![]()

Search Market Research Report

Plastic Bags and Sacks Market Size, Share Global Analysis Report, 2026-2034

Plastic Bags and Sacks Market Size, Share, Growth Analysis Report By Product Type (T-shirt Bags, Gusseted Bags, Lay Flat Bags, Trash Bags, Rubble Sacks, Woven Sacks, and Others), By Material (HDPE, LDPE, LLDPE, PP, Biodegradable, and Others), By End-User (Retail & Consumer, Institutional, Industrial), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

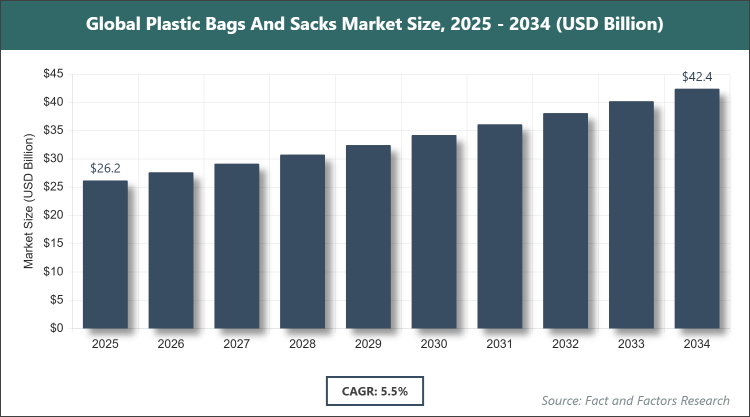

[221+ Pages Report] According to Facts & Factors, the global plastic bags and sacks market size was estimated at USD 26.20 billion in 2025 and is expected to reach USD 42.30 billion by the end of 2034. The plastic bags and sacks industry is anticipated to grow by a CAGR of 5.5% between 2026 and 2034. The plastic bags and sacks Market is driven by increasing demand from retail and e-commerce sectors.

Market Overview

Market Overview

The plastic bags and sacks market encompasses a wide range of flexible packaging solutions made primarily from polymers, designed for carrying, storing, and protecting goods in various forms. These products include lightweight carriers for everyday use, heavy-duty options for waste management, and specialized variants for industrial applications, serving as essential tools in logistics, retail, and household scenarios. Plastic bags and sacks are valued for their versatility, offering features like water resistance, durability, and ease of customization, while adapting to evolving needs in packaging efficiency and sustainability.

Key Insights

- As per the analysis shared by our research analyst, the global plastic bags and sacks market is estimated to grow annually at a CAGR of around 5.5% over the forecast period (2026-2034).

- In terms of revenue, the global plastic bags and sacks market size was valued at around USD 26.20 billion in 2025 and is projected to reach USD 42.30 billion, by 2034.

- The market is driven by expanding retail sectors, rising e-commerce activities, and demand for cost-effective packaging solutions.

- Based on the product type, the T-shirt bags segment dominated the market in 2025 with a share of around 29.4% due to their widespread use in grocery and retail for convenience and low cost.

- Based on the material, the HDPE segment dominated the market in 2025 with a share of around 35% owing to its strength, moisture resistance, and affordability in high-volume applications.

- Based on the end-user, the retail & consumer segment dominated the market in 2025 with a share of around 45% because of increasing consumer reliance on convenient carry solutions in shopping environments.

- Asia Pacific dominated the global market in 2025 with a share of over 43% attributed to rapid industrialization, population growth, and booming e-commerce in the region.

Growth Drivers

- Increasing E-commerce Penetration

The surge in online shopping has significantly boosted the demand for plastic bags and sacks as they provide efficient, lightweight packaging for shipping diverse products ranging from apparel to electronics. This trend is particularly evident in emerging economies where digital retail platforms are expanding rapidly, necessitating reliable and cost-effective packaging to ensure product safety during transit. Innovations in bag designs, such as resealable features, further enhance their appeal for e-commerce logistics, reducing damage rates and improving customer satisfaction.

As e-commerce continues to integrate with traditional retail, the need for versatile sacks that can handle bulk orders and returns grows, driving manufacturers to scale production. This dynamic not only supports market expansion but also encourages investments in automated packaging lines to meet the high-volume requirements of global online marketplaces.

- Rising Demand from Retail and Food Sectors

Retail chains and supermarkets heavily rely on plastic bags for customer convenience, with T-shirt bags being a staple for carrying groceries and daily essentials. The food industry benefits from these products' ability to maintain hygiene and extend shelf life through barrier properties against moisture and contaminants. As urbanization increases, more consumers frequent organized retail, amplifying the volume of bags used daily.

This driver is compounded by the need for customizable branding on bags, which helps retailers enhance visibility and loyalty. In developing regions, the shift from loose to packaged goods further propels usage, aligning with health and safety standards that favor sealed packaging.

Restraints

- Stringent Environmental Regulations

Governments worldwide are imposing bans and taxes on single-use plastics to combat pollution, forcing manufacturers to pivot toward alternatives and increasing operational costs. This regulatory pressure disrupts supply chains and limits the availability of traditional plastic bags in key markets like Europe and parts of North America. Compliance requires significant R&D investments, which can strain smaller players and slow market growth.

The shift also leads to consumer backlash against non-eco-friendly options, reducing demand and prompting boycotts. As policies evolve, inconsistencies across regions create challenges in global trade, further restraining expansion.

- High Volatility in Raw Material Prices

Fluctuations in petroleum-based resin prices, driven by geopolitical tensions and supply disruptions, elevate production costs for plastic bags and sacks. This volatility makes budgeting unpredictable and squeezes profit margins, especially for price-sensitive segments like retail packaging. Manufacturers often pass costs to consumers, potentially reducing affordability and market penetration.

Dependency on fossil fuels exposes the industry to broader energy market shifts, complicating long-term planning. Efforts to hedge through contracts provide limited relief, as sudden spikes can still impact competitiveness against alternative materials.

Opportunities

- Advancements in Biodegradable Materials

The development of eco-friendly polymers like PLA and PBAT opens new avenues for sustainable plastic bags that decompose naturally, appealing to environmentally conscious consumers and regulators. This innovation allows companies to tap into premium markets where green certifications command higher prices and brand loyalty. Partnerships with biotech firms accelerate material enhancements, improving durability without compromising biodegradability.

As corporate sustainability goals align with consumer preferences, biodegradable options gain traction in food packaging and retail, potentially capturing shares from traditional plastics. This opportunity fosters market differentiation and supports expansion into regulated regions.

- Expansion in Emerging Markets

Rapid economic growth in Asia and Latin America creates untapped demand for affordable packaging in burgeoning retail and industrial sectors. Infrastructure development and rising disposable incomes drive consumption of packaged goods, increasing the need for sacks in agriculture and construction. Local manufacturing hubs reduce import dependencies, enabling customized solutions for regional needs.

Strategic alliances with local distributors enhance market entry, while low labor costs boost competitiveness. This expansion diversifies revenue streams and mitigates risks from saturated developed markets.

Challenges

- Competition from Alternative Packaging

The rise of paper bags, reusable totes, and cloth alternatives poses a threat as they gain favor for their perceived environmental benefits. Retailers adopting these options to meet sustainability targets reduce reliance on plastics, fragmenting market share. Educating consumers on the lifecycle advantages of recyclable plastics becomes crucial but challenging amid negative perceptions.

Innovation in alternatives, such as compostable fibers, accelerates substitution, requiring plastic manufacturers to invest heavily in counter-strategies. This competition intensifies price wars and demands continuous product evolution.

- Supply Chain Disruptions

Global events like pandemics and trade conflicts interrupt raw material supplies and logistics, delaying production and increasing costs. Dependency on imported resins heightens vulnerability, leading to shortages and inflated prices. Diversifying suppliers offers partial mitigation but involves additional complexities in quality control.

Adapting to disruptions requires agile operations, yet smaller firms struggle with limited resources. Long-term, building resilient networks is essential but time-consuming in a volatile geopolitical landscape.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 26.20 Billion |

Projected Market Size in 2034 |

USD 42.30 Billion |

CAGR Growth Rate |

5.5% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Novolex, Berry Global Inc., Mondi Group, Inteplast Group, AEP Industries Inc., Ampac Holdings LLC, Bischof & Klein GmbH & Co. KG, Starlinger & Co Gesellschaft M.B.H, Da Nang Plastic Joint Stock Company, Hanoi Plastic Bag JSC, Goglio Group, Schur Flexibles Group, and Others. |

Key Segment |

By Product Type, By Material, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The plastic bags and sacks market is segmented by product type, material, end-user, and region.

Based on Product Type Segment, the plastic bags and sacks market is divided into T-shirt bags, gusseted bags, lay flat bags, trash bags, rubble sacks, woven sacks, and others. The most dominant segment is T-shirt bags, which hold a significant market share due to their ubiquitous use in retail for carrying lightweight items like groceries, offering ease of handling and low production costs that make them ideal for high-volume distribution. The second most dominant is trash bags, valued for their durability in waste management, helping to contain odors and leaks while supporting hygiene standards in households and commercial spaces; together, these segments drive the market by addressing everyday consumer needs and enabling efficient logistics in retail chains.

Based on Material Segment, the plastic bags and sacks market is divided into HDPE, LDPE, LLDPE, PP, biodegradable, and others. HDPE emerges as the most dominant material owing to its high tensile strength and resistance to punctures, making it suitable for heavy-duty applications like trash and industrial sacks, which reduces breakage and enhances reliability in demanding environments. LLDPE ranks as the second most dominant, prized for its flexibility and stretchability that allow for thinner yet stronger films, contributing to cost savings and material efficiency; these materials propel market growth by balancing performance with economic viability across various uses.

Based on End-User Segment, the plastic bags and sacks market is divided into retail & consumer, institutional, industrial. The retail & consumer segment dominates primarily because of the constant demand for convenient carry options in shopping, where bags facilitate impulse buys and customer satisfaction through branding opportunities. The industrial segment is the second most dominant, utilizing sacks for bulk storage and transport of materials like chemicals and construction debris, ensuring safety and efficiency in operations; these end-users fuel overall market expansion by integrating bags into supply chains and daily routines.

Recent Developments

- In early 2025, Novolex announced the acquisition of a biodegradable packaging startup to expand its eco-friendly product line, aiming to meet rising regulatory demands and consumer preferences for sustainable options in North America and Europe.

- Berry Global launched a new range of recycled-content plastic sacks in mid-2025, incorporating 30% post-consumer resin to reduce environmental impact while maintaining strength for industrial applications.

- In late 2025, Mondi Group partnered with a major e-commerce platform to supply customized woven sacks, enhancing durability for shipping and contributing to reduced packaging waste through reusable designs.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the plastic bags and sacks market, driven by its vast manufacturing base and high population density that fuels constant demand across retail and industrial sectors. Countries like China and India lead with extensive production capabilities, where low-cost labor and abundant raw materials enable mass output for both domestic and export needs. The region's rapid urbanization encourages widespread use in everyday commerce, from street vendors to large supermarkets, while e-commerce giants integrate these products into their logistics for efficient delivery. Cultural reliance on convenient packaging further solidifies its position, with innovations adapting to local preferences such as colorful designs for festivals. Overall, the blend of economic growth and infrastructural development positions Asia Pacific as a powerhouse, influencing global trends through scale and affordability.

North America maintains a strong presence in the market, with the United States as the dominating country due to its advanced retail infrastructure and emphasis on consumer convenience. The region benefits from sophisticated supply chains that prioritize durable packaging for food and pharmaceuticals, where regulations on hygiene drive adoption of high-quality sacks. Innovation hubs focus on sustainable variants to align with environmental policies, fostering collaborations between manufacturers and tech firms for smarter materials. E-commerce expansion amplifies usage in warehousing and shipping, while diverse consumer behaviors from urban to rural areas ensure broad application. This dynamic environment supports steady growth, balancing tradition with forward-thinking approaches to packaging challenges.

Europe exhibits a mature market characterized by stringent environmental standards, with Germany leading as the dominant country through its engineering prowess in producing efficient, recyclable bags. The emphasis on circular economy principles encourages shifts toward biodegradable options, integrated into retail and industrial practices across the continent. Collaborative efforts among EU nations standardize quality, reducing waste and promoting reuse in sectors like agriculture and construction. Cultural awareness of sustainability influences consumer choices, pushing manufacturers to innovate in design and functionality. Europe's market thrives on this regulatory-driven evolution, setting benchmarks for global practices while maintaining competitiveness through technological advancements.

Latin America is emerging as a key player, with Brazil dominating due to its expansive agricultural and retail sectors that heavily rely on sacks for transport and storage. The region's tropical climate necessitates moisture-resistant packaging, supporting growth in food exports and local markets. Economic diversification increases demand in urban centers, where e-commerce is gaining traction amid improving internet access. Investments in local production reduce import dependencies, fostering job creation and supply chain resilience. This upward trajectory is marked by adaptations to regional needs, blending affordability with functional improvements to capture more market share.

The Middle East & Africa region shows promising growth, led by South Africa with its developed industrial base utilizing sacks for mining and agriculture. Oil-rich nations in the Middle East leverage petrochemical resources for cost-effective production, supplying both local construction booms and exports. Africa's expanding urban populations drive retail usage, while challenges like waste management spur innovations in durable options. Regional trade agreements enhance distribution, connecting producers with diverse markets. Overall, the area benefits from resource availability and demographic shifts, positioning it for increased contributions to the global landscape.

Competitive Analysis

The global plastic bags and sacks market is dominated by players:

- Novolex

- Berry Global Inc.

- Mondi Group

- Inteplast Group

- AEP Industries Inc.

- Ampac Holdings LLC

- Bischof & Klein GmbH & Co. KG

- Starlinger & Co Gesellschaft M.B.H

- Da Nang Plastic Joint Stock Company

- Hanoi Plastic Bag JSC

- Goglio Group

- Schur Flexibles Group

- And Others

The global plastic bags and sacks market is segmented as follows:

By Product Type

- T-shirt Bags

- Gusseted Bags

- Lay Flat Bags

- Trash Bags

- Rubble Sacks

- Woven Sacks

- Others

By Material

- HDPE

- LDPE

- LLDPE

- PP

- Biodegradable

- Others

By End-User

- Retail & Consumer

- Institutional

- Industrial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global plastic bags and sacks market is dominated by players:

- Novolex

- Berry Global Inc.

- Mondi Group

- Inteplast Group

- AEP Industries Inc.

- Ampac Holdings LLC

- Bischof & Klein GmbH & Co. KG

- Starlinger & Co Gesellschaft M.B.H

- Da Nang Plastic Joint Stock Company

- Hanoi Plastic Bag JSC

- Goglio Group

- Schur Flexibles Group

- Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors