![]()

Search Market Research Report

E-Waste Management Market Size, Share Global Analysis Report, 2024 – 2032

E-Waste Management Market Size, Share, Growth Analysis Report By Material Type (Metal, Plastic, Glass, and Others), By Application (Trashed and Recycled), By Source Type (Household Appliance, Consumer Electronics, Industrial Electronics, and Others), and By Region - Global and Regional Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2024 – 2032

Industry Insights

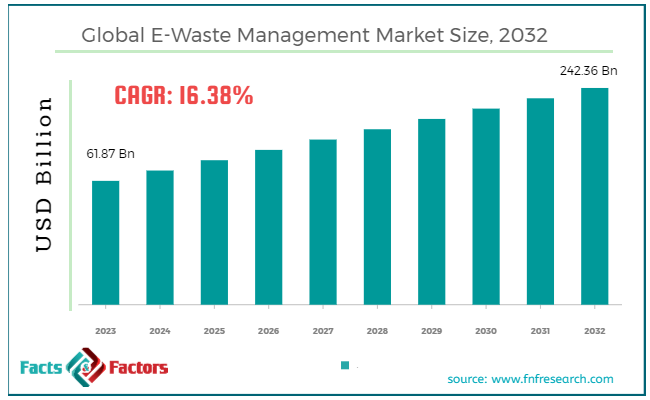

[220+ Pages Report] According to Facts & Factors, the global e-waste management market size in terms of revenue was valued at around USD 61.87 billion in 2023 and is expected to reach a value of USD 242.36 billion by 2032, growing at a CAGR of roughly 16.38% from 2024 to 2032. The global e-waste management market is projected to grow at a significant growth rate due to several driving factors.

Market Overview

Market Overview

E-waste (Electronic waste) management involves the systematic handling of electronic products that have become obsolete or reached the end of their useful life. This process is critical because it addresses both environmental concerns and the recovery of valuable materials from old electronics. Proper e-waste management includes the collection, sorting, recycling, and safe disposal of various types of electronic waste such as computers, smartphones, televisions, household appliances, and other digital and electronic devices.

These items often contain precious metals like gold and silver, as well as hazardous substances including lead, mercury, cadmium, platinum, palladium, gallium, and indium which can pose significant health and environmental risks if not managed properly.

The process of e-waste management not only helps in mitigating the environmental damage caused by the harmful components but also facilitates the recycling and repurposing of materials that would otherwise contribute to resource depletion.

As the global consumption of electronic goods continues to grow, driven by rapid technological advancements and increasing consumer demand, the importance of effective e-waste management becomes more pronounced. It is crucial for minimizing the ecological footprint of discarded electronics, preventing the pollution of ecosystems, and promoting the sustainable use of our planet's resources.

Key Highlights

- The e-waste management market has registered a CAGR of 16.38% during the forecast period.

- In terms of revenue, the global e-waste management market was estimated at roughly USD 61.87 billion in 2023 and is predicted to attain a value of USD 242.36 billion by 2032.

- The global e-waste management market is growing due to rapid technological turnover, stringent environmental regulations, increasing awareness of e-waste hazards, economic benefits from material recovery, advancements in recycling technologies, and corporate commitments to sustainability. These factors drive the demand for effective e-waste management solutions.Top of Form

- Based on the material type, the metal segment is growing at a high rate and is projected to dominate the global market.

- On the basis of the application, the trashed segment is projected to swipe the largest market share.

- Based on the source type, the consumer electronics segment is expected to dominate the global market.

- By region, the Europe region is expected to dominate the global market.

E-Waste Management Market Dynamics:

The e-waste management market navigates a dynamic landscape with forces propelling its growth and obstacles requiring careful consideration. Here's a breakdown of the key drivers, restraints, opportunities, and challenges:

Growth Drivers:

- Surging E-Waste Generation: The insatiable consumer appetite for the latest electronics and rapid technological advancements lead to a constant rise in e-waste. This ever-increasing volume fuels the demand for efficient e-waste management solutions.

- Stringent Environmental Regulations: Governments worldwide are enacting stricter regulations to address the environmental hazards associated with improper e-waste disposal. These regulations mandate responsible e-waste management practices, creating a robust market for compliant solutions.

- Resource Recovery Potential: E-waste is a treasure trove of valuable resources. Recycling metals, plastics, and rare earth elements from e-waste offers significant economic benefits and promotes a more circular economy. This potential for resource recovery is a major driver of market growth.

- Growing Public Awareness: Increased public awareness about the environmental impact of e-waste is fostering a shift towards responsible disposal practices. This growing consciousness creates a wider customer base for e-waste management services.

Restraints:

- Informal Recycling Sector: The presence of a large informal e-waste recycling sector in developing countries raises concerns. These facilities often lack proper infrastructure and environmental safeguards, posing health and environmental risks. Formalizing and regulating this sector present a challenge for the organized e-waste management market.

- High Collection Costs: The logistics of collecting e-waste, particularly from dispersed locations, can be expensive. Developing cost-effective collection methods and infrastructure is crucial for expanding the reach of e-waste management services.

- Lack of Standardized Legislation: The absence of standardized e-waste management regulations across different countries can create confusion and hinder the development of a global e-waste management market. International cooperation to establish uniform standards is necessary.

Opportunities:

- Technological Advancements: Advancements in sorting, dismantling, and recycling technologies can improve efficiency and profitability within the e-waste management sector. This can lead to the development of more sustainable and cost-effective e-waste processing methods.

- Decentralized Processing Solutions: The emergence of smaller, decentralized processing facilities closer to e-waste generation points can reduce transportation costs and improve collection efficiency. This trend presents an opportunity for market expansion.

- Integration with the Circular Economy: E-waste management can play a critical role in the circular economy by capturing valuable resources and reintroducing them into the production cycle. This integration presents opportunities for collaboration between the e-waste management sector and other industries.

Challenges:

- Rapid Evolution of E-Waste: The rapid pace of technological innovation results in a constantly evolving stream of e-waste with diverse materials and components. Adapting e-waste management processes to handle this complexity remains a challenge.

- Consumer Behavior: Encouraging consumers to properly dispose of e-waste and participate in take-back programs is crucial. Shifting consumer behavior patterns towards responsible e-waste management practices requires ongoing educational initiatives.

- Data Security Concerns: E-waste can contain sensitive data. Developing secure and reliable methods for data wiping and destruction before e-waste processing is essential to ensure consumer privacy and data security.

E-Waste Management Market: Segmentation Analysis

The global e-waste management market is segmented based on material type, application, source type, and region.

By Material Type Insights

On the basis of Material Type, the global e-waste management market is bifurcated into metals, plastics, glass, and others. This segment accounted for 48.3% of the total revenue share in 2023. Metals found in e-waste include precious metals such as gold, silver, and platinum, along with base metals like copper, aluminum, and iron. These metals are highly valuable and can be recovered and reused in various industries, including electronics and manufacturing. The metal segment is particularly lucrative due to the high value of recovered metals.

This segment is experiencing robust growth due to efficient and improving technologies for metal recovery and the high demand for these materials in the production of new electronic products. Metals typically have one of the highest CAGRs in the e-waste material segments because of their economic value and the relatively straightforward technologies available for their extraction and recycling.

Plastics constitute a significant portion of e-waste, used primarily as casings and components in electronic devices. This segment is expected to witness the highest growth rate during the forecast period. Recycling plastics from e-waste is crucial to reduce the volume of waste and prevent environmental pollution. Plastic recycling is challenging due to the presence of flame retardants and other additives that complicate the recycling process.

However, advancements in recycling technologies and increased focus on sustainable materials are driving growth in this segment. The growth rate for recycled plastics is increasing as new methods are developed to handle the complexity of plastic waste, including chemical recycling techniques that break down plastics into their constituent monomers.

Glass is primarily found in screens and monitors and is often treated with chemicals to enhance performance, which can complicate recycling processes. The glass segment is growing due to the development of specialized processes to remove impurities and recover glass for reuse, particularly in the manufacture of new electronic screens or other glass products. Glass recycling in e-waste management is gaining momentum, but it typically has a lower CAGR compared to metals due to the lesser economic value and higher processing costs associated with glass recovery.

By Application Insights

The e-waste management market can be segmented by application into trashed and recycled. This segment accounted for 60.2% of revenue share in 2023. Trashed segment involves e-waste that is disposed of in landfills or incinerated without any prior sorting or processing.

Trashing is the least environmentally friendly method of e-waste disposal as it leads to the release of toxic substances into the environment and the loss of potentially valuable materials. Despite growing environmental awareness and stricter regulations, a significant proportion of e-waste still ends up being trashed, particularly in regions with less stringent waste management policies or inadequate recycling infrastructure. The growth rate in this segment is gradually declining as more effective recycling technologies become available and as regulatory frameworks around the world tighten.

The recycled segment includes e-waste that is processed to extract valuable materials for reuse in manufacturing new products. This segment is registering growth at a CAGR of 19.2% between 2024 to 2032. This process not only conserves natural resources but also reduces environmental pollution. Recycling is the fastest-growing segment in the e-waste management market, driven by increasing consumer awareness, technological advancements in recycling processes, and robust regulatory support promoting sustainable waste management practices.

This segment's growth is further supported by the economic benefits of recovering precious metals and other valuable materials from discarded electronics. The recycling segment exhibits a higher CAGR compared to trashing, reflecting the global shift towards sustainable development and circular economy principles. The adoption of advanced recycling technologies that improve the efficiency and effectiveness of material recovery is a key factor propelling this growth.

By Source Type Insights

Based on Source Type, the global e-waste management market is categorized into household appliance, consumer electronics, industrial electronics, and others. Household appliance segment includes large appliances like refrigerators, washing machines, and air conditioners, as well as smaller items like microwaves and vacuum cleaners.

Household appliances often contain a variety of materials including metals, plastics, and glass that require specialized recycling processes. The replacement cycle for household appliances, driven by technological advancements and consumer demand for energy-efficient models, contributes to a significant volume of e-waste. The segment's growth in the e-waste management market is bolstered by stringent regulations on appliance disposal and recycling, particularly in developed countries.

Consumer electronics segment encompasses personal electronics such as smartphones, tablets, computers, and televisions. These products typically have shorter life cycles and are rapidly upgraded due to fast-paced technological innovations and consumer demand for the latest technologies. This segment has held a market share of around 40.6% in 2023. Consumer electronics generate a substantial amount of e-waste, characterized by high turnover rates. The segment is a major focus of e-waste recycling efforts due to the high volume and the valuable materials like precious metals and rare earth elements that can be recovered. Recycling initiatives are increasingly supported by consumer awareness and manufacturer take-back programs.

Industrial electronics include devices and systems used in industrial settings, such as control systems, sensors, and large-scale electronic equipment. These items are critical for various industrial operations and often contain valuable, high-grade materials suitable for recovery. The recycling of industrial electronics is driven by the need to manage the disposal of specialized and often hazardous electronic components used in manufacturing and other industrial processes. The segment benefits from the growing industrial focus on sustainability and the responsible disposal of obsolete electronics.

Recent Developments:

- In July 2023, ERI stepped up its commitment to sustainability by launching IT asset disposition and e-waste recycling services aimed at helping businesses achieve their Environmental, Social, and Governance (ESG) goals and support the circular economy.

- Earlier in 2022, ERI partnered with Call2Recycle and CellBlock FCS to debut OneDrum, an innovative solution for collecting and transporting large volumes of consumer batteries. This system streamlines the recycling process by eliminating the need for sorting batteries by chemistry or individually bagging battery terminals.

- In another initiative from 2022, ERI collaborated with Redrock Environmental Group to offer residents of Madera County a green solution for disposing of unwanted consumer electronics, thereby fostering community engagement in sustainable practices.

- Also in 2022, TES, a firm specializing in IT Asset Disposal and e-waste management, strategically divested its European trade operations focused on e-scrap recycling. This decision was made to better align with extended producer responsibility programs, enhancing its commitment to environmentally responsible recycling practices.

Report Scope

Report Attribute |

Details |

Market Size in 2023 |

USD 61.87 Billion |

Projected Market Size in 2032 |

USD 242.36 Billion |

CAGR Growth Rate |

16.38% CAGR |

Base Year |

2023 |

Forecast Years |

2024-2032 |

Key Market Players |

ERI, Aurubis AG, Boliden AB, Capital Environment Holdings Ltd., Cimelia Resource Recovery, CRT Recycling Ltd., Electronic Waste Management, Enviro-Hub Holdings Ltd., eolia, Global Electric Electronic Processing Inc., MBA Polymer Inc. , MBA Polymers Inc., MRI Pty Ltd., Sembcorp Environmental Management, Sims Lifecycle Services, Stena Metall AB., Tetronics (International) Limited, TRIPLE M METAL LP, Umicore, Waste Management Inc., and Others. |

Key Segment |

By Material Type, By Application, By Source Type, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

E-Waste Management Market: Regional Analysis

In North America, the e-waste management market is driven by strong regulatory policies, particularly in the United States and Canada. Both countries have robust regulatory frameworks that mandate the recycling of e-waste and penalize improper disposal. The United States leads with initiatives such as state-specific e-waste legislation, which require manufacturers to finance the recycling of electronic goods.

There is a well-established infrastructure for e-waste collection and recycling, including high-tech facilities that ensure the safe and efficient processing of electronic waste. Public awareness and corporate responsibility also play significant roles in driving the e-waste management initiatives forward. The market in North America is characterized by a high degree of innovation in recycling technologies and a significant CAGR that reflects steady growth in the sector.

Europe is often considered the global leader in e-waste management due to stringent EU regulations like the Waste Electrical and Electronic Equipment (WEEE) Directive and the Restriction of Hazardous Substances (RoHS) Directive. This region has captured a market share of around 38.6% in 2023. These regulations enforce strict standards on the collection, treatment, and recycling of e-waste, and they encourage manufacturers to design electronics in an environmentally-friendly manner. Countries such as Germany, Sweden, and the Netherlands have some of the highest e-waste recycling rates in the world.

The European market benefits from extensive public sector involvement and sophisticated recycling technologies that enable high recovery rates of valuable materials from e-waste. Europe's CAGR is among the highest globally and is expected to grow at a CAGR of 17.15% from 2024 to 2032, supported by proactive policies and high consumer awareness about environmental sustainability.

The Asia-Pacific region experiences rapid growth in e-waste generation due to increasing electronic consumption in emerging economies like China and India. This region faces significant challenges due to varied regulatory environments and often insufficient e-waste management infrastructure.

However, the potential for market growth is substantial, driven by urbanization, rising incomes, and increasing awareness of the need for sustainable waste management practices. Initiatives are increasingly being put in place to improve e-waste management, and countries like South Korea, Japan, and Taiwan are leading in terms of implementing effective e-waste policies and recycling technologies. The CAGR in Asia-Pacific is expected to be very high as these efforts continue to expand.

In Latin America, the e-waste management market is developing, with countries like Brazil and Argentina slowly building their e-waste regulatory and processing capabilities. The region generally lacks comprehensive legal frameworks specific to e-waste, which hampers the formal development of e-waste recycling sectors.

However, the increasing penetration of electronics in the region, coupled with growing environmental awareness, is likely to drive the demand for better e-waste management practices in the coming years. Investments in recycling infrastructure and the establishment of formal e-waste collection mechanisms are expected to increase, offering a significant growth potential in the market.

The Middle East and Africa (MEA) region shows increasing signs of entering the e-waste management market with more focus due to the expanding volume of e-waste generated by growing urban populations and increased access to consumer electronics. The regulatory environment across the region remains underdeveloped, with many countries lacking specific e-waste legislation.

However, initiatives in countries like South Africa, which has a more established e-waste management framework, point towards a gradual evolution towards structured e-waste recycling systems. The market is at a nascent stage but has potential for high growth if supported by appropriate policy frameworks and investments in recycling technologies.

E-Waste Management Market: List of Key Players

Some of the main competitors dominating the global e-waste management market include;

- ERI

- Aurubis AG

- Boliden AB

- Capital Environment Holdings Ltd.

- Cimelia Resource Recovery

- CRT Recycling Ltd.

- Electronic Waste Management

- Enviro-Hub Holdings Ltd.

- eolia

- Global Electric Electronic Processing Inc.

- MBA Polymer Inc.

- MBA Polymers, Inc.

- MRI Pty Ltd.

- Sembcorp Environmental Management

- Sims Lifecycle Services

- Stena Metall AB.

- Tetronics (International) Limited

- TRIPLE M METAL LP

- Umicore

- Waste Management, Inc.

The global e-waste management market is segmented as follows:

By Material Type Segment Analysis

- Metal

- Plastic

- Glass

- Others

By Application Segment Analysis

- Trashed

- Recycled

By Source Type Segment Analysis

- Household Appliance

- Consumer Electronics

- Industrial Electronics

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- ERI

- Aurubis AG

- Boliden AB

- Capital Environment Holdings Ltd.

- Cimelia Resource Recovery

- CRT Recycling Ltd.

- Electronic Waste Management

- Enviro-Hub Holdings Ltd.

- eolia

- Global Electric Electronic Processing Inc.

- MBA Polymer Inc.

- MBA Polymers, Inc.

- MRI Pty Ltd.

- Sembcorp Environmental Management

- Sims Lifecycle Services

- Stena Metall AB.

- Tetronics (International) Limited

- TRIPLE M METAL LP

- Umicore

- Waste Management, Inc.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors