![]()

Search Market Research Report

Photosensitive Polyimide (PSPI) Market Size, Share Global Analysis Report, 2026-2034

Photosensitive Polyimide (PSPI) Market Size, Share, Growth Analysis Report By Type (Positive Photosensitive Polyimide, Negative Photosensitive Polyimide), By Application (Chip Packaging, Memory, Display Panel, Printed Circuit Board, Others), By End-Use Industry (Electronics, Automotive, Aerospace, Healthcare, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

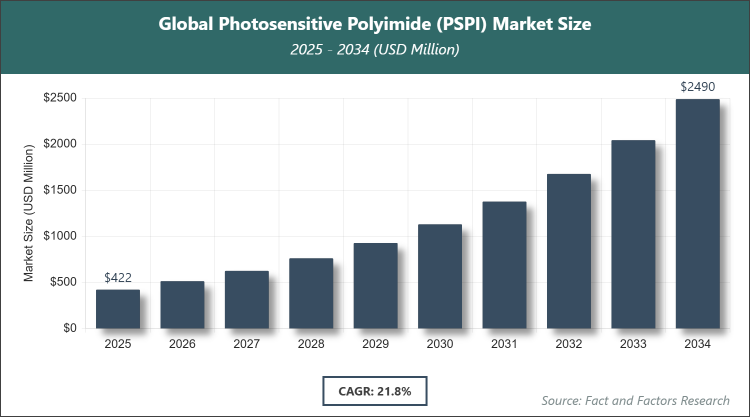

[235+ Pages Report] According to Facts & Factors, the global photosensitive polyimide (PSPI) market size was estimated at USD 422 million in 2025 and is expected to reach USD 3646 million by the end of 2034. The photosensitive polyimide (PSPI) industry is anticipated to grow by a CAGR of 21.8% between 2026 and 2034. The photosensitive polyimide (PSPI) Market is driven by increasing demand in advanced semiconductor packaging and flexible displays.

Market Overview

Market Overview

Photosensitive Polyimide (PSPI) is a high-performance polymer material that exhibits excellent thermal stability, mechanical strength, and chemical resistance while being sensitive to light, enabling precise patterning through photolithography processes. This unique combination makes PSPI ideal for applications in microelectronics, where it serves as an insulating layer, passivation film, or stress buffer in advanced electronic components. Unlike traditional polyimides, PSPI can be directly imaged and developed, simplifying manufacturing workflows and enhancing precision in device fabrication.

Key Insights

- As per the analysis shared by our research analyst, the global photosensitive polyimide (PSPI) market is estimated to grow annually at a CAGR of around 21.8% over the forecast period (2026-2034).

- In terms of revenue, the global photosensitive polyimide (PSPI) market size was valued at around USD 422 million in 2025 and is projected to reach USD 3646 million, by 2034.

- The market is driven by increasing demand for advanced semiconductor packaging, flexible displays, and high-performance electronic components.

- Based on the type, the negative photosensitive polyimide segment accounted for the largest market share of 59% in 2025, due to its superior resolution, better adhesion properties, and compatibility with thick-film applications in semiconductor manufacturing.

- Based on the application, the chip packaging segment dominated with 40% share in 2025, as it benefits from PSPI's ability to provide reliable insulation and stress relief in miniaturized semiconductor devices, driving efficiency in high-density packaging.

- Based on the end-use industry, the electronics segment dominated with 60% share in 2025, owing to widespread adoption in consumer electronics, displays, and circuit boards where PSPI enhances durability and performance under harsh conditions.

- Asia-Pacific dominated the global market with 55% share in 2025, attributed to its robust electronics manufacturing ecosystem, presence of key semiconductor foundries, and rapid industrialization in countries like China, Japan, and South Korea.

Growth Drivers

- Increasing Demand in Semiconductor and Electronics Industries

The photosensitive polyimide (PSPI) market is experiencing robust growth driven by the escalating demand for advanced materials in the semiconductor and electronics sectors. As electronic devices become more compact and powerful, PSPI's exceptional properties, such as high thermal resistance and precise photopatterning capabilities, make it indispensable for applications like wafer-level packaging and flexible circuits. This demand is further amplified by the proliferation of 5G technology, IoT devices, and electric vehicles, which require reliable insulation and protection layers to ensure optimal performance and longevity.

Additionally, advancements in lithography technologies and the push for miniaturization in chip design are propelling PSPI adoption. Manufacturers are increasingly relying on PSPI to achieve finer resolutions and thicker films without compromising mechanical integrity, leading to improved yield rates and cost efficiencies in production processes. The integration of PSPI in next-generation displays, such as OLED and micro-LED, also contributes significantly, as it enables flexible and durable substrates that meet the stringent requirements of modern consumer electronics.

Restraints

- High Production Costs and Complex Manufacturing Processes

One of the primary restraints hindering the growth of the photosensitive polyimide (PSPI) market is the elevated production costs associated with raw materials and specialized manufacturing techniques. The synthesis of PSPI involves intricate chemical processes and high-purity precursors, which escalate overall expenses and limit accessibility for smaller manufacturers. This cost barrier can deter widespread adoption, particularly in price-sensitive markets or emerging economies where budget constraints are more pronounced.

Furthermore, the complexity of PSPI processing, including precise control over exposure, development, and curing stages, poses challenges in scaling production. Any deviations can lead to defects, reducing yield and increasing waste, which further amplifies costs. Regulatory compliance with environmental standards for chemical handling and disposal adds another layer of complexity, potentially slowing down innovation and market expansion in regions with strict environmental policies.

Opportunities

- Emerging Applications in Flexible Electronics and 5G Infrastructure

The photosensitive polyimide (PSPI) market presents significant opportunities through its expanding role in flexible electronics and 5G infrastructure development. As the demand for foldable devices, wearable technology, and high-speed communication networks surges, PSPI's flexibility, low dielectric constant, and thermal stability position it as a key enabler for innovative designs. This opens avenues for market players to collaborate with tech giants in developing next-gen products that require bendable and reliable materials.

Moreover, investments in research for bio-based and eco-friendly PSPI variants could unlock new markets in sustainable electronics. The growing focus on electric vehicles and renewable energy systems also offers opportunities, where PSPI can be utilized in battery management systems and solar panels for enhanced durability and efficiency. Strategic partnerships and R&D initiatives aimed at reducing costs and improving processability will be crucial in capitalizing on these emerging trends.

Challenges

- Supply Chain Disruptions and Raw Material Volatility

The photosensitive polyimide (PSPI) market faces challenges from supply chain disruptions and volatility in raw material prices, which can impact production stability and profitability. Dependence on specific chemical suppliers, often concentrated in certain regions, makes the market vulnerable to geopolitical tensions, natural disasters, or trade restrictions, leading to shortages and delayed deliveries.

In addition, fluctuations in the prices of key precursors like diamines and dianhydrides, influenced by global oil prices and demand from other industries, add uncertainty. Manufacturers must navigate these issues while maintaining quality standards, which may require diversifying suppliers or investing in alternative materials. The challenge is compounded by the need for continuous innovation to meet evolving industry specifications, demanding agile supply chain strategies to sustain growth.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 422 Million |

Projected Market Size in 2034 |

USD 3646 Million |

CAGR Growth Rate |

21.8% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Kolon Industries Inc., DuPont, HD MicroSystems, Nissan Chemical Corporation, The Chemours Company, UBE Industries Ltd., Kaneka Corporation, Chang Chun Group, Mitsui Chemicals Inc., SKC Kolon PI, Toray Industries Inc., Asahi Kasei, Showa Denko K.K., Sumitomo Chemical, Eternal Materials Co. Ltd., HITACHI Chemical Co. Ltd., JSR Corporation, and Others. |

Key Segment |

By Type, By Application, By End-Use Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The photosensitive polyimide (PSPI) market is segmented by type, application, end-use industry, and region.

Based on Type Segment, the photosensitive polyimide (PSPI) market is divided into positive photosensitive polyimide, negative photosensitive polyimide. The most dominant segment is negative photosensitive polyimide, which holds a significant share due to its excellent resolution, thicker film capabilities, and better compatibility with alkaline developers, making it preferred for complex semiconductor structures. This dominance drives the market by enabling high-precision patterning in advanced packaging, reducing process steps, and improving overall device reliability. The second most dominant is positive photosensitive polyimide, valued for its ease of removal in exposed areas and suitability for fine-line applications, contributing to market growth through its use in display technologies and MEMS devices where clean patterning is essential.

Based on Application Segment, the photosensitive polyimide (PSPI) market is divided into chip packaging, memory, display panel, printed circuit board, others. The most dominant segment is chip packaging, accounting for the largest share because of PSPI's superior dielectric properties and stress buffering, which are critical for protecting delicate semiconductor chips from thermal and mechanical stresses, thereby enhancing device lifespan and performance in high-density integrations. This drives the market by supporting the miniaturization trend in electronics. The second most dominant is printed circuit board, favored for its adhesion and flexibility, aiding in the production of reliable, high-frequency PCBs that meet the demands of 5G and automotive electronics, thus fueling market expansion through improved connectivity and durability.

Based on End-Use Industry Segment, the photosensitive polyimide (PSPI) market is divided into electronics, automotive, aerospace, healthcare, others. The most dominant segment is electronics, with the highest share owing to PSPI's role in enabling compact, high-performance components like displays and sensors, driven by consumer demand for smarter devices. This dominance propels market growth by facilitating innovations in consumer and industrial electronics. The second most dominant is automotive, where PSPI's thermal resistance and reliability support advanced driver-assistance systems and electric vehicle components, contributing to market advancement through enhanced safety and efficiency in modern vehicles.

Recent Developments

- In March 2024, Toray Industries launched a new positive-tone PSPI formulation with sub-8 µm patterning resolution for foldable OLED displays, improving display durability and reducing manufacturing defects by 12%.

- In November 2023, Fujifilm Electronic Materials introduced a hybrid PSPI product combining polyimide and polybenzoxazole chemistries, achieving 15% higher thermal resistance for next-generation semiconductor packaging.

- In February 2024, Asahi Kasei completed a pilot for low-temperature curable PSPI coatings for flexible displays, enhancing bend endurance by 10% and enabling energy-efficient production processes.

- In August 2025, Asahi Kasei announced plans to double its PIMEL™ photosensitive polyimide production capacity at its Fuji City facility by 2030 to meet rising demand in the semiconductor industry.

- In June 2023, Arkema acquired a majority stake in PI Advanced Materials Co., Ltd., to strengthen its position in the high-performance materials sector, particularly in the PSPI market.

Regional Analysis

- Asia-Pacific to dominate the global market

The Asia-Pacific region dominates the global photosensitive polyimide (PSPI) market, primarily due to its status as the world's leading hub for electronics and semiconductor manufacturing. Countries like China, Japan, South Korea, and Taiwan host major foundries and display producers, driving high demand for PSPI in applications such as chip packaging and flexible circuits. The region's rapid industrialization, coupled with government investments in technology infrastructure, fosters innovation and production scalability. China, as the dominating country, benefits from its vast supply chain ecosystem and policy support for semiconductor self-sufficiency, enabling cost-effective mass production and attracting global partnerships that further solidify its leadership.

North America holds a significant position in the PSPI market, supported by advanced R&D capabilities and a strong focus on high-tech industries like aerospace and telecommunications. The United States, the dominating country in this region, leads with cutting-edge innovations from companies in Silicon Valley and robust funding for semiconductor research. This emphasis on technological advancement drives PSPI adoption in next-gen devices, while collaborations between academia and industry accelerate material improvements. The region's emphasis on quality and performance standards ensures sustained growth, particularly in defense and medical applications where reliability is paramount.

Europe's PSPI market is characterized by its emphasis on sustainable and high-precision manufacturing, with key contributions from the automotive and aerospace sectors. Germany, as the dominating country, excels through its engineering prowess and investments in Industry 4.0 initiatives, promoting PSPI use in electric vehicles and smart manufacturing. The region's stringent environmental regulations encourage the development of eco-friendly PSPI variants, fostering innovation. Collaborative efforts across the EU enhance supply chain resilience, positioning Europe as a vital player in advanced materials for diverse industrial applications.

Latin America's PSPI market is emerging, driven by growing electronics assembly and automotive industries, particularly in Mexico and Brazil. Mexico, the dominating country, leverages its proximity to North American markets and trade agreements like USMCA to attract foreign investments in manufacturing. This facilitates PSPI integration in automotive electronics and consumer goods, supporting regional economic growth. However, challenges like infrastructure limitations are being addressed through international partnerships, paving the way for expanded adoption and market development.

The Middle East & Africa region shows potential in the PSPI market, fueled by diversification efforts into technology and manufacturing sectors. The United Arab Emirates, as the dominating country, invests heavily in smart cities and renewable energy projects, incorporating PSPI in electronics and solar applications. Initiatives like Vision 2031 aim to build a knowledge-based economy, attracting global tech firms and enhancing local capabilities. Africa's growing telecom sector also contributes, with increasing demand for durable materials in infrastructure development.

Competitive Analysis

The global photosensitive polyimide (PSPI) market is dominated by players:

- Kolon Industries Inc.

- DuPont

- HD MicroSystems

- Nissan Chemical Corporation

- The Chemours Company

- UBE Industries Ltd.

- Kaneka Corporation

- Chang Chun Group

- Mitsui Chemicals Inc.

- SKC Kolon PI

- Toray Industries Inc.

- Asahi Kasei

- Showa Denko K.K.

- Sumitomo Chemical

- Eternal Materials Co. Ltd.

- HITACHI Chemical Co. Ltd.

- JSR Corporation

The global photosensitive polyimide (PSPI) market is segmented as follows:

By Type

- Positive Photosensitive Polyimide

- Negative Photosensitive Polyimide

By Application

- Chip Packaging

- Memory

- Display Panel

- Printed Circuit Board

- Others

By End-Use Industry

- Electronics

- Automotive

- Aerospace

- Healthcare

- Others

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors