![]()

Search Market Research Report

Phytosterols Market Size, Share Global Analysis Report, 2026-2034

Phytosterols Market Size, Share, Growth Analysis Report By Type (Beta-Sitosterol, Campesterol, Stigmasterol, and Others), By Application (Food and Beverages, Pharmaceuticals, Cosmetics, Dietary Supplements, and Others), By End-User (Food Industry, Pharmaceutical Industry, Cosmetic Industry, Feed Industry, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

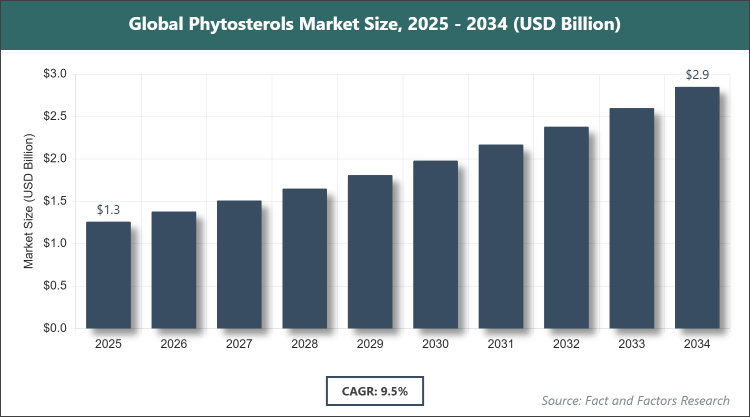

[220+ Pages Report] According to Facts & Factors, the global phytosterols market size was estimated at USD 1.26 billion in 2025 and is expected to reach USD 2.79 billion by the end of 2034. The phytosterols industry is anticipated to grow by a CAGR of 9.5% between 2026 and 2034. The phytosterols Market is driven by increasing demand for functional foods and rising awareness of cardiovascular health benefits.

Market Overview

Market Overview

Phytosterols are naturally occurring compounds found in plants that structurally resemble cholesterol and are known for their ability to lower cholesterol levels in humans by inhibiting its absorption in the intestines. These plant sterols are widely utilized in various industries, including food and beverages, pharmaceuticals, and cosmetics, to enhance product functionality and promote health benefits such as cardiovascular support and anti-inflammatory properties.

Key Insights

- As per the analysis shared by our research analyst, the phytosterols market is estimated to grow annually at a CAGR of around 9.5% over the forecast period (2026-2034).

- In terms of revenue, the phytosterols market was valued at USD 1.26 Billion in 2025 and is expected to reach USD 2.79 Billion by 2034.

- The market is driven by increasing consumer awareness regarding cardiovascular health and the benefits of plant-based sterols.

- Based on the type, Beta-Sitosterol accounted for largest market share of over 50% in 2025 due to its high efficacy in cholesterol reduction and widespread incorporation in functional foods and supplements.

- Based on the application, Food and Beverages dominated with a share of around 45% in 2025 owing to the growing demand for fortified products like margarines, yogurts, and dairy alternatives that promote heart health.

- Based on the end-user, Food Industry held the leading share of approximately 40% in 2025 because of its extensive use in processed foods to meet consumer preferences for natural, health-enhancing ingredients.

- Europe dominated the market with more than 50% share in 2025 owing to stringent food safety regulations and high consumer focus on preventive healthcare.

Growth Drivers

- Increasing Awareness of Cardiovascular Health Benefits

The rising global incidence of heart-related ailments has heightened consumer focus on preventive measures, positioning phytosterols as a key ingredient in cholesterol management strategies. Educational campaigns by health organizations and governments have amplified knowledge about how phytosterols block cholesterol absorption, leading to broader adoption in daily diets.

This awareness is further bolstered by clinical studies validating phytosterols' efficacy, encouraging manufacturers to innovate and integrate them into everyday products. As a result, the market sees sustained demand from health-conscious demographics, particularly in aging populations seeking natural alternatives to pharmaceuticals.

- Rising Demand for Functional Foods and Nutraceuticals

Consumers are increasingly seeking foods that offer additional health benefits beyond basic nutrition, driving the incorporation of phytosterols in items like spreads, cereals, and beverages. This trend is supported by the clean-label movement, where natural plant-derived ingredients are preferred over synthetic additives.

The expansion of the nutraceutical sector, fueled by e-commerce and retail channels, has made phytosterol-enriched products more accessible, contributing to market growth. Innovations in formulation techniques ensure stability and bioavailability, enhancing product appeal and market penetration.

Restraints

- High Production Costs and Supply Chain Volatility

Extracting phytosterols from sources like vegetable oils involves complex processes, leading to elevated manufacturing expenses that can hinder affordability and market expansion. Fluctuations in raw material prices, influenced by agricultural yields and global trade dynamics, add to these challenges.

These cost factors often result in higher end-product prices, limiting accessibility in price-sensitive emerging markets. Additionally, dependency on specific plant sources exposes the supply chain to risks from climate changes and geopolitical issues, potentially disrupting steady market growth.

- Stringent Regulatory Approvals and Labeling Requirements

Navigating diverse international regulations for health claims and ingredient approvals can delay product launches and increase compliance costs for manufacturers. Variations in acceptable daily intake levels and labeling standards across regions create barriers to global expansion.

Such restraints may slow innovation as companies invest heavily in research to meet safety and efficacy proofs. This regulatory landscape also favors established players, potentially stifling competition from smaller entrants and affecting overall market dynamism.

Opportunities

- Expansion in Emerging Markets of Asia-Pacific

Rapid urbanization and rising disposable incomes in Asia-Pacific countries are creating new avenues for phytosterol adoption, particularly in functional foods tailored to local tastes. Growing health awareness amid lifestyle diseases opens doors for targeted marketing and product localization.

Partnerships with regional suppliers can optimize supply chains, reducing costs and enhancing market entry. This region's untapped potential, combined with government initiatives promoting healthy eating, positions it for significant growth contributions.

- Innovations in Extraction and Application Technologies

Advancements in sustainable extraction methods, such as enzymatic processes, promise to lower costs and improve yield efficiency, attracting investment in R&D. New applications in cosmetics and animal feed expand the market beyond traditional uses, diversifying revenue streams.

These innovations also address bioavailability challenges, enabling novel product formats like gummies and powders. As technology evolves, it fosters collaborations between academia and industry, accelerating market evolution.

Challenges

- Competition from Alternative Cholesterol-Lowering Agents

The presence of substitutes like stanols, omega-3s, and prescription drugs poses a threat, as consumers may opt for these based on perceived efficacy or familiarity. Differentiating phytosterols requires robust marketing and evidence-based claims to maintain market share.

This competition intensifies in saturated segments like supplements, where innovation is key to retention. Economic downturns could further shift preferences toward cheaper alternatives, challenging phytosterol positioning.

- Limited Raw Material Availability and Sustainability Concerns

Over-reliance on specific crops for phytosterol sourcing raises sustainability issues, including deforestation and biodiversity loss, prompting scrutiny from eco-conscious consumers. Ensuring ethical sourcing adds complexity to operations.

Climate variability impacts crop quality and quantity, potentially leading to shortages. Addressing these through diversified sourcing and sustainable practices is essential but requires long-term investments.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.26 Billion |

Projected Market Size in 2034 |

USD 2.79 Billion |

CAGR Growth Rate |

9.5% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BASF SE, Cargill Incorporated, Archer Daniels Midland Company (ADM), Raisio Plc, Bunge Limited, DuPont (IFF), Wilmar International Ltd., Arboris LLC, Kensing LLC, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The phytosterols market is segmented by type, application, end-user, and region.

Based on Type Segment, the phytosterols market is divided into Beta-Sitosterol, Campesterol, Stigmasterol, and others. Beta-Sitosterol emerges as the most dominant segment, holding over 50% market share, primarily due to its superior cholesterol-blocking properties and versatility in formulations, which drives demand in health-focused products. Campesterol follows as the second most dominant, valued for its complementary role in blends that enhance overall efficacy, contributing to market growth by enabling customized solutions for specific health needs.

Based on Application Segment, the phytosterols market is divided into Food and Beverages, Pharmaceuticals, Cosmetics, Dietary Supplements, and others. Food and Beverages is the most dominant segment with around 45% share, as it leverages phytosterols for fortification in everyday consumables, boosting heart health claims and driving sales through consumer preference for functional edibles. Pharmaceuticals ranks second, benefiting from clinical applications in drug development, which propels market expansion by addressing therapeutic needs in cardiovascular treatments.

Based on End-User Segment, the phytosterols market is divided into Food Industry, Pharmaceutical Industry, Cosmetic Industry, Feed Industry, and others. The Food Industry dominates with approximately 40% share, owing to its large-scale integration of phytosterols in processed foods to meet regulatory health standards and consumer demands for natural additives, significantly fueling overall market momentum. The Pharmaceutical Industry is the second dominant, utilizing phytosterols in formulations for targeted health interventions, thereby enhancing market growth through innovation in medical applications.

Recent Developments

- In December 2025, BASF agreed to sell its Food & Health Performance Ingredients unit, including the Illertissen site in Germany, to Louis Dreyfus Company, as part of BASF’s strategy to optimize its portfolio and focus on core businesses while enabling the unit to thrive under new ownership specialized in agricultural commodities.

- In August 2024, Elicit Plant gained global traction with its EliTerra technology, which uses phytosterols to boost crop stress resistance and reduce water usage by up to 20%, expanding rapidly across major farming regions and highlighting phytosterols' role in sustainable agriculture.

- In May 2024, Kensing acquired Vitae Naturals and Advanced Organic Materials (AOM) to produce plant-based phytosterols and vitamin E from non-GMO, deforestation-free sources like soy, sunflower, and rapeseed, strengthening its position in natural ingredients for food and personal care.

- In September 2023, Nutrartis launched Cardiosmile, a plant sterol supplement in the U.S., designed to reduce LDL cholesterol and triglycerides, capitalizing on the health benefits of phytosterols to target consumers seeking convenient heart health solutions.

Regional Analysis

- Europe to dominate the global market

Europe continues to lead the phytosterols market due to its advanced regulatory framework that supports health claims on food labels, encouraging widespread adoption in fortified products. The region's emphasis on preventive healthcare, coupled with a mature food industry, fosters innovation in phytosterol applications. Germany stands out as the dominating country, with its strong pharmaceutical and food manufacturing sectors driving research and production, while consumer trust in science-backed ingredients sustains demand across diverse demographics.

North America exhibits robust growth in the phytosterols market, driven by increasing health consciousness and a surge in lifestyle-related diseases prompting dietary shifts. The United States dominates this region, benefiting from a vast consumer base and extensive retail networks that promote functional foods and supplements. Ongoing R&D investments by key players enhance product efficacy, while marketing campaigns highlighting natural cholesterol management appeal to health-savvy populations, ensuring steady market expansion.

Asia-Pacific is emerging as a high-potential area for phytosterols, fueled by rapid urbanization and evolving dietary habits towards healthier options. China leads as the dominating country, with its massive population and growing middle class demanding plant-based health solutions amid rising cardiovascular concerns. Local manufacturers are adapting phytosterols into traditional foods, supported by government initiatives on nutrition, which accelerates adoption and positions the region for significant future contributions.

Latin America shows promising developments in the phytosterols market, influenced by improving economic conditions and greater access to health information. Brazil dominates here, leveraging its agricultural strengths to source raw materials efficiently while addressing public health challenges like obesity. The integration of phytosterols in affordable food products resonates with consumers, and partnerships with international firms bring technological advancements, enhancing market penetration.

The Middle East & Africa region is gradually incorporating phytosterols, driven by urbanization and exposure to global health trends. South Africa emerges as the dominating country, with its developed food processing industry facilitating the inclusion of phytosterols in everyday items. Efforts to combat non-communicable diseases through better nutrition policies support growth, though challenges in distribution persist, the focus on affordable, natural ingredients promises progressive expansion.

Competitive Analysis

The global phytosterols market is dominated by players:

- BASF SE

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- Raisio Plc

- Bunge Limited

- DuPont (IFF)

- Wilmar International Ltd.

- Arboris LLC

- Kensing LLC

- And Others

The global phytosterols market is segmented as follows:

By Type

- Beta-Sitosterol

- Campesterol

- Stigmasterol

- Others

By Application

- Food and Beverages

- Pharmaceuticals

- Cosmetics

- Dietary Supplements

- Others

By End-User

- Food Industry

- Pharmaceutical Industry

- Cosmetic Industry

- Feed Industry

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global phytosterols market is dominated by players:

- BASF SE

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- Raisio Plc

- Bunge Limited

- DuPont (IFF)

- Wilmar International Ltd.

- Arboris LLC

- Kensing LLC

- Others

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors