![]()

Search Market Research Report

Food Contact Paper Market Size, Share Global Analysis Report, 2026-2034

Food Contact Paper Market Size, Share, Growth Analysis Report By Type (Kraft Paper, Greaseproof Paper, Glassine Paper, Parchment Paper, and Others), By Application (Fresh Produce, Dry Groceries, Bakery Products, Liquid Food and Drinks, Takeaway and Vending Foods, and Others), By End-User (Food Service Outlets, Restaurants, Households, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

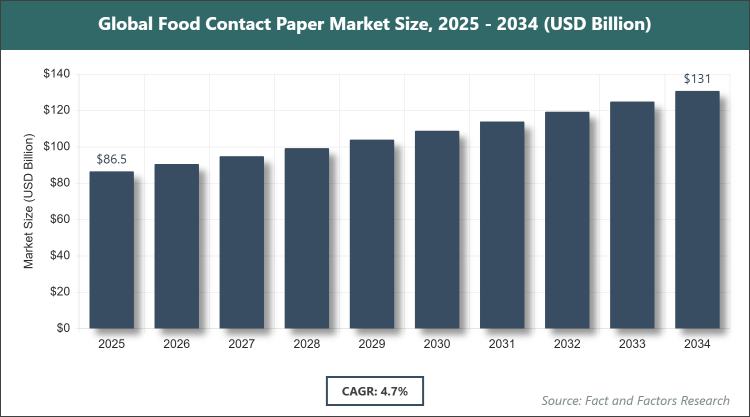

[215+ Pages Report] According to Facts & Factors, the global Food Contact Paper market size was estimated at USD 86.50 billion in 2025 and is expected to reach USD 131.15 billion by the end of 2034. The Food Contact Paper industry is anticipated to grow by a CAGR of 4.70% between 2026 and 2034. The Food Contact Paper Market is driven by growing demand for eco-friendly food packaging.

Market Overview

Market Overview

Food contact paper refers to specialized paper materials designed for direct or indirect contact with food products, ensuring safety, hygiene, and preservation while complying with regulatory standards for migration limits and barrier properties. This market encompasses the production, innovation, and distribution of papers like kraft, greaseproof, and parchment used in packaging solutions that prevent contamination, extend shelf life, and support sustainable alternatives to plastic in various food handling scenarios.

Key Insights

- As per the analysis shared by our research analyst, the Food Contact Paper market is estimated to grow annually at a CAGR of around 4.70% over the forecast period (2026-2034).

- In terms of revenue, the Food Contact Paper market size was valued at around USD 86.50 billion in 2025 and is projected to reach USD 131.15 billion by 2034.

- Due to a variety of driving factors, the market is predicted to rise at a significant rate. The Food Contact Paper Market is driven by increasing demand for sustainable packaging, rising food delivery services, and stringent regulations on plastic use.

- Based on the Type, the Kraft Paper segment dominated the market in 2025 with a market share of 39.67% and why it is due to its strength, sustainability, and versatility in food packaging applications like bags and wrappers.

- Based on the Application, the Takeaway and Vending Foods segment dominated the market in 2025 with a market share of 28% and why it is due to the surge in online food delivery and quick-service restaurants requiring convenient, eco-friendly packaging.

- Based on the End-User, the Food Service Outlets segment dominated the market in 2025 with a market share of 42% and why it is because it caters to high-volume needs in cafes and fast-food chains for hygienic, disposable solutions.

- Based on region, Asia Pacific was the leading revenue generator in 2025, holding a market share of 35.80%, due to rapid growth in the food service industry across China, India, and Japan, along with rising bans on plastic packaging.

Growth Drivers

- Growing Demand for Eco-Friendly Packaging

The shift toward sustainable materials in response to environmental concerns and consumer preferences for biodegradable options has significantly boosted the adoption of food contact paper. This demand is fueled by global initiatives to reduce plastic waste, where paper offers a recyclable alternative that aligns with corporate sustainability goals and enhances brand image.

Additionally, advancements in paper coatings and barriers improve functionality, making it suitable for a wider range of food applications, thereby driving innovation and market penetration in emerging economies focused on green packaging.

Restraints

- Concerns Regarding Chemical Usage

Increasing scrutiny over potential chemical migration from treatments like PFAS in food contact paper poses a barrier, leading to stricter regulations and reformulation costs for manufacturers. This issue arises from health and environmental risks associated with certain additives, impacting consumer trust and supply chain dynamics.

Moreover, the need for ongoing testing and certification to ensure compliance elevates operational expenses, potentially slowing adoption in price-sensitive markets and hindering overall growth amid evolving safety standards.

Opportunities

- Expansion in Online Food Delivery

The boom in e-commerce and food delivery platforms creates avenues for specialized food contact paper designed for insulation and leak-proofing, catering to the need for convenient, sustainable takeout packaging. This trend is amplified by urban lifestyles demanding ready-to-eat solutions.

Furthermore, partnerships with delivery giants can spur customized innovations, expanding market reach and fostering growth in high-growth regions through scalable, eco-conscious products.

Challenges

- Regulatory Compliance Complexity

Navigating diverse international standards for food safety and material composition presents challenges, requiring extensive documentation and adaptations that increase time-to-market. This complexity is heightened by varying regional requirements, affecting global supply chains.

Efforts to standardize regulations are underway, but the lack of uniformity continues to strain resources, particularly for smaller players, potentially limiting innovation and market entry.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 86.50 Billion |

Projected Market Size in 2034 |

USD 131.15 Billion |

CAGR Growth Rate |

4.70% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Mondi Plc, Twin Rivers Paper Company, Westrock Company, Ahlstrom Oyj, Nordic Paper, SCG Packaging PCL, Seaman Paper Company, UPM Global, KRPA PAPER, Smurfit Kappa Group, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Food Contact Paper market is segmented by Type, Application, End-User, and region.

Based on Type Segment, the Food Contact Paper market is divided into Kraft Paper, Greaseproof Paper, Glassine Paper, Parchment Paper, and others. The most dominant segment is Kraft Paper, which leads due to its robust structure ideal for heavy-duty packaging and eco-friendly appeal, driving the market by enabling versatile use in grocery bags and containers that support sustainability trends. The second most dominant is Greaseproof Paper, prominent for its oil-resistant properties in bakery and fast-food wrapping, contributing to market growth through enhanced food preservation and compliance with hygiene standards.

Based on Application Segment, the Food Contact Paper market is divided into Fresh Produce, Dry Groceries, Bakery Products, Liquid Food and Drinks, Takeaway and Vending Foods, and others. The most dominant segment is Takeaway and Vending Foods, excelling because of the rise in on-the-go consumption and delivery services, propelling the market via demand for leak-proof, insulated packaging solutions. The second most dominant is Bakery Products, valued for protecting freshness in items like bread and pastries, boosting market expansion by aligning with consumer preferences for sustainable alternatives.

Based on End-User Segment, the Food Contact Paper market is divided into Food Service Outlets, Restaurants, Households, and others. The most dominant segment is Food Service Outlets, dominating due to high-volume requirements for disposable, hygienic packaging in quick-service environments, driving the market with efficient, cost-effective solutions. The second most dominant is Restaurants, essential for premium takeout and dine-in needs, contributing to market progress through customized, branded packaging that enhances customer experience.

Recent Developments

- In January 2025, Ahlstrom Oyj launched a new line of fully compostable and recyclable grease-resistant papers, developed with a proprietary plant-based coating, offering an alternative to traditional fluorochemical-treated products.

- In April 2025, International Paper Co. announced a significant investment in its North American facilities to upgrade its pulp-processing technology, enhancing its capability to produce recycled-content papers compliant with new FDA food safety guidelines.

- In September 2024, Mondi Plc announced a strategic partnership with a leading food delivery platform to co-develop sustainable, temperature-retaining packaging solutions designed to reduce plastic waste in the food delivery sector.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific holds the leading position in the Food Contact Paper market, propelled by rapid urbanization and a burgeoning food service sector. China dominates as the key country, with its massive manufacturing base and government policies phasing out single-use plastics, accelerating the shift to paper-based solutions in packaging for exports and domestic consumption. India's growing middle class further supports demand through increased takeaway culture, while Japan's focus on high-quality, innovative barriers enhances product sophistication in the region.

North America demonstrates strong growth, supported by stringent food safety regulations and consumer-driven sustainability. The United States leads, emphasizing eco-friendly alternatives in fast-food chains and retail, with Canada's integrated supply chains aiding cross-border trade. Mexico contributes through expanding food processing industries, prioritizing cost-effective yet compliant materials.

Europe maintains a mature market presence, guided by EU directives on circular economy and waste reduction. Germany dominates, leveraging advanced recycling infrastructure and R&D in barrier technologies for bakery and produce packaging. The United Kingdom follows with post-Brexit alignments to green standards, while France emphasizes premium applications in gourmet foods.

Latin America exhibits emerging opportunities, amid economic diversification and environmental awareness. Brazil leads, adopting paper solutions in urban food delivery and agriculture exports to meet global sustainability demands. Argentina supports through institutional packaging in hospitality, fostering regional trade.

Middle East & Africa shows progressive adoption, influenced by tourism and import reliance. Saudi Arabia dominates, integrating food contact paper in Vision 2030's hospitality projects for safe, disposable options in arid conditions. South Africa aids with retail expansions, focusing on hygienic packaging for diverse consumer bases.

Competitive Analysis

The global Food Contact Paper market is dominated by players:

- Mondi Plc

- Twin Rivers Paper Company

- Westrock Company

- Ahlstrom Oyj

- Nordic Paper

- SCG Packaging PCL

- Seaman Paper Company

- UPM Global

- KRPA PAPER

- Smurfit Kappa Group

The global Food Contact Paper market is segmented as follows:

By Type

- Kraft Paper

- Greaseproof Paper

- Glassine Paper

- Parchment Paper

- Others

By Application

- Fresh Produce

- Dry Groceries

- Bakery Products

- Liquid Food and Drinks

- Takeaway and Vending Foods

- Others

By End-User

- Food Service Outlets

- Restaurants

- Households

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Mondi Plc

- Twin Rivers Paper Company

- Westrock Company

- Ahlstrom Oyj

- Nordic Paper

- SCG Packaging PCL

- Seaman Paper Company

- UPM Global

- KRPA PAPER

- Smurfit Kappa Group

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors