![]()

Search Market Research Report

LCD Monitor Arm Market Size, Share Global Analysis Report, 2026-2034

LCD Monitor Arm Market Size, Share, Growth Analysis Report By Type (Single Monitor Arm, Dual Monitor Arm, Multi-Monitor Arm), By Application (Office, Healthcare, Education, Others), By End-User (Commercial, Residential, Industrial), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

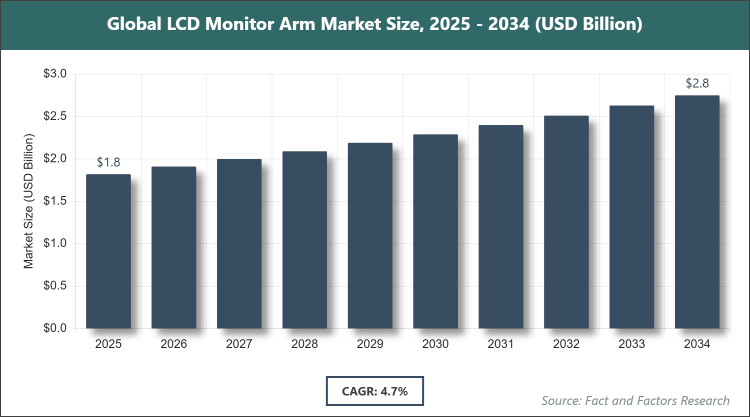

[230+ Pages Report] According to Facts & Factors, the global LCD monitor arm market size was estimated at USD 1.82 billion in 2025 and is expected to reach USD 2.84 billion by the end of 2034. The LCD monitor arm industry is anticipated to grow by a CAGR of 4.7% between 2026 and 2034. The LCD monitor arm Market is driven by increasing demand for ergonomic workspace solutions.

Market Overview

Market Overview

The LCD monitor arm market encompasses products designed to support and position LCD monitors in various settings, allowing for adjustable height, tilt, swivel, and rotation to enhance user comfort and productivity. These arms are essential accessories that attach to desks, walls, or other surfaces, providing flexibility in monitor placement while optimizing space and reducing strain on the neck, eyes, and back. They cater to a wide range of users by improving ergonomics in professional and personal environments, with designs varying from basic fixed models to advanced multi-joint systems that accommodate single or multiple screens.

Key Insights

- As per the analysis shared by our research analyst, the LCD monitor arm market is estimated to grow annually at a CAGR of around 4.7% over the forecast period (2026-2034).

- In terms of revenue, the LCD monitor arm market size was valued at around USD 1.82 billion in 2025 and is projected to reach USD 2.84 billion, by 2034.

- The LCD monitor arm market is driven by increasing adoption of ergonomic office equipment.

- Based on the type, the single monitor arm segment dominated with 50% share because it offers cost-effective and versatile solutions for basic workstation setups, appealing to a broad user base in home offices and small businesses.

- Based on the application, the office segment dominated with 45% share because of the surge in remote and hybrid work models that prioritize adjustable setups for prolonged computer use.

- Based on the end-user, the commercial segment dominated with 60% share because businesses invest heavily in employee wellness and productivity-enhancing tools.

- The North America region dominated the market with 35% share because of high awareness of workplace ergonomics, stringent health regulations, and widespread adoption of advanced office technologies.

Growth Drivers

- Increasing Adoption of Ergonomic Workspaces

The rising focus on employee health and productivity has led to greater demand for ergonomic solutions like LCD monitor arms, which help prevent musculoskeletal disorders by allowing customizable screen positioning. This trend is particularly prominent in corporate offices where prolonged screen time is common, driving companies to equip workstations with adjustable arms to comply with occupational health standards and improve overall work efficiency.

Additionally, the shift toward remote work has extended this demand to home setups, where individuals seek professional-grade ergonomics without permanent fixtures. Technological advancements in arm designs, such as gas spring mechanisms for smooth adjustments, further support market growth by offering durable and user-friendly options that integrate seamlessly with modern LCD monitors.

Restraints

- High Cost of Premium Products

Quality LCD monitor arms with advanced features like multi-monitor support and heavy-duty construction can be expensive, limiting adoption among budget-conscious consumers and small enterprises. This price barrier often leads to preferences for cheaper alternatives or makeshift solutions, which may not provide the same level of durability or ergonomic benefits, thereby slowing overall market penetration in price-sensitive regions.

Moreover, the availability of low-cost, inferior products from unbranded manufacturers can undermine trust in the market, as these items frequently fail prematurely, leading to negative user experiences. Compatibility issues with varying monitor sizes and weights also restrain growth, as users hesitate to invest in arms that may not suit their specific setups without additional modifications.

Opportunities

- Expansion in Emerging Markets

Rapid urbanization and the growth of IT sectors in developing regions present opportunities for LCD monitor arm manufacturers to tap into new customer bases through affordable, entry-level products. As co-working spaces and startups proliferate, there is potential for customized solutions that address space constraints and multi-device usage, fostering partnerships with local distributors to build market presence.

Furthermore, innovations in sustainable materials and eco-friendly designs can attract environmentally conscious buyers, while integrations with smart office technologies like IoT-enabled adjustments offer differentiation. Collaborations with monitor brands for bundled offerings could also expand reach, capitalizing on the increasing digitalization in education and healthcare sectors across these markets.

Challenges

- Intense Market Competition

The LCD monitor arm market faces stiff competition from numerous players, leading to price wars and margin pressures that challenge profitability for established brands. Differentiating products in a saturated space requires continuous R&D investment, which smaller firms may struggle with, resulting in market consolidation favoring larger entities with stronger supply chains.

Supply chain disruptions, such as raw material shortages or logistical issues, exacerbate challenges by increasing production costs and delaying deliveries. Evolving consumer preferences toward portable devices like laptops reduce the need for fixed monitor arms, pushing manufacturers to innovate hybrid solutions that accommodate both traditional and mobile setups to remain relevant.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.82 Billion |

Projected Market Size in 2034 |

USD 2.84 Billion |

CAGR Growth Rate |

4.7% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Ergotron Inc., Humanscale, Herman Miller, Inc., Loctek Ergonomic Technology Corp., Colebrook Bosson Saunders (CBS), North Bayou, Atdec Pty Ltd., Eastern Global Corporation, Modernsolid Industrial Co. Ltd., Highgrade Tech. Co. Ltd., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The LCD monitor arm market is segmented by type, application, end-user, and region.

Based on Type Segment, the LCD monitor arm market is divided into single monitor arm, dual monitor arm, multi-monitor arm. The most dominant segment is the single monitor arm, which leads due to its affordability, simplicity, and widespread applicability in standard desk environments where users typically operate with one screen; this dominance drives the market by catering to entry-level consumers and small offices, enabling broader accessibility and encouraging upgrades to more advanced models as needs evolve. The second most dominant is the dual monitor arm, favored for its ability to support multitasking in professional settings like graphic design or data analysis, helping to boost productivity and market growth through enhanced workflow efficiency in mid-sized enterprises.

Based on Application Segment, the LCD monitor arm market is divided into office, healthcare, education, others. The most dominant segment is office, which excels because of the global rise in desk-based jobs and hybrid work cultures demanding flexible screen adjustments to reduce fatigue; this drives the market by integrating with corporate wellness programs, promoting sustained demand and innovation in space-saving designs. The second most dominant is healthcare, where arms facilitate precise monitor positioning in diagnostic and monitoring stations, enhancing accuracy and comfort for medical staff, thereby contributing to market expansion through specialized applications in hospitals and clinics.

Based on End-User Segment, the LCD monitor arm market is divided into commercial, residential, industrial. The most dominant segment is commercial, leading owing to large-scale deployments in businesses focused on ergonomic compliance and employee retention; this propels market growth by standardizing arms in office infrastructures, fostering bulk purchases and long-term contracts. The second most dominant is residential, growing from home office trends where individuals prioritize personal comfort, aiding market development by expanding consumer access through online retail and affordable options tailored for compact living spaces.

Recent Developments

- In April 2023, INOVATIV introduced its versatile Monitor Arm Systems at the National Association of Broadcasters event, featuring VESA compatibility, support for weights up to 55 lb, 360° rotation, and smooth tilt and pan adjustments, aimed at enhancing workstation flexibility in broadcasting and creative industries.

- In November 2022, Portwell Technology launched a new series of medical-grade touch monitors and all-in-one computers with widescreen LCD options, designed for easy VESA mounting and compatibility with desktop stands, boosting demand for complementary LCD monitor arms in healthcare settings.

- In early 2025, Ergotron unveiled an updated line of gas spring monitor arms with integrated cable management and sustainable aluminum construction, targeting eco-conscious corporate clients and addressing the growing need for durable, adjustable solutions in hybrid work environments.

Regional Analysis

- North America to dominate the global market

North America maintains a leading position in the LCD monitor arm market, driven by advanced technological infrastructure and a strong emphasis on workplace health in countries like the United States. The region's dominance stems from widespread corporate adoption of ergonomic tools to comply with labor laws, coupled with high disposable incomes enabling premium purchases. Innovation hubs in the US foster product development, while Canada's growing tech sector adds momentum. This area benefits from robust e-commerce channels and awareness campaigns on posture-related issues, ensuring steady demand across offices and homes.

Europe follows closely, with countries such as Germany and the UK prioritizing stringent health and safety regulations that mandate ergonomic setups in professional environments. The market thrives on sustainable manufacturing practices and integrations with smart office systems, appealing to eco-aware consumers. Scandinavia's focus on work-life balance further boosts adoption in education and healthcare, where adjustable arms enhance user experience. Economic stability supports investments in high-quality products, while EU-wide initiatives promote wellness, driving consistent growth in both commercial and residential segments.

Asia Pacific emerges as a high-growth region, led by China's massive manufacturing base and India's expanding IT industry, where rapid urbanization fuels demand for space-efficient solutions. Japan's technological prowess contributes through innovative designs, while Southeast Asian nations like Singapore adopt arms for modern co-working spaces. Low production costs enable affordable exports, attracting global buyers, and rising middle-class incomes spur residential uptake. Government pushes for digital economies amplify the need for ergonomic accessories in bustling urban centers.

Latin America shows promising potential, with Brazil as the key driver through its burgeoning corporate sector and increasing remote work trends. Mexico's proximity to North American markets facilitates trade, introducing advanced products to local users. The region grapples with economic variability but gains from affordable imports and growing awareness of health benefits. Investments in infrastructure, particularly in urban areas, support adoption in offices and educational institutions, paving the way for gradual expansion amid improving living standards.

The Middle East & Africa region experiences steady progress, dominated by the UAE's modern business hubs and South Africa's tech-savvy workforce. Saudi Arabia's Vision 2030 initiatives promote ergonomic workspaces in new developments, while Africa's youthful population drives educational applications. Challenges like infrastructure gaps persist, but oil-rich nations invest in premium setups for corporate environments. Growing tourism and hospitality sectors in the Middle East further integrate arms for efficient operations, fostering niche growth opportunities.

Competitive Analysis

The global LCD monitor arm market is dominated by players:

- Ergotron Inc.

- Humanscale

- Herman Miller, Inc.

- Loctek Ergonomic Technology Corp.

- Colebrook Bosson Saunders (CBS)

- North Bayou

- Atdec Pty Ltd.

- Eastern Global Corporation

- Modernsolid Industrial Co. Ltd.

- Highgrade Tech. Co. Ltd.

- And Others.

The global LCD monitor arm market is segmented as follows:

By Type

- Single Monitor Arm

- Dual Monitor Arm

- Multi-Monitor Arm

By Application

- Office

- Healthcare

- Education

- Others

By End-User

- Commercial

- Residential

- Industrial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global LCD monitor arm market is dominated by players:

- Ergotron Inc.

- Humanscale

- Herman Miller, Inc.

- Loctek Ergonomic Technology Corp.

- Colebrook Bosson Saunders (CBS)

- North Bayou

- Atdec Pty Ltd.

- Eastern Global Corporation

- Modernsolid Industrial Co. Ltd.

- Highgrade Tech. Co. Ltd.

- Others.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors