![]()

Search Market Research Report

Face Mask Market Size, Share Global Analysis Report, 2026-2034

Face Mask Market Size, Share, Growth Analysis Report By Type (Surgical Masks, N95 Respirators, KN95 Respirators, Cloth/Fashion Masks, and Others), By Application (Individual Use, Industrial Use, and Others), By Distribution Channel (Online Sales, Offline Retail Pharmacies, Supermarkets/Hypermarkets, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

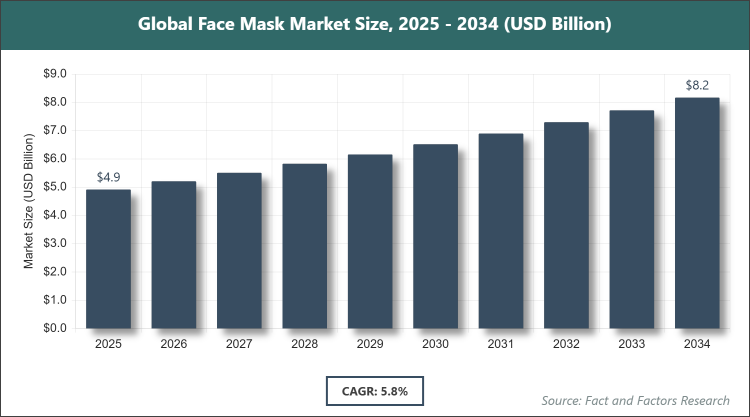

[228+ Pages Report] According to Facts & Factors, the global Face Mask market size was estimated at USD 4.92 billion in 2025 and is expected to reach USD 8.17 billion by the end of 2034. The Face Mask industry is anticipated to grow by a CAGR of 5.8% between 2026 and 2034. The Face Mask Market is driven by sustained demand for respiratory protection, growing hygiene awareness, and increasing industrial safety regulations.

Market Overview

Market Overview

The face mask market encompasses the manufacturing, distribution, and consumption of personal protective devices designed to cover the nose and mouth, primarily to filter airborne particles, droplets, and aerosols, thereby reducing the transmission of respiratory pathogens and protecting both the wearer and others from environmental pollutants, dust, allergens, and occupational hazards. The market includes a wide spectrum of products ranging from disposable medical-grade surgical masks and high-filtration respirators (N95/KN95/FFP2) to reusable cloth and fashion masks, serving healthcare, industrial, consumer, and institutional end-uses. It is heavily influenced by public health policies, occupational safety standards, consumer behavior shifts toward preventive hygiene, sustainability concerns driving biodegradable and washable alternatives, and innovations in filtration efficiency, breathability, comfort, and anti-fog/anti-microbial technologies.

Key Insights

- As per the analysis shared by our research analyst, the global Face Mask market is estimated to grow annually at a CAGR of around 5.8% over the forecast period (2026-2034).

- In terms of revenue, the global Face Mask market size was valued at around USD 4.92 billion in 2025 and is projected to reach USD 8.17 billion, by 2034.

- The Face Mask market is projected to witness significant growth due to persistent respiratory health concerns, stricter workplace safety norms, and rising consumer preference for everyday protection.

- Based on the Type, the Surgical Masks segment accounted for the largest market share of 42% due to widespread institutional demand in healthcare settings and cost-effectiveness for general public use.

- Based on the Application, the Individual Use segment dominated the market with the highest share owing to sustained post-pandemic hygiene consciousness among consumers.

- Based on the Distribution Channel, the Offline Retail Pharmacies segment held the leading position with a substantial share because of immediate availability, professional advice, and consumer trust in pharmacy-sourced medical products.

- Based on the region, the Asia Pacific region captured around 44% market share, driven by large population base, high manufacturing capacity, and ongoing air pollution & health awareness in key countries.

Growth Drivers

- Persistent Respiratory Health & Hygiene Awareness

Even after the acute phase of the COVID-19 pandemic, public consciousness about airborne transmission of viruses (influenza, RSV, new coronaviruses), air pollution (PM2.5), and allergens remains significantly elevated in many countries especially in Asia, Latin America, and parts of Europe sustaining baseline demand for face masks in daily life, public transport, crowded indoor spaces, and during flu seasons. This “new normal” behavior is reinforced by government health advisories, school and workplace mask policies during outbreaks, and increased media coverage of respiratory illnesses.

Additionally, growing elderly populations (who are more vulnerable to respiratory infections) and rising prevalence of chronic respiratory conditions (COPD, asthma) in both developed and developing nations continue to drive consistent therapeutic and preventive usage, creating a stable demand floor far above pre-2020 levels.

Restraints

- Commodity Price Pressure & Declining Perceived Urgency

After the massive demand surge of 2020–2022, the face mask category has become highly commoditized with intense price competition among thousands of manufacturers (especially in China), leading to razor-thin margins, proliferation of low-quality/counterfeit products, and downward pressure on average selling prices, particularly in the surgical and cloth mask segments. In many societies, the sense of “emergency” has faded, reducing everyday voluntary usage among the general population outside of high-risk or high-pollution settings.

Moreover, mask fatigue, social stigma in some regions, and the inconvenience of prolonged wear continue to limit consistent consumer adoption in non-mandatory situations, constraining volume growth in the discretionary individual-use segment.

Opportunities

- Industrial & Occupational Safety Expansion

Stringent workplace safety regulations (OSHA, EU-OSHA, ISO 45001, local equivalents) and growing corporate ESG commitments are driving mandatory or voluntary adoption of respirators and high-filtration masks in construction, mining, manufacturing, welding, pharmaceuticals, laboratories, agriculture, and waste management sectors previously under-penetrated compared to healthcare. This shift is accelerated by rising awareness of long-term occupational lung diseases (silicosis, asbestosis, COPD).

Furthermore, the rapid growth of gig economy delivery riders, sanitation workers, and outdoor laborers in emerging markets creates a large new addressable market for comfortable, durable, reusable, or disposable protective masks designed for extended wear in hot/humid conditions.

Challenges

- Supply Chain Volatility & Raw Material Cost Fluctuations

The face mask industry remains heavily dependent on non-woven polypropylene (meltblown & spunbond), elastic ear loops, and nose wires commodities whose prices are sensitive to petrochemical feedstock costs, energy prices, shipping disruptions, and export restrictions (as seen during 2020–2021). Geopolitical tensions and trade policies can quickly create shortages or cost spikes.

In addition, the coexistence of thousands of small-scale producers, inconsistent quality standards, and periodic overcapacity leads to boom-bust cycles, making long-term planning and pricing strategy difficult for branded manufacturers and distributors.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 4.92 Billion |

Projected Market Size in 2034 |

USD 8.17 Billion |

CAGR Growth Rate |

5.8% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

3M Company, Honeywell International Inc., Kimberly-Clark Corporation, Cardinal Health, Owens & Minor, Prestige Ameritech, Alpha Pro Tech, Moldex-Metric Inc., Makrite, Guangzhou Pidegree Medical Technology Co., Ltd., BYD Precision Manufacturing, Ansell Limited, and Others. |

Key Segment |

By Type, By Application, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Face Mask market is segmented by type, application, distribution channel, and region.

Based on Type Segment, the Face Mask market is divided into Surgical Masks, N95 Respirators, KN95 Respirators, Cloth/Fashion Masks, and others. The most dominant segment is Surgical Masks, which holds the largest share due to their balance of filtration efficacy, breathability, low cost, and universal acceptance in healthcare and general public settings, driving the market by serving as the default choice for institutional procurement and everyday use; the second most dominant is N95 Respirators, critical for high-risk environments and healthcare workers, contributing to market growth through sustained occupational and pandemic preparedness demand.

Based on Application Segment, the Face Mask market is divided into Individual Use, Industrial Use, and others. The most dominant segment is Individual Use, commanding the highest share because of widespread consumer adoption for daily protection against pollution, allergens, and seasonal illnesses, which drives the market by providing volume stability even in non-pandemic periods; the second most dominant is Industrial Use, growing steadily due to regulatory mandates and workplace safety focus, propelling market expansion in manufacturing and construction sectors.

Based on Distribution Channel Segment, the Face Mask market is divided into Online Sales, Offline Retail Pharmacies, Supermarkets/Hypermarkets, and others. The most dominant segment is Offline Retail Pharmacies, holding the biggest share due to consumer trust, immediate availability, professional advice, and role as the primary channel for medical-grade masks, driving the market by ensuring consistent access for health-conscious buyers; the second most dominant is Online Sales, experiencing the fastest growth due to convenience, subscription models, bulk purchasing, and wide product variety.

Recent Developments

- In January 2025, 3M launched an updated N95 respirator series with enhanced headband comfort and better breathability for extended healthcare shifts.

- In late 2024, Honeywell introduced a new range of reusable elastomeric half-mask respirators targeting industrial users in Asia-Pacific and Latin America.

- In Q1 2025, several Chinese manufacturers received updated KN95 certifications under new GB2626-2019 standards, improving export quality to North America and Europe.

- In 2025, major pharmacy chains (CVS, Walgreens, Boots) expanded in-store “mask stations” with fitting guides and sustainability-focused reusable options.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific is the largest and fastest-growing region in the face mask market, with China as the dominant country due to its unparalleled manufacturing capacity (accounting for the majority of global surgical mask and respirator production), massive domestic consumption driven by severe urban air pollution in many cities, high population density, cultural acceptance of mask-wearing, and strong export orientation to North America, Europe, and other regions. Government stockpiling policies, frequent influenza waves, and ongoing health education reinforce baseline demand. China's dominance is reinforced by economies of scale, rapid innovation in automation, and ability to quickly scale production during regional outbreaks.

North America remains a high-value market with strong demand for certified medical-grade and industrial respirators, led by the United States through strict NIOSH/OSHA standards, high healthcare spending, aging population prone to respiratory issues, large construction and manufacturing sectors, and continued public health consciousness post-COVID. Reimbursement for certain medical uses and corporate safety programs support consistent sales.

Europe maintains a mature and quality-focused market, dominated by Germany due to stringent EU MDR regulations, high occupational safety awareness, significant elderly population requiring compression therapy-related products, advanced industrial base (automotive, chemicals), and preference for premium, certified, and sustainable mask options. Cross-border harmonization of standards supports efficient distribution.

Latin America is growing steadily with increasing health awareness and industrial activity, led by Brazil through expanding urban middle class, rising pollution concerns in megacities, growing manufacturing sector, and government health campaigns promoting respiratory protection during dry seasons and influenza periods.

The Middle East & Africa region shows gradual but accelerating adoption, with Saudi Arabia as the dominant country due to Vision 2030 healthcare and industrial diversification investments, large expatriate workforce in construction and oil & gas requiring respiratory protection, increasing air pollution awareness in urban centers, and government stockpiling for public health preparedness.

Competitive Analysis

The global Face Mask market is dominated by players:

- 3M Company

- Honeywell International Inc.

- Kimberly-Clark Corporation

- Cardinal Health

- Owens & Minor

- Prestige Ameritech

- Alpha Pro Tech

- Moldex-Metric Inc.

- Makrite

- Guangzhou Pidegree Medical Technology Co., Ltd.

- BYD Precision Manufacturing

- Ansell Limited

The global Face Mask market is segmented as follows:

By Type

- Surgical Masks

- N95 Respirators

- KN95 Respirators

- Cloth/Fashion Masks

- Others

By Application

- Individual Use

- Industrial Use

- Others

By Distribution Channel

- Online Sales

- Offline Retail Pharmacies

- Supermarkets/Hypermarkets

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- 3M Company

- Honeywell International Inc.

- Kimberly-Clark Corporation

- Cardinal Health

- Owens & Minor

- Prestige Ameritech

- Alpha Pro Tech

- Moldex-Metric Inc.

- Makrite

- Guangzhou Pidegree Medical Technology Co., Ltd.

- BYD Precision Manufacturing

- Ansell Limited

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors