![]()

Search Market Research Report

Alloy Steel Market Size, Share Global Analysis Report, 2026-2034

Alloy Steel Market Size, Share, Growth Analysis Report By Type (Flat Products, Long/Tubular Products, Semi-Finished Products, and Others), By Grade (High Alloy Steels, Low Alloy Steels), By Application (Automotive, Machinery & Equipment, Oil and Gas, Construction, Aerospace, Power Generation, Marine, and Others), By Process (Hot Rolled, Cold Rolled, Forged, Extruded, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

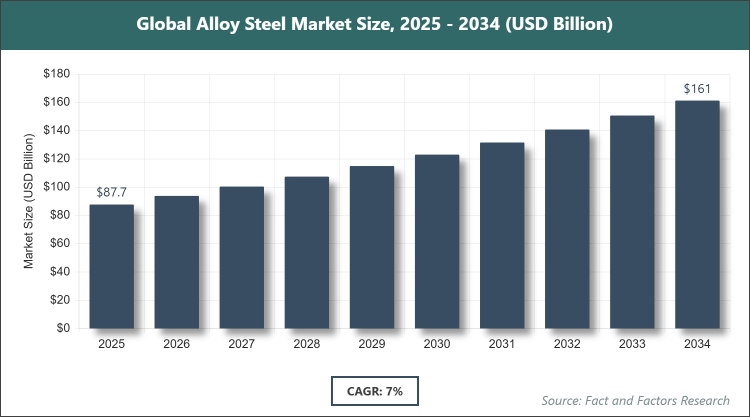

[218+ Pages Report] According to Facts & Factors, the global Alloy Steel market size was estimated at USD 87.72 billion in 2025 and is expected to reach USD 162.35 billion by the end of 2034. The Alloy Steel industry is anticipated to grow by a CAGR of 7.0% between 2026 and 2034. The Alloy Steel Market is driven by expanding construction and automotive sectors demanding high-strength materials.

Market Overview

Market Overview

The alloy steel market refers to the production, distribution, and utilization of steel enhanced with alloying elements such as chromium, nickel, molybdenum, and vanadium to improve properties like strength, corrosion resistance, and durability for demanding applications. This market caters to industries requiring materials that withstand extreme conditions, offering variants from low-alloy to high-alloy steels tailored for specific performance needs. It encompasses a value chain focused on raw material processing, melting, forming, and heat treatment to produce versatile products integral to infrastructure, transportation, and energy sectors, emphasizing innovation in composition for enhanced sustainability and efficiency.

Key Insights

- As per the analysis shared by our research analyst, the global Alloy Steel market is estimated to grow annually at a CAGR of around 7.0% over the forecast period (2026-2034).

- In terms of revenue, the global Alloy Steel market size was valued at around USD 87.72 billion in 2025 and is projected to reach USD 162.35 billion by 2034.

- The Alloy Steel market is projected to witness significant growth due to rising infrastructure development and automotive production demands.

- Based on the Type, the Flat Products segment accounted for the largest market share of 45% due to its extensive use in automotive and construction for sheets and plates.

- Based on the Grade, the Low Alloy Steels segment dominated the market with the highest share, owing to cost-effectiveness and versatility in structural applications.

- Based on the Application, the Automotive segment held the leading position with a substantial share because of increasing demand for lightweight, high-strength components.

- Based on the Process, the hot-rolled segment accounted for the largest market share of 50% due to its efficiency in producing large volumes at lower costs.

- Based on the region, the Asia Pacific region captured around 60% market share, driven by rapid industrialization and manufacturing growth in emerging economies.

Growth Drivers

- Expanding Automotive Industry

The automotive sector's push for lighter, stronger materials to improve fuel efficiency and safety is fueling alloy steel demand, as it provides superior tensile strength and impact resistance for components like chassis and engine parts. Global vehicle production surges, particularly in electric vehicles, require advanced alloys for battery enclosures and structural integrity. Innovations in alloy compositions enhance weldability and formability, supporting mass production techniques.

Furthermore, regulatory standards on emissions drive the adoption of high-performance steels, fostering collaborations between steelmakers and automakers. This synergy not only boosts market volume but also encourages R&D in sustainable alloys, aligning with eco-friendly manufacturing trends and expanding applications in hybrid vehicles.

Restraints

- Volatility in Raw Material Prices

Fluctuations in prices of key alloying elements like nickel and chromium, influenced by mining disruptions and trade tariffs, increase production costs and affect profitability. This instability leads to unpredictable pricing for end-users, potentially slowing adoption in cost-sensitive industries. Supply chain vulnerabilities from geopolitical issues further exacerbate shortages.

Additionally, reliance on imported raw materials exposes manufacturers to currency risks and logistical challenges. These factors constrain market growth, especially for small enterprises, necessitating hedging strategies and alternative sourcing to stabilize operations.

Opportunities

- Advancements in Sustainable Production

The shift toward green steelmaking using electric arc furnaces and recycled scrap offers opportunities to reduce carbon emissions, appealing to environmentally regulated markets. This innovation lowers energy consumption and enhances alloy quality, opening doors for premium, eco-friendly products. Government subsidies for sustainable practices accelerate technology adoption.

Moreover, R&D in bio-based reductants and hydrogen-based processes promises long-term cost savings. This opportunity positions the market for growth in circular economy models, attracting investments and expanding into new sectors like renewable energy infrastructure.

Challenges

- Stringent Environmental Regulations

Increasing global mandates on emissions and waste management require costly upgrades to production facilities, straining resources for compliance. Failure to adapt can result in penalties and market exclusion. Evolving standards demand continuous monitoring and innovation.

In addition, public pressure for low-carbon footprints challenges traditional processes, impacting competitiveness. These issues necessitate strategic investments in clean technologies to overcome barriers and sustain growth.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 87.72 Billion |

Projected Market Size in 2034 |

USD 162.35 Billion |

CAGR Growth Rate |

7.0% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

ArcelorMittal, Nippon Steel Corporation, Tata Steel, JFE Steel Corporation, POSCO, ThyssenKrupp AG, SSAB AB, Outokumpu Oyj, Aperam, Allegheny Technologies Incorporated (ATI), Jindal Stainless, Voestalpine AG, and Others. |

Key Segment |

By Type, By Grade, By Application, By Process, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Alloy Steel market is segmented by type, grade, application, process, and region.

Based on Type Segment, The Alloy Steel market is divided into Flat Products, Long/Tubular Products, Semi-Finished Products, and others. The most dominant segment is Flat Products, which holds the largest share due to its broad applicability in automotive body panels and construction sheets, driving the market by enabling efficient fabrication and cost-effective mass production; the second most dominant is Long/Tubular Products, essential for oil & gas pipelines and structural beams, contributing to market growth through durability in harsh environments and infrastructure projects.

Based on Grade Segment, The Alloy Steel market is divided into High Alloy Steels, Low Alloy Steels. The most dominant segment is Low Alloy Steels, commanding the highest share because of their balanced strength and affordability for general engineering, which drives the market by supporting widespread use in construction and machinery; the second most dominant is High Alloy Steels, preferred for corrosion-resistant applications in aerospace and chemical processing, propelling market expansion via specialized high-value products.

Based on Application Segment, The Alloy Steel market is divided into Automotive, Machinery & Equipment, Oil and Gas, Construction, Aerospace, Power Generation, Marine, and others. The most dominant segment is Automotive, holding the biggest share due to demand for high-strength alloys in vehicle lightweighting, driving the market by improving fuel efficiency and safety standards; the second most dominant is Construction, utilizing alloys for structural integrity in buildings, contributing to market growth amid global urbanization.

Based on Process Segment, The Alloy Steel market is divided into Hot Rolled, Cold Rolled, Forged, Extruded, and others. The most dominant segment is Hot Rolled, with the largest share attributed to its scalability for thick sections in infrastructure, driving the market by reducing processing costs; the second most dominant is Cold Rolled, offering precise dimensions for automotive parts, helping sustain market demand through quality enhancements.

Recent Developments

- In November 2025, global flat steel market trends highlighted growth driven by green steel initiatives and capacity expansions by key players like ArcelorMittal and Tata Steel.

- In January 2023, Evonik invested in upgrading methionine intermediates, indirectly boosting alloy steel use in chemical equipment.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the alloy steel market, dominated by China through its massive manufacturing base and export-driven economy, where rapid urbanization fuels construction and automotive demands for durable alloys. The region's investment in infrastructure projects like high-speed rails enhances alloy adoption for strength and longevity. Government policies promoting industrial upgrades support technological advancements in steel production. China's dominance arises from integrated supply chains and low-cost labor, enabling competitive pricing globally.

North America shows robust growth with focus on advanced alloys for aerospace and energy, led by the United States via innovation hubs and defense spending. The region's emphasis on sustainable materials aligns with regulatory frameworks, driving R&D in high-performance steels. Strategic trade agreements facilitate imports of alloying elements. The U.S. excels through technological leadership and diverse applications in oil & gas.

Europe maintains maturity with emphasis on eco-friendly alloys, dominated by Germany through automotive giants like Volkswagen utilizing high-alloy steels. EU green deals promote recycled steel, fostering circular economies. Collaborative R&D across nations enhances alloy properties for marine and power sectors. Germany's lead stems from engineering expertise and export focus.

Latin America emerges with resource-based production, led by Brazil via mining and construction booms requiring alloy steels for infrastructure. Foreign investments in energy projects boost demand. Brazil's dominance comes from natural resources and regional trade pacts.

The Middle East & Africa advances through oil-driven economies, with Saudi Arabia dominating via diversification into manufacturing using alloys for petrochemical plants. Vision 2030 initiatives spur industrial growth. Saudi Arabia's position strengthens from energy wealth and strategic partnerships.

Competitive Analysis

The global Alloy Steel market is dominated by players:

- ArcelorMittal

- Nippon Steel Corporation

- Tata Steel

- JFE Steel Corporation

- POSCO

- ThyssenKrupp AG

- SSAB AB

- Outokumpu Oyj

- Aperam

- Allegheny Technologies Incorporated (ATI)

- Jindal Stainless

- Voestalpine AG

The global Alloy Steel market is segmented as follows:

By Type

- Flat Products

- Long/Tubular Products

- Semi-Finished Products

- Others

By Grade

- High Alloy Steels

- Low Alloy Steels

By Application

- Automotive

- Machinery & Equipment

- Oil and Gas

- Construction

- Aerospace

- Power Generation

- Marine

- Others

By Process

- Hot Rolled

- Cold Rolled

- Forged

- Extruded

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- ArcelorMittal

- Nippon Steel Corporation

- Tata Steel

- JFE Steel Corporation

- POSCO

- ThyssenKrupp AG

- SSAB AB

- Outokumpu Oyj

- Aperam

- Allegheny Technologies Incorporated (ATI)

- Jindal Stainless

- Voestalpine AG

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors