![]()

Search Market Research Report

Third-Party Optical Transceivers Market Size, Share Global Analysis Report, 2026 - 2034-

Third-Party Optical Transceivers Market Size, Share, Growth Analysis Report By Form Factor (SFP, SFP+, QSFP/QSFP+, XFP, CFP, and Others), By Data Rate (Up to 10 Gbps, 10–40 Gbps, 41–100 Gbps, Above 100 Gbps), By Application (Data Centers, Telecommunication, Enterprise Networks, Cloud Providers, Wireless Networks, and Others), By End-User (IT & Telecom, BFSI, Government, Education, Healthcare, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026 - 2034-

Industry Insights

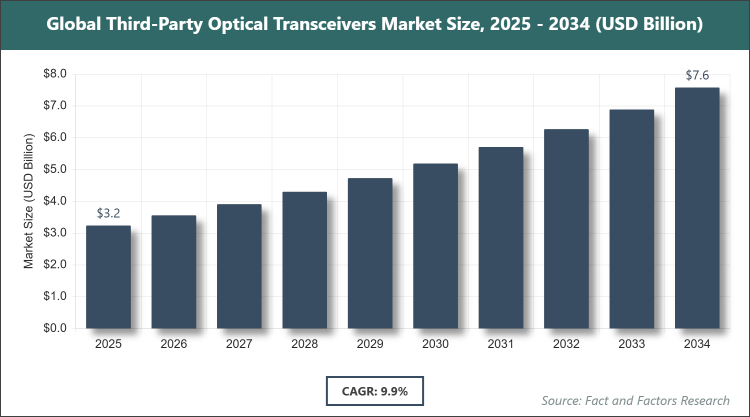

[238+ Pages Report] According to Facts & Factors, the global Third-Party Optical Transceivers market size was estimated at USD 3.24 billion in 2025 and is expected to reach USD 8.33 billion by the end of 2034. The Third-Party Optical Transceivers industry is anticipated to grow by a CAGR of 9.9% between 2026 and 2034. The Third-Party Optical Transceivers Market is driven by escalating demand for cost-effective high-speed data transmission solutions.

Market Overview

Market Overview

Third-party optical transceivers refer to compatible networking modules produced by vendors other than original equipment manufacturers, enabling data transmission over fiber optic networks at reduced costs while meeting industry standards for interoperability and performance in applications such as data centers, telecommunications, and enterprise networks, without incorporating quantitative data in this foundational description.

Key Insights

- As per the analysis shared by our research analyst, the global Third-Party Optical Transceivers market is estimated to grow annually at a CAGR of around 9.9% over the forecast period (2026-2034).

- In terms of revenue, the global Third-Party Optical Transceivers market size was valued at around USD 3.24 billion in 2025 and is projected to reach USD 8.33 billion by 2034.

- The market is driven by rising adoption of cloud computing and 5G networks requiring high-bandwidth solutions.

- Based on the Form Factor, the QSFP/QSFP+ segment dominated the market in 2025 with a share of 44%, due to its support for high-speed data rates in data centers and telecom applications.

- Based on the Data Rate, the Above 100 Gbps segment dominated the market in 2025 with a share of over 35%, attributed to the surge in demand for ultra-high-speed connectivity in AI and cloud infrastructures.

- Based on the Application, the Data Centers segment dominated the market in 2025 with a share of over 40%, owing to the expansion of hyperscale facilities and need for efficient interconnects.

- Based on the End-User, the IT & Telecom segment dominated the market in 2025 with a share of around 45%, driven by rapid 5G deployments and network upgrades.

- Based on the region, Asia Pacific dominated the market in 2025 with a share of around 40%, fueled by rapid digital transformation and massive investments in telecom infrastructure in countries like China and India.

Growth Drivers

- Rising Demand for High-Speed Data Transmission

The relentless push for higher bandwidth in data centers and telecommunications networks is a primary catalyst, as third-party transceivers offer affordable alternatives to OEM products while supporting advanced speeds like 400G and beyond. This affordability enables broader adoption among small to medium enterprises, facilitating seamless upgrades to fiber optic infrastructures without prohibitive costs.

Technological advancements in transceiver design, such as improved compatibility and energy efficiency, further accelerate market penetration, allowing integration into diverse network environments and supporting the global shift towards digital economies reliant on real-time data exchange.

Restraints

- Compatibility and Warranty Concerns

Potential interoperability issues with proprietary equipment from major vendors can hinder adoption, as network operators fear voided warranties or system failures, leading to reluctance in shifting from OEM solutions. This uncertainty often results in extended evaluation periods and increased testing costs, slowing market expansion.

Supply chain vulnerabilities, including component shortages and geopolitical tensions affecting raw material availability, compound these issues, potentially causing delays in deployment and elevating prices, which disproportionately impact budget-conscious buyers in emerging markets.

Opportunities

- Expansion of 5G and Cloud Infrastructure

The global rollout of 5G networks and the proliferation of cloud services create avenues for third-party transceivers to fill gaps in high-volume deployments, offering scalable, cost-effective options for operators expanding coverage. Innovations in multi-vendor compatibility open doors for partnerships and custom solutions tailored to specific regional needs.

Sustainability trends favoring energy-efficient optics align with environmental regulations, positioning third-party providers to capture market share through eco-friendly designs that reduce power consumption in large-scale installations, attracting environmentally conscious enterprises.

Challenges

- Stringent Regulatory and Quality Standards

Compliance with international standards for performance and safety poses significant hurdles, as varying regional regulations require extensive certification processes that increase operational costs for manufacturers. Failure to meet these can lead to market exclusion or legal repercussions, particularly in highly regulated sectors like healthcare and government.

Intensifying competition from OEMs, enhancing their own compatible line,s threatens market share, while intellectual property disputes over transceiver coding and firmware could result in litigation, diverting resources from innovation and growth initiatives.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 3.24 Billion |

Projected Market Size in 2034 |

USD 8.33 Billion |

CAGR Growth Rate |

9.9% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Finisar Corporation, Cisco Systems Inc., Lumentum Holdings Inc., Juniper Networks Inc., Mellanox Technologies, Sumitomo Electric Industries Ltd., Accelink Technologies Co. Ltd., Foxconn Interconnect Technology, Hisense Broadband Multimedia Technologies Co. Ltd., Source Photonics Inc., and Others. |

Key Segment |

By Form Factor, By Data Rate, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Third-Party Optical Transceivers market is segmented by form factor, data rate, application, end-user, and region.

Based on Form Factor Segment, the Third-Party Optical Transceivers market is divided into SFP, SFP+, QSFP/QSFP+, XFP, CFP, and Others. The most dominant segment is QSFP/QSFP+, holding over 44% share, due to its ability to handle high-density, high-speed connections essential for modern data centers, driving the market by enabling efficient scaling of bandwidth-intensive applications like AI and video streaming; the second most dominant is SFP/SFP+, appreciated for its versatility in enterprise and telecom networks, contributing to growth through cost-effective upgrades in legacy systems and support for diverse transmission distances.

Based on Data Rate Segment, the Third-Party Optical Transceivers market is divided into Up to 10 Gbps, 10–40 Gbps, 41–100 Gbps, and Above 100 Gbps. The most dominant segment is Above 100 Gbps, with over 35% share, as it caters to the exploding need for ultra-fast data transfer in hyperscale environments, propelling the market forward by facilitating advanced technologies such as 5G and cloud computing; the second most dominant is 41–100 Gbps, which balances performance and cost for mid-tier applications, aiding market expansion through widespread adoption in enterprise networking and metro access.

Based on Application Segment, the Third-Party Optical Transceivers market is divided into Data Centers, Telecommunication, Enterprise Networks, Cloud Providers, Wireless Networks, and Others. The most dominant segment is Data Centers, capturing over 40% share, owing to the surge in global data traffic and need for high-performance interconnects, fueling market growth by supporting efficient, scalable infrastructure for big data and AI workloads; the second most dominant is Telecommunication, driven by 5G expansions requiring reliable high-speed links, advancing the market through enhanced connectivity in mobile and broadband services.

Based on End-User Segment, the Third-Party Optical Transceivers market is divided into IT & Telecom, BFSI, Government, Education, Healthcare, and Others. The most dominant segment is IT & Telecom, with around 45% share, due to its critical role in enabling seamless data transmission for network operators, driving the market by meeting the demands of digital transformation and high-speed internet; the second most dominant is BFSI, where secure and fast data handling is paramount, contributing to growth through applications in financial transactions and data security.

Recent Developments

- In November 2023, Lumentum Operations LLC acquired Cloud Light Technology Limited for approximately USD 750 million, enhancing its capabilities in high-speed optical modules for cloud data centers.

- In September 2023, Tower Semiconductor and InnoLight Technology collaborated to develop multi-generation high-speed optical transceivers using Tower’s Silicon Photonics platform.

- In March 2023, Eoptolink Technology Inc., Ltd. launched Multimode BIDI Transceivers in 100G, 400G, and 800G versions, facilitating upgrades without replacing existing fiber infrastructure.

- In 2023, Amphenol ICC acquired Finisar Corporation, strengthening its portfolio in optical components and modules.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific emerges as a frontrunner in the third-party optical transceivers arena, bolstered by expansive telecommunications growth and a thriving e-commerce sector that demands robust data handling capabilities. China stands out as the dominating country, with its massive investments in 5G infrastructure and data center expansions fueling innovation and adoption of cost-effective transceiver solutions. The region's dynamic tech ecosystem, coupled with supportive government policies promoting digital connectivity, creates a fertile ground for market players to explore diverse applications from urban broadband to rural network enhancements.

North America maintains a strong foothold through its advanced technological landscape and emphasis on high-performance networking, with the United States leading as the dominating country via its concentration of hyperscale data centers and cutting-edge R&D facilities. This area thrives on a culture of innovation, where enterprises prioritize scalable and interoperable solutions to support cloud computing and AI-driven operations.

Europe exhibits resilience with its focus on regulatory compliance and sustainable practices, positioning Germany as the dominating country through its engineering prowess and commitment to high-quality manufacturing standards. The continent's integrated approach to digital infrastructure underscores a balanced strategy encompassing both traditional telecom and emerging IoT applications.

Latin America is gaining momentum amid increasing digital inclusion efforts and foreign investments, with Brazil as the dominating country leveraging its large population and growing tech hubs to advance network capabilities. This region capitalizes on economic diversification to bridge connectivity gaps in urban and remote areas alike.

The Middle East & Africa region is progressively advancing, driven by strategic infrastructure projects and oil-rich economies transitioning to digital diversification, with the United Arab Emirates leading as the dominating country through its visionary smart city initiatives and global trade connectivity. This area focuses on harnessing transceiver technologies to support expansive wireless networks and enterprise solutions.

Competitive Analysis

The global Third-Party Optical Transceivers market is dominated by players:

- Finisar Corporation

- Cisco Systems Inc.

- Lumentum Holdings Inc.

- Juniper Networks Inc.

- Mellanox Technologies

- Sumitomo Electric Industries Ltd.

- Accelink Technologies Co. Ltd.

- Foxconn Interconnect Technology

- Hisense Broadband Multimedia Technologies Co. Ltd.

- Source Photonics Inc.

The global Third-Party Optical Transceivers market is segmented as follows:

By Form Factor

- SFP

- SFP+

- QSFP/QSFP+

- XFP

- CFP

- Others

By Data Rate

- Up to 10 Gbps

- 10–40 Gbps

- 41–100 Gbps

- Above 100 Gbps

By Application

- Data Centers

- Telecommunication

- Enterprise Networks

- Cloud Providers

- Wireless Networks

- Others

By End-User

- IT & Telecom

- BFSI

- Government

- Education

- Healthcare

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Finisar Corporation

- Cisco Systems Inc.

- Lumentum Holdings Inc.

- Juniper Networks Inc.

- Mellanox Technologies

- Sumitomo Electric Industries Ltd.

- Accelink Technologies Co. Ltd.

- Foxconn Interconnect Technology

- Hisense Broadband Multimedia Technologies Co. Ltd.

- Source Photonics Inc.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors