![]()

Search Market Research Report

Messaging Platform Market Size, Share Global Analysis Report, 2026-2034

Messaging Platform Market Size, Share, Growth Analysis Report By Type (Consumer Messaging Apps, Enterprise Messaging Platforms, Business Messaging Solutions, RCS & A2P Messaging), By Deployment (Cloud-based, On-premise), By End-User (Individual Consumers, Enterprises & SMBs, Government & Public Sector), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

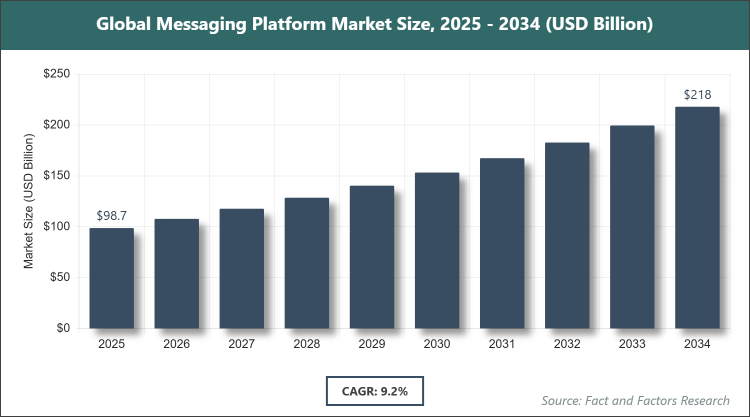

[241+ Pages Report] According to Facts & Factors, the global Messaging Platform market size was estimated at USD 98.7 billion in 2025 and is expected to reach USD 218.4 billion by the end of 2034. The Messaging Platform industry is anticipated to grow by a CAGR of 9.2% between 2026 and 2034. The Messaging Platform Market is driven by explosive growth in mobile internet penetration, enterprise digital transformation, and convergence of personal & business communication channels.

Market Overview

Market Overview

Messaging platforms encompass a broad ecosystem of software applications and infrastructure that enable real-time text, voice, image, video, file sharing, and increasingly rich interactive communication between individuals, groups, businesses, and automated systems. These platforms range from consumer-oriented mobile-first chat applications to enterprise-grade secure collaboration tools and business-to-consumer conversational commerce channels. Modern messaging platforms integrate end-to-end encryption, cross-platform compatibility, rich media support, bots & automation, payment capabilities, and API access for third-party integration, serving as the primary communication layer for both personal relationships and professional workflows in an increasingly mobile and always-connected digital economy.

Key Insights

- As per the analysis shared by our research analyst, the global Messaging Platform market is estimated to grow annually at a CAGR of around 9.2% over the forecast period (2026-2034).

- In terms of revenue, the global Messaging Platform market size was valued at around USD 98.7 billion in 2025 and is projected to reach USD 218.4 billion by 2034.

- The market is driven by rapid enterprise adoption of secure internal & customer messaging and convergence of personal & business communication.

- Based on the type, the consumer messaging apps segment dominated the market with a share of 58%, as it captures the massive daily active user base and generates substantial advertising & in-app purchase revenue.

- Based on the deployment, the cloud-based segment dominated with a share of 76%, due to scalability, lower upfront costs, rapid feature updates, and seamless integration with other SaaS tools.

- Based on the end-user, the enterprises & SMBs segment dominated with a share of 44%, attributed to the accelerating shift from email & legacy UCaaS toward modern, secure, context-rich messaging platforms.

- Asia Pacific dominated the global market with a share of 47%, owing to the highest concentration of mobile-first users, explosive super-app growth, and aggressive RCS rollout by telecom operators.

Growth Drivers

- Enterprise Shift Toward Modern Collaboration & Customer Engagement

Organizations across all sizes are replacing fragmented legacy communication tools (email + legacy UC + file shares) with unified messaging-first platforms that offer real-time presence, threaded conversations, file collaboration, bots, and integration with CRM, ERP, and productivity suites. This shift is accelerated by hybrid/remote work permanence and the demand for secure, compliant internal communication.

Simultaneously, businesses are adopting messaging as the primary customer engagement channel, especially through RCS business messaging, WhatsApp Business API, Apple Messages for Business, and in-app chat because response rates and conversion are significantly higher than email or traditional SMS, driving measurable ROI in marketing, support, and transactional use cases.

Restraints

- Fragmentation & Interoperability Barriers

Despite standards efforts (Matrix, RCS), the messaging ecosystem remains highly fragmented with competing protocols, closed gardens (iMessage, WhatsApp, WeChat, Telegram, Signal), and limited cross-platform rich messaging capabilities. This fragmentation creates user fatigue, reduces network effects for new entrants, and complicates enterprise deployment of unified messaging strategies.

Additionally, many large enterprises still face internal resistance to moving away from email due to compliance archiving requirements, e-discovery needs, and user habit inertia, slowing the replacement cycle even when better alternatives exist.

Opportunities

- RCS Business Messaging & A2P 2.0 Monetization Wave

The global rollout of Rich Communication Services (RCS) by mobile operators, combined with branded sender verification, rich cards, carousels, suggested replies, and transaction capabilities, is creating the first truly global, carrier-grade alternative to closed messaging ecosystems for enterprise-to-consumer communication. This opens a multi-billion-dollar opportunity for A2P messaging revenue.

Super-apps and mini-program ecosystems (WeChat, WhatsApp Business, Telegram Mini Apps, Google Business Messages) are evolving into full commerce & service platforms, allowing brands to build entire customer journeys, discovery, engagement, payment, fulfillment inside messaging, significantly increasing lifetime value and reducing reliance on traditional apps or websites.

Challenges

- Privacy, Security & Regulatory Pressure

Messaging platforms are under intense scrutiny from regulators (DMA in the EU, antitrust actions in multiple jurisdictions, data localization laws, lawful interception mandates) while simultaneously being expected to deliver best-in-class end-to-end encryption and metadata protection. Balancing compliance with user privacy expectations remains technically and politically difficult.

Rising sophistication of phishing, business email compromise (BEC) via messaging, account takeover attacks, and AI-generated deepfake scams is forcing platforms to invest heavily in identity verification, fraud detection, and user education, increasing operating costs and occasionally degrading user experience through added friction.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 98.7 Billion |

Projected Market Size in 2034 |

USD 218.4 Billion |

CAGR Growth Rate |

9.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Meta, Tencent, Microsoft, Alphabet, ByteDance, Snap Inc., Telegram, Discord, Slack (Salesforce), Apple, Sinch AB, Twilio Inc., Infobip, Vonage (Ericsson), and Others. |

Key Segment |

By Type, By Deployment, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Messaging Platform market is segmented by type, deployment, end-user, and region.

Based on Type Segment, the Messaging Platform market is divided into consumer messaging apps, enterprise messaging platforms, business messaging solutions, RCS & A2P messaging. The consumer messaging apps segment emerges as the most dominant, holding approximately 58% market share, primarily because it commands the largest daily active user base globally and generates the majority of advertising, in-app purchase, and premium subscription revenue, thereby driving overall market growth through massive scale and network effects. The enterprise messaging platforms segment follows as the second most dominant, with around 22% share, fueled by rapid adoption of secure, compliant team collaboration tools that integrate deeply with productivity and CRM ecosystems, contributing significantly to high-margin recurring SaaS revenue.

Based on Deployment Segment, the Messaging Platform market is divided into cloud-based, on-premise. The cloud-based segment is the most dominant, capturing about 76% of the market, as enterprises overwhelmingly prefer SaaS delivery models for faster deployment, automatic updates, elastic scaling, lower total cost of ownership, and seamless integration with other cloud services, helping to propel the market through accelerated digital transformation. The on-premise segment ranks second, with roughly 24% share, primarily serving highly regulated industries (finance, government, defense) that require complete data sovereignty and custom security controls.

Based on End-User Segment, the Messaging Platform market is divided into individual consumers, enterprises & SMBs, government & public sector. The enterprises & SMBs segment is the most dominant, capturing about 44% of the market, driven by the urgent need for secure internal communication, customer engagement at scale, and workflow automation within messaging interfaces, thereby driving the market through high ARPU SaaS contracts and rapid seat growth. The individual consumers segment ranks second, with roughly 38% share, representing the enormous advertising and monetization potential of daily active users across the dominant consumer apps.

Recent Developments

- In January 2026, WhatsApp Business crossed 200 million monthly transacting users and launched WhatsApp Flows allowing brands to build multi-step interactive customer journeys entirely inside chat.

- In December 2025, Google announced RCS Business Messaging now supports verified senders in 90+ countries and introduced dynamic rich cards with deep linking and payment integration.

- In November 2025, Microsoft Teams introduced native RCS support for consumer phone numbers and advanced compliance archiving for regulated industries.

- In October 2025, Telegram launched Telegram Business a paid tier offering verified badges, automated greetings, quick replies, chat folders, and API access for SMBs.

- In Q3 2025, Meta rolled out end-to-end encrypted WhatsApp Cloud API 2.0 with improved message templates, analytics, and multi-device support for large enterprises.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific is the undisputed leader in messaging platform usage and monetization, home to the world’s largest daily active user bases and the most advanced super-app ecosystems. China dominates this region through WeChat’s unparalleled integration of messaging, payments, mini-programs, official accounts, and lifestyle services, creating a closed-loop digital economy that generates enormous revenue per user and serves as a model for other markets.

North America remains the highest ARPU region for enterprise messaging platforms and continues to set global standards for workplace collaboration tools. The United States leads, with Microsoft Teams, Slack (Salesforce), Google Workspace, and Zoom becoming deeply embedded in corporate workflows and driving substantial SaaS subscription revenue.

Europe exhibits strong growth in both consumer privacy-focused apps (Signal, Threema, Element/Matrix) and enterprise UCaaS platforms, influenced by GDPR and the Digital Markets Act. Germany stands out due to its conservative approach to data protection, strong adoption of on-premise and sovereign cloud solutions, and leadership in secure government & critical infrastructure messaging.

Latin America shows very high organic growth rates in consumer messaging and increasing enterprise adoption, especially in Brazil and Mexico. Brazil leads thanks to massive WhatsApp usage for both personal and business communication, early RCS business messaging adoption, and rapid digitization of SMBs.

The Middle East & Africa region is experiencing rapid catch-up growth driven by mobile-first populations and government digital transformation initiatives. The United Arab Emirates and Saudi Arabia lead in enterprise-grade secure messaging adoption (especially government-to-citizen services), while WhatsApp and Telegram dominate consumer usage across the continent.

Competitive Analysis

The global Messaging Platform market is dominated by players:

- Meta (WhatsApp, Messenger, Instagram DM)

- Tencent (WeChat)

- ByteDance (TikTok, Douyin messaging)

- Microsoft (Teams)

- Alphabet (Google Messages / RCS, Gmail chat)

- Snap Inc. (Snapchat)

- Telegram FZ-LLC

- Discord Inc.

- Slack Technologies (Salesforce)

- Apple (iMessage, Business Chat)

- Sinch AB

- Twilio Inc.

- Infobip

- Vonage (Ericsson)

- And Others.

The global Messaging Platform market is segmented as follows:

By Type

- Consumer Messaging Apps

- Enterprise Messaging Platforms

- Business Messaging Solutions

- RCS & A2P Messaging

By Deployment

- Cloud-based

- On-premise

By End-User

- Individual Consumers

- Enterprises & SMBs

- Government & Public Sector

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Meta (WhatsApp, Messenger, Instagram DM)

- Tencent (WeChat)

- ByteDance (TikTok, Douyin messaging)

- Microsoft (Teams)

- Alphabet (Google Messages / RCS, Gmail chat)

- Snap Inc. (Snapchat)

- Telegram FZ-LLC

- Discord Inc.

- Slack Technologies (Salesforce)

- Apple (iMessage, Business Chat)

- Sinch AB

- Twilio Inc.

- Infobip

- Vonage (Ericsson)

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors