularly under the General Data Protection Regulation (GDPR). Europe region has captured a market share of around 34.87% in 2023. This regulatory environment challenges and guides the development of digital health applications across the continent. European countries like Germany, the UK, France, and the Nordic countries are at the forefront, leveraging digital health to enhance healthcare delivery and patient management.

The European market is also seeing significant growth in telemedicine, driven by government initiatives aimed at integrating digital health more comprehensively into public healthcare systems. With a CAGR of approximately 12.14%, Europe demonstrates strong growth potential, underscored by an increasing focus on cross-border health data exchange and digital health innovation.

The Asia-Pacific region is witnessing the fastest growth in the digital health market, with a CAGR exceeding 13.92%. This surge is fueled by rapid technological adoption, increasing healthcare expenditures, and supportive government policies aimed at enhancing healthcare accessibility.

Major economies like China and India are aggressively pushing digital health initiatives as part of broader healthcare reform efforts. Japan and Australia are investing in digital solutions to manage aging populations and improve rural healthcare access, respectively. The region’s large, diverse population and growing middle class provide a fertile ground for digital health technologies, making it a global leader in terms of growth dynamics.

Latin America is experiencing gradual growth in the digital health sector, with Brazil and Mexico leading the way. The region benefits from increasing internet penetration and mobile device usage, which are critical in promoting the adoption of telemedicine and mobile health applications. Despite facing economic and infrastructural challenges, the region shows potential with a CAGR of 8.10%. Efforts to integrate digital health tools into the existing healthcare infrastructure are underway, aiming to improve healthcare access and quality across the region.

The Middle East and Africa (MEA) region, while still developing in terms of digital health infrastructure, shows promising growth, especially in Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia. These countries are incorporating digital health as a key component of their national health strategies, such as Saudi Arabia's Vision 2030.

The MEA region's growth is estimated at a CAGR of 9.11%, driven by investments in smart health technologies and digital transformation projects aimed at enhancing healthcare delivery and expanding access. Challenges remain, however, particularly in terms of regulatory frameworks and the need for increased training and awareness among healthcare providers.

Digital Health Market: List of Key Players

Some of the main competitors dominating the global digital health market include;

- AdvancedMD Inc.

- AirStrip Technologies

- Allscripts Healthcare, Inc

- Apple Inc.

- Athenahealth Inc.

- BioTelemetry Inc

- Boston Scientific Corporation

- Cerner Corporation (Oracle)

- Cisco Systems

- eClinicalWorks

- Epic Systems Corporation

- FUJIFILM Holdings Corporation

- General Electric Company

- Honeywell International Inc

- iHealth Lab Inc

- Koninklijke Philips N.V.

- McKesson Corporation

- Medtronic

- Samsung Electronics Co. Ltd.

- Siemens Healthcare GmbH

- Validic

- Vodafone Group

The global digital health market is segmented as follows:

By Component

- Services

- Software

- Hardware

By Technology

- Telehealthcare

- Telehealth

- Telecare

- mHealth

- Apps

- Healthcare Analytics

- Digital Health Systems

- E-prescribing Systems

- Virtual Care Platforms

- Wearable Health Technology

- Heart Rate Sensors

- Fitness Trackers

- Sleep Monitors

- BP Monitors

- Cardiac & Glucose Monitors

- Others

- Remote Patient Monitoring (RPM)

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- AdvancedMD Inc.

- AirStrip Technologies

- Allscripts Healthcare, Inc

- Apple Inc.

- Athenahealth Inc.

- BioTelemetry Inc

- Boston Scientific Corporation

- Cerner Corporation (Oracle)

- Cisco Systems

- eClinicalWorks

- Epic Systems Corporation

- FUJIFILM Holdings Corporation

- General Electric Company

- Honeywell International Inc

- iHealth Lab Inc

- Koninklijke Philips N.V.

- McKesson Corporation

- Medtronic

- Samsung Electronics Co. Ltd.

- Siemens Healthcare GmbH

- Validic

- Vodafone Group

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors