![]()

Search Market Research Report

Medical Oxygen Concentrators Market Size, Share Global Analysis Report, 2026-2034

Medical Oxygen Concentrators Market Size, Share, Growth Analysis Report By Type (Portable, Stationary), By Delivery System (Continuous Flow, Pulse Flow), By Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Respiratory Distress Syndrome, Others), By End-User (Hospitals & Clinics, Home Care Settings, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

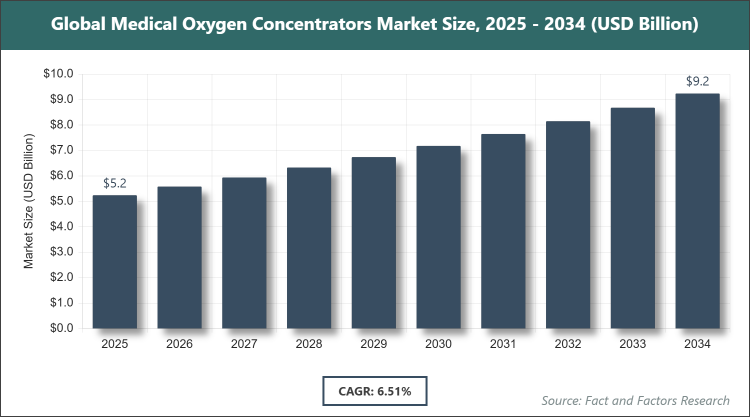

[225+ Pages Report] According to Facts & Factors, the global Medical Oxygen Concentrators market size was estimated at USD 5.24 billion in 2025 and is expected to reach USD 9.25 billion by the end of 2034. The Medical Oxygen Concentrators industry is anticipated to grow by a CAGR of 6.51% between 2026 and 2034. The Medical Oxygen Concentrators Market is driven by the rising prevalence of respiratory diseases and an aging population.

Market Overview

Market Overview

Medical oxygen concentrators are devices that extract oxygen from ambient air through pressure swing adsorption or membrane separation, delivering concentrated oxygen to patients with respiratory deficiencies. These concentrators are essential for home and clinical settings, providing a continuous supply of medical-grade oxygen without the need for refills, and are available in portable and stationary models to accommodate mobility needs. They play a vital role in managing conditions like chronic obstructive pulmonary disease, asthma, and sleep apnea, offering a safe, cost-effective alternative to liquid or gaseous oxygen systems by ensuring reliable therapy while minimizing logistical challenges associated with traditional oxygen delivery methods.

Key Insights

- As per the analysis shared by our research analyst, the global Medical Oxygen Concentrators market is estimated to grow annually at a CAGR of around 6.51% over the forecast period (2026-2034).

- In terms of revenue, the global Medical Oxygen Concentrators market size was valued at around USD 5.24 billion in 2025 and is projected to reach USD 9.25 billion by 2034.

- The market is driven by increasing demand for home-based oxygen therapy and technological advancements in portable devices.

- Based on the type, the portable segment dominated the market with a share of 60%, as it offers mobility and convenience for patients with active lifestyles, enhancing compliance and accessibility.

- Based on the delivery system, the pulse flow segment dominated with a share of 55%, due to its efficiency in oxygen delivery synchronized with breathing, conserving energy, and extending battery life.

- Based on the application, the COPD segment dominated with a share of 45%, attributed to the high prevalence of the disease requiring long-term oxygen support.

- Based on the end-user, the home care settings segment dominated with a share of 65%, owing to the shift toward home healthcare and cost-effectiveness.

- North America dominated the global market with a share of 40%, due to advanced healthcare infrastructure, high disease prevalence, and favorable reimbursement policies.

Growth Drivers

- Rising Prevalence of Respiratory Disorders

The escalating incidence of chronic respiratory conditions such as COPD, asthma, and pneumonia, exacerbated by pollution, smoking, and aging populations, has heightened the demand for medical oxygen concentrators as a primary therapy tool. This driver is supported by global health initiatives focusing on early diagnosis and management, leading to increased adoption in both clinical and home environments. Technological improvements in device efficiency and user-friendliness further amplify this growth, making concentrators a preferred choice over traditional oxygen sources.

Moreover, the integration of smart features like remote monitoring and app connectivity enhances patient outcomes by enabling real-time adjustments and compliance tracking. As healthcare systems emphasize preventive care, the market benefits from expanded access to these devices through insurance coverage and government programs, sustaining long-term expansion.

Restraints

- High Device Costs and Maintenance Requirements

The substantial purchase price of advanced oxygen concentrators, coupled with ongoing maintenance and electricity costs, limits accessibility in low-income regions and for uninsured patients. This restraint is particularly pronounced in developing countries where economic constraints and inadequate power infrastructure hinder widespread use, despite growing health needs.

Additionally, the need for regular filter replacements and professional servicing adds to the total ownership cost, potentially deterring adoption among elderly or low-mobility users. These factors contribute to market fragmentation, with cheaper alternatives like oxygen cylinders competing in price-sensitive segments, slowing overall penetration.

Opportunities

- Expansion in Emerging Markets

Rapid urbanization and improving healthcare access in the Asia Pacific and Latin America present opportunities for market entry through affordable, localized manufacturing and distribution partnerships. Innovations in battery-powered, lightweight models cater to regions with unreliable electricity, tapping into underserved populations with rising respiratory issues.

Furthermore, collaborations with governments for public health programs and telemedicine integration can accelerate adoption. This opportunity fosters diversified revenue, with potential for customized solutions addressing local environmental challenges like high altitude or pollution, positioning companies for global leadership.

Challenges

- Regulatory Compliance and Supply Chain Issues

Stringent approval processes from bodies like the FDA and EMA delay product launches, while supply chain disruptions for components like zeolites affect production timelines. These challenges are intensified by geopolitical tensions and raw material shortages, impacting device availability during demand surges like pandemics.

In addition, varying international standards complicate global exports, requiring extensive testing and adaptations. Overcoming these through resilient supply networks and accelerated regulatory pathways is essential, but persistent issues could erode market confidence and growth momentum.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 5.24 Billion |

Projected Market Size in 2034 |

USD 9.25 Billion |

CAGR Growth Rate |

6.51% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Koninklijke Philips N.V., Invacare Corporation, Inogen, GCE Healthcare, CAIRE Inc., Drive DeVilbiss International, O2 Concepts, LLC, Nidek Medical Products, Inc., Precision Medical, Inc., Besco Medical, and Others. |

Key Segment |

By Type, By Delivery System, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Medical Oxygen Concentrators market is segmented by type, delivery system, application, end-user, and region.

Based on Type Segment, the Medical Oxygen Concentrators market is divided into portable, stationary. The portable segment emerges as the most dominant, holding approximately 60% market share, primarily due to its convenience for ambulatory patients, enabling independent living and travel, which drives market growth by expanding usage beyond hospitals and supporting the trend toward home-based care. The stationary segment follows as the second most dominant, with around 40% share, owing to its higher oxygen output for severe cases and cost-effectiveness for long-term use, contributing to market expansion by serving inpatient and high-flow therapy needs.

Based on Delivery System Segment, the Medical Oxygen Concentrators market is divided into continuous flow, pulse flow. The pulse flow segment is the most dominant, capturing about 55% of the market, as it delivers oxygen on-demand, improving battery life and portability, driven by patient preference for energy-efficient devices and helping to propel the market through enhanced user satisfaction and compliance. The continuous flow segment ranks second, with roughly 45% share, benefiting from its reliability for patients requiring steady oxygen supply, aiding market growth by addressing critical care scenarios in clinical settings.

Based on Application Segment, the Medical Oxygen Concentrators market is divided into chronic obstructive pulmonary disease (COPD), asthma, respiratory distress syndrome, others. The chronic obstructive pulmonary disease (COPD) segment is the most dominant, capturing about 45% of the market, due to the high global burden of COPD necessitating long-term oxygen therapy, thereby driving the market through increased demand for reliable concentrators in management protocols. The asthma segment ranks second, with roughly 25% share, leveraging concentrators for acute exacerbations and home monitoring, contributing to market growth by supporting preventive care and reducing hospital visits.

Based on End-User Segment, the Medical Oxygen Concentrators market is divided into hospitals & clinics, home care settings, others. The home care settings segment is the most dominant, capturing about 65% of the market, propelled by the shift to home-based therapy for cost savings and patient comfort, driving the market through broader accessibility and telehealth integration. The hospitals & clinics segment ranks second, with roughly 30% share, utilizing concentrators for inpatient care and emergencies, aiding market expansion by ensuring efficient oxygen supply in high-volume facilities.

Recent Developments

- In May 2023, Inogen Inc. launched the Rove 6 portable oxygen concentrator with an 8-year service life, enhancing durability and patient reliability for long-term use.

- In October 2023, CAIRE Inc. introduced the Companion 5 stationary concentrator with autoFLOW technology, adjusting flow rates to reduce energy consumption and improve efficiency.

- In January 2024, Philips Respironics released an updated SimplyGo Mini with improved battery life, targeting mobile patients with respiratory conditions.

- In July 2024, Drive DeVilbiss Healthcare expanded its production facility to meet rising demand for home oxygen solutions post-pandemic.

- In November 2025, Nidek Medical partnered with a telehealth provider to integrate monitoring features into its concentrators for remote patient management.

Regional Analysis

- North America to dominate the global market

North America leads the medical oxygen concentrators market, supported by advanced healthcare systems, high awareness of respiratory health, and robust reimbursement policies that facilitate device adoption. The United States dominates this region with its large patient pool suffering from COPD and asthma, coupled with significant R&D investments leading to innovative portable solutions, enabling better home care and reducing hospital burdens while driving technological advancements.

Europe maintains a prominent position, driven by aging demographics and stringent health regulations promoting quality devices. Germany emerges as the key country, with its strong manufacturing base and focus on precision engineering, fostering developments in energy-efficient concentrators that align with sustainability goals and support widespread use in clinical and home settings across the continent.

Asia Pacific shows accelerated growth, fueled by urbanization, pollution-related respiratory issues, and improving medical infrastructure. China stands out as dominant, leveraging its massive population and government initiatives for healthcare access, rapidly expanding production and distribution to meet domestic demand and export needs in emerging markets.

Latin America experiences emerging expansion, aided by increasing healthcare investments and awareness campaigns. Brazil leads, utilizing its growing economy and public health programs to adopt affordable concentrators, addressing rural access challenges and enhancing treatment for chronic conditions in diverse populations.

The Middle East & Africa region progresses steadily, propelled by infrastructure developments and international aid. South Africa dominates, capitalizing on its advanced medical facilities and efforts to combat respiratory diseases, integrating concentrators into national health strategies for improved patient outcomes in urban and remote areas.

Competitive Analysis

The global Medical Oxygen Concentrators market is dominated by players:

- Koninklijke Philips N.V.

- Invacare Corporation

- Inogen

- GCE Healthcare

- CAIRE Inc.

- Drive DeVilbiss International

- O2 Concepts, LLC

- Nidek Medical Products, Inc.

- Precision Medical, Inc.

- Besco Medical

- And Others.

The global Medical Oxygen Concentrators market is segmented as follows:

By Type

- Portable

- Stationary

By Delivery System

- Continuous Flow

- Pulse Flow

By Application

- Chronic Obstructive Pulmonary Disease (COPD)

- Asthma

- Respiratory Distress Syndrome

- Others

By End-User

- Hospitals & Clinics

- Home Care Settings

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Koninklijke Philips N.V.

- Invacare Corporation

- Inogen

- GCE Healthcare

- CAIRE Inc.

- Drive DeVilbiss International

- O2 Concepts, LLC

- Nidek Medical Products, Inc.

- Precision Medical, Inc.

- Besco Medical

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors