![]()

Search Market Research Report

Oil Country Tubular Goods Market Size, Share Global Analysis Report, 2026 - 2034

Oil Country Tubular Goods Market Size, Share, Growth Analysis Report By Product Type (Casing Pipe, Tubing Pipe, Line Pipe, and Drill Pipe), By Material Type (Carbon Steel, Alloy Steel, Stainless Steel, Nickel Alloys, and Others), By Application (Drilling, Production, Completion, Workover, and Exploration), By End Use (Oil Industry, Natural Gas Industry, Geothermal Energy, Mining, and Construction), And By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026 - 2034

Industry Insights

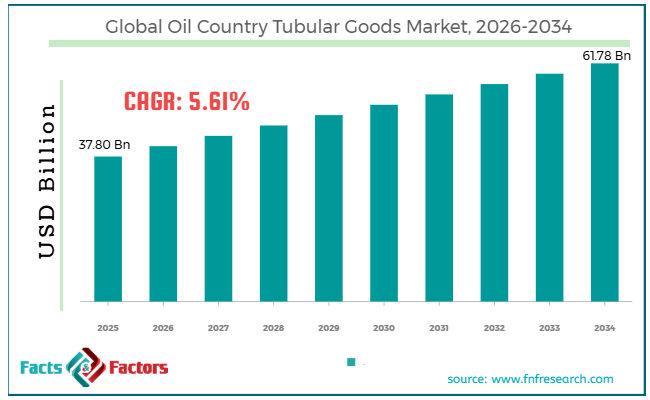

What will be the size of the global oil country tubular goods market during the forecast period?

[221+ Pages Report] According to Facts & Factors, the global oil country tubular goods market size was around USD 37.80 billion in 2025 and is projected to reach USD 61.78 billion by 2034, with a compound annual growth rate (CAGR) of roughly 5.61% between 2026 and 2034.

Market Overview

Market Overview

Oil country tubular goods are dedicated steel pipes used in oil and gas production and exploration, comprising tubing, casing, and drill pipes. They are designed to tolerate harsh temperatures, high pressure, and corrosive environments encountered in drilling operations. They hold significance for maintaining well integrity, promising safe extraction, and enhancing production efficacy. The global oil country tubular goods market is projected to witness substantial growth driven by the expansion of drilling activities, the growth of unconventional resources, and technological improvements in OCTG. Increasing investments in both offshore and onshore drilling projects are driving OCTG consumption worldwide. Exploration of untapped reserves needs extensive use of casing, tubing, and drill pipes. This sustained drilling activity is a major growth propeller for the market.

Moreover, the development of tight oil, shale gas, and deepwater reserves demands OCTG solutions. These challenging environments are experiencing elevated demand for premium-grade products. Furthermore, continuous advancement in manufacturing processes and materials improves the performance of OCTG products. Enhanced durability, strength, and resistance reduce operational failures and maintenance needs. These improvements encourage broader adoption in complex drilling operations.

Although drivers exist, the global market is challenged by factors like volatility in crude oil prices and high manufacturing costs. Frequent variations in crude oil prices impact production and exploration budgets. During price downturns, companies lessen drilling activities and delay projects. This leads to inconsistent demand for OCTG products worldwide. Likewise, OCTG production involves expensive raw materials, complex processing techniques, and high-grade steel. These high costs increase the overall price of tubular goods. Hence, profit margins can be controlled, mainly in competitive markets. Even so, the global oil country tubular goods industry is well-positioned due to the development of advanced materials and digitalization in oilfields.

Innovation in high-strength steel and corrosion-resistant alloys improves product performance. These materials are ideal for extreme drilling environments and extended product lifespan, thus offering opportunities for premium product segments. Additionally, the adoption of digital technologies like predictive analytics and sensors enhances operational efficiency. Smart monitoring systems help detect failures and enhance performance. This notably fuels demand for technologically-advanced OCTG solutions.

Impact of the USA-Israel war on Iran on the Oil Country Tubular Goods Market

The ongoing conflict, including Iran, has disturbed global oil supplies, fueling crude oil price instability and encouraging increased upstream drilling activity in stable regions. This results in a temporary rise in demand for OCT Goods, especially for tubing and casing used in fresh exploration projects. Nonetheless, supply chain disturbances, geopolitical uncertainty, and high logistics costs create lasting challenges, leading to cautious investments and unstable industry growth.

Key Insights:

- As per the analysis shared by our research analyst, the global oil country tubular goods market is estimated to grow annually at a CAGR of around 5.61% over the forecast period (2026-2034)

- In terms of revenue, the global oil country tubular goods market size was valued at around USD 37.80 billion in 2025 and is projected to reach USD 61.78 billion by 2034.

- The oil country tubular goods market is projected to grow significantly owing to increasing demand for energy worldwide, expansion of shale gas and tight oil production, and increased investments in upstream oil & gas sector.

- Based on product type, the casing pipe segment is expected to lead the market, while the tubing pipe segment is expected to grow considerably.

- Based on material type, the carbon steel segment leads the market, while the alloy steel segment is expected to grow rapidly over the coming years.

- Based on application, the production segment is the dominating segment, while the drilling segment is projected to witness sizeable revenue over the forecast period.

- Based on end use, the oil industry segment is expected to lead the market, followed by the natural gas industry segment.

- By region, North America is projected to dominate the global market during the forecast period, followed by the Asia Pacific.

Growth Drivers

- How is rig count growth & upstream capital investment significantly fueling the oil country tubular goods market?

Worldwide rig activity and upstream capital spending are major drivers of OCTG demand, as every well requires considerable tubular goods. In 2025, rig counts rose notably in major basins, including North America’s shale regions, supporting long-term hydrocarbon supply. Increased exploration budgets by independents and national oil companies drive recurring OCTG purchases. Despite variations, sustained upstream investment promises steady tubular goods procurement, thus impacting the oil country tubular goods market.

- How do technological advancements & premium product adoption positively impact the development of the oil country tubular goods market?

Improvements in threading, metallurgy, and connection systems have driven preference for premium-grade OCTG over standard API grades due to sour and HPHT gas performance. Corrosion-resistant and premium tubular now capture a leading share of shipments, since operators prefer reduced downtime and longer well life. Enhanced manufacturing reliability and efficiency support broader adoption. These technological gains are driving the use of the said products in complex drilling programs.

Restraints

- Supply chain bottlenecks & geopolitical trade barriers notably hinder the market progress

Persistent supply chain disturbances, worsened by COVID-19 consequences, increased tariffs, and geopolitical stresses, are creating delays and cost escalations in material sourcing and distribution. Import duties on steel and associated inputs further complicate worldwide movements of tubular inventory. Logistical challenges also increase transportation costs for heavy OCTG products, especially in offshore or remote locations.

Opportunities

- How is the localization of production & value chain integration offer advantageous conditions for the growth of the oil country tubular goods market?

Establishing regional manufacturing centers near emerging E&P markets, such as APAC, Africa, and South America, reduces reliance on imports and exposure to tariffs while improving delivery schedules. Vertical integration also improves bargaining power with large operators and can lock in long-term contracts with bundled service models. These value chain strategies yield high margins and strong local penetration in the oil country tubular goods industry.

Challenges

- Maintaining consistent quality & QA standards is one of the major challenges to the market growth

Meeting stringent quality standards from API specifications to premium connection certifications is complex, mainly for suppliers scaling their production. Quality lapses, such as threading issues or uneven walls, may lead to high rejection rates and reputational risk. Continuous quality control demands expensive inspection procedures and investments in a skilled workforce.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 37.80 Billion |

Projected Market Size in 2034 |

USD 61.78 Billion |

CAGR Growth Rate |

5.61% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Tenaris, Vallourec, TMK Group, Nippon Steel Corporation, JFE Steel, United States Steel Corporation, ArcelorMittal, SeAH Steel, Tianjin Pipe Group (TPCO), Baoshan Iron & Steel (Baosteel), Jindal Saw Limited, Benteler International, Forum Energy Technologies, ISMT Limited, Continental Alloys & Services, and others. |

Key Segment |

By Product Type, By Material Type, By Application, By End Use, and Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Segmentation Analysis

The global oil country tubular goods market is segmented based on product type, material type, application, end use, and region.

- Why is the Casing Pipe segment projected to dominate the oil country tubular goods market?

Based on product type, the global oil country tubular goods industry is divided into casing pipe, tubing pipe, line pipe, and drill pipe. The casing pipe segment holds a dominant market share of nearly 55%. They are important for lining and supporting wellbores, maintaining structural integrity, and preventing formation collapse under extreme downhole conditions in offshore, onshore, and deepwater drilling projects.

Conversely, the tubing segment ranks second with 31% market share, as it is vital for transporting hydrocarbons from the reservoir to the surface and enhancing production efficiency. Growing production activities, shale and unconventional field development, and enhanced oil recovery sustain a strong demand for tubing.

- What factors help the Carbon Steel segment lead the oil country tubular goods market?

Based on material type, the global market is segmented into carbon steel, alloy steel, stainless steel, nickel alloys, and others. The carbon steel segment holds leadership with 70% market share. This dominance is attributed to its reliable performance under high pressures, cost-efficiency, and broader availability.

Nonetheless, the alloy steel segment holds second place with a 30% share due to its tensile properties, superior strength, and resistance to harsh environments.

- Which factors help the Production segment dominate the oil country tubular goods market?

Based on application, the global oil country tubular goods market is segmented into drilling, production, completion, workover, and exploration. The production segment captures nearly 45% market share. Tubular goods are vital for production activities, including transporting fluids once wells are operational and maintaining well integrity. The segmental dominance is backed by extensive use of casing and tubing over long service periods.

However, the drilling segment ranks second with 35% of the market share. Drilling operations require large volumes of high-performance, durable casing, tubing, and drill pipes. These products support advancements of boreholes into subsurface formations and well construction. Growing investments in onshore, deepwater, and unconventional drilling continue to fuel segmental dominance.

- What are the key reasons for the leadership of the Oil Industry segment in the oil country tubular goods market?

Based on end use, the global market is segmented into oil industry, natural gas industry, geothermal energy, mining, and construction. The oil industry leads the market with 75% share, since tubular goods are widely used for casing, drilling, and production operations. High oilfield activity in key producing regions fuels continuous consumption.

Nevertheless, natural gas is expected to grow considerably, accounting for 25% of the market, driven by rising shale gas and LNG projects that require large volumes of casing, drill pipes, and tubing. Investments in gas infrastructure continue to back stable OCTG demand.

Regional Analysis

- What enables North America strong foothold in the global Oil Country Tubular Goods Market?

North America is likely to sustain its leadership in the oil country tubular goods market, with a 5% CAGR, driven by extensive shale oil and gas development, a well-established manufacturing base and oilfield infrastructure, favorable regulatory policies, and high exploration investment. North America dominates the market due to large shale oil and gas development in Canada and the United States. Advanced horizontal drilling techniques and hydraulic fracturing require large volumes of premium casing and tubing, driving consistent demand for OCTG products.

Moreover, the region's developed oilfield infrastructure and manufacturing base are another propeller. The presence of key OCTG producers with modernized fabrication and coating facilities promises supply and quick delivery to active drilling sites, reinforcing market dominance. Also, favorable regulatory policies and high exploration investment encourage ongoing upstream development. Strong capital expenditure by national and private oil companies on offshore and onshore projects propels OCTG consumption, strengthening regional dominance in the market.

- Why does Asia Pacific rank second in the global Oil Country Tubular Goods Market?

Asia Pacific continues to hold the second-highest share, with a 6.5% CAGR in the oil country tubular goods industry, driven by rapid energy demand growth, expansion of oil & gas infrastructure, and the emergence of unconventional resources. APAC’s growing urbanization and industrialization are fueling a remarkable rise in oil and gas consumption. This increased energy demand drives production and exploration activities, which, in turn, drive the need for OCTG products in the Asia Pacific. Several economies in the region are heavily investing in pipeline networks and new oilfields. The development of offshore and onshore infrastructure is driving demand for tubing, casing, and drilling pipes, which is backing strong OCTG market growth.

Additionally, tight oil and shale gas are rapidly growing in the region, requiring high-strength, advanced tubular goods. These technically demanding operations drive demand for premium OCTG products, strengthening APAC’s position in the global market.

Competitive Analysis

The leading players in the global oil country tubular goods market are:

- Tenaris

- Vallourec

- TMK Group

- Nippon Steel Corporation

- JFE Steel

- United States Steel Corporation

- ArcelorMittal

- SeAH Steel

- Tianjin Pipe Group (TPCO)

- Baoshan Iron & Steel (Baosteel)

- Jindal Saw Limited

- Benteler International

- Forum Energy Technologies

- ISMT Limited

- Continental Alloys & Services

What are the key trends in the global Oil Country Tubular Goods Market?

- Smart oilfield integration and digitalization:

The use of monitoring systems, sensors, and predictive maintenance technologies is growing in oil and gas operations. Smart monitoring helps detect early faults and failures in tubular goods, enhances well performance, and lowers downtime. This creates demand for technologically compatible OCTG products.

- Adoption of advanced drilling technologies:

Horizontal drilling, hydraulic fracturing, and directional drilling are becoming standard in both offshore and onshore projects. These techniques require specialized, durable tubular goods, fueling innovation in OCTG design, coatings, and connections to improve well longevity and efficiency.

The global oil country tubular goods market is segmented as follows:

By Product Type

- Casing Pipe

- Tubing Pipe

- Line Pipe

- Drill Pipe

By Material Type

- Carbon Steel

- Alloy Steel

- Stainless Steel

- Nickel Alloys

- Others

By Application

- Drilling

- Production

- Completion

- Workover

- Exploration

By End Use

- Oil Industry

- Natural Gas Industry

- Geothermal Energy

- Mining

- Construction

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Tenaris

- Vallourec

- TMK Group

- Nippon Steel Corporation

- JFE Steel

- United States Steel Corporation

- ArcelorMittal

- SeAH Steel

- Tianjin Pipe Group (TPCO)

- Baoshan Iron & Steel (Baosteel)

- Jindal Saw Limited

- Benteler International

- Forum Energy Technologies

- ISMT Limited

- Continental Alloys & Services

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors