![]()

Search Market Research Report

Home Elevator Market Size, Share Global Analysis Report, 2026-2034

Home Elevator Market Size, Share, Growth Analysis Report By Type (Hydraulic, Traction, Machine Room-Less, Pneumatic, and Others), By Application (New Construction and Retrofit), By End-User (Single-Family Homes, Multi-Family Homes, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

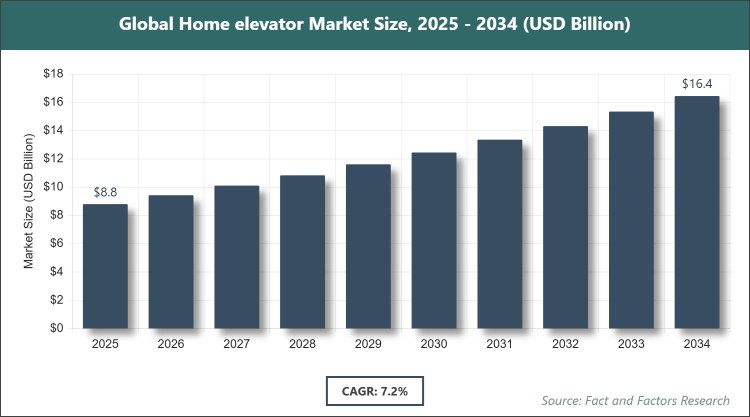

[233 Pages Report] According to Facts & Factors, the global Home elevator market size was estimated at USD 8.8 billion in 2025 and is expected to reach USD 17.5 billion by the end of 2034. The Home elevator industry is anticipated to grow by a CAGR of 7.2% between 2026 and 2034. The Home elevator Market is driven by rising demand for accessibility solutions in multi-story private residences and increasing luxury home construction worldwide.

Market Overview

Market Overview

The Home elevator market covers specialized vertical transportation systems installed in private residences to provide convenient, safe, and accessible movement between floors. These compact elevators are engineered for low- to mid-rise homes, incorporating quiet operation, space-saving designs, elegant finishes, and advanced safety features such as emergency brakes, battery backups, and obstruction sensors. Available in hydraulic, traction, machine-room-less, and pneumatic configurations, home elevators cater to aging homeowners seeking to age in place, families with mobility challenges, and luxury property owners desiring enhanced convenience and property value. The market emphasizes customization, energy efficiency, and seamless integration with smart home systems, transforming multi-level living into an inclusive and comfortable experience while complying with residential building codes and accessibility standards.

Key Insights

- As per the analysis shared by our research analyst, the Home elevator market is estimated to grow annually at a CAGR of around 7.2% over the forecast period (2026-2034).

- In terms of revenue, the Home elevator market size was valued at around USD 8.8 billion in 2025 and is projected to reach USD 17.5 billion by 2034.

- The Home elevator Market is driven by an aging population and a luxury residential construction boom.

- Based on the Type, the Hydraulic segment dominated the market in 2025 with a share of 52% due to lower installation costs, smooth ride quality, and suitability for low-rise single-family homes.

- Based on the Application, the Retrofit segment dominated the market in 2025 with a share of 58%, owing tothe renovation of existing multi-story homes for accessibility and modern living.

- Based on the End-User, the Single-Family Homes segment dominated the market in 2025 with a share of 68% because private homeowners prioritize personalized luxury and aging-in-place solutions.

- North America dominated the global Home elevator market in 2025 with a share of 37%, attributed to high disposable incomes, strong focus on home accessibility, and premium residential construction activity.

Growth Drivers

- Aging Population and Accessibility Needs

Increasing life expectancy and the desire to age in place have prompted homeowners to install elevators that eliminate stair-climbing barriers, particularly for seniors with reduced mobility.

Supportive government incentives and universal design trends in residential architecture further accelerate adoption in both new builds and renovations.

Restraints

- High Installation and Maintenance Costs

Custom engineering, structural modifications, and premium safety features result in significant upfront expenses that deter budget-conscious buyers in mid-range housing segments.

Ongoing service contracts and periodic inspections add to lifetime ownership costs, slowing penetration in price-sensitive markets.

Opportunities

- Smart Home Integration and Luxury Customization

Advancements in IoT connectivity, voice control, and energy-efficient drives allow home elevators to become seamless extensions of smart homes, appealing to tech-savvy luxury buyers.

Rising demand for compact pneumatic and machine-room-less models in space-constrained urban villas creates new growth avenues for manufacturers.

Challenges

- Regulatory Compliance and Space Constraints

Varying local building codes, safety certifications, and structural requirements complicate installations, especially in older homes with limited shaft space.

Supply chain disruptions for specialized components and skilled installer shortages extend project timelines and raise costs.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 8.8 Billion |

Projected Market Size in 2034 |

USD 17.5 Billion |

CAGR Growth Rate |

7.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Otis Elevator Company, Schindler Group, KONE Corporation, Thyssenkrupp Elevator, Mitsubishi Electric Corporation, Fujitec Co., Ltd., Cibes Lift Group, Kalea Lifts, Nibav Lifts, Waupaca Elevator Company, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Home elevator market is segmented by type, application, end-user, and region.

Based on Type Segment, the Home elevator market is divided into hydraulic, traction, machine room-less, pneumatic, and others. The most dominant segment is Hydraulic, valued for cost-effectiveness in low-rise applications. The second most dominant is Machine Room-Less. Hydraulic dominates due to reliable performance, minimal structural demands, and lower initial investment, helping drive market growth by making home elevators accessible to a broader range of single-family homeowners seeking practical accessibility upgrades.

Based on Application Segment, the Home elevator market is divided into new construction and retrofit. The most dominant segment is Retrofit, supported by the renovation of existing multi-level homes. The second most dominant is New Construction. Retrofit leads because many homeowners upgrade older properties for modern accessibility and resale value, propelling market expansion through faster project turnaround and strong aftermarket demand for elegant, space-efficient solutions.

Based on the End-User Segment, the Home elevator market is divided into single-family homes, multi-family homes, and others. The most dominant segment is Single-Family Homes, driven by personalized luxury installations. The second most dominant is Multi-Family Homes. Single-Family Homes dominate due to higher customization budgets and direct owner decision-making, driving market growth by fueling premium feature adoption and repeat business through word-of-mouth in affluent residential communities.

Recent Developments

- In February 2026, Otis Elevator Company introduced a new compact machine-room-less home elevator series with enhanced voice-activated controls and energy-saving regenerative drives.

- In November 2025, Schindler Group launched its Schindler Home platform featuring AI-based predictive maintenance for residential elevators in luxury villas.

- In September 2025, Kalea Lifts expanded its European footprint with a new pneumatic vacuum elevator model designed for narrow shafts in historic homes.

- In June 2025, Cibes Lift Group partnered with smart home integrators to offer fully app-controlled cylinder-driven home elevators across North America.

- In April 2025, Nibav Lifts unveiled its latest panoramic glass home elevator with IoT integration and solar-ready power options for eco-conscious buyers.

Regional Analysis

- North America to dominate the global market

North America leads the Home elevator market through high per-capita wealth, strong emphasis on universal design, and a mature luxury residential sector that values convenience and property enhancement. The region excels in customization and rapid adoption of smart technologies. The United States dominates within North America, benefiting from a large base of multi-story suburban homes, aging baby boomers seeking independence, and favorable tax incentives for accessibility modifications that encourage widespread installation in both new luxury builds and existing properties.

Europe holds a prominent position in the Home elevator market, supported by strict accessibility regulations and cultural preference for elegant architectural integration. Collaborative design standards promote aesthetically pleasing solutions. Germany leads the region, with its engineering precision and focus on energy-efficient systems enabling sophisticated installations in both modern villas and heritage renovations, while strong after-sales service networks ensure long-term reliability.

Asia Pacific is witnessing accelerated growth in the Home elevator market, driven by rising affluent urban households and rapid high-rise villa development in China, Japan, and South Korea. Government policies promoting barrier-free housing further stimulate demand. China dominates, leveraging its massive real estate sector and growing middle-to-upper class to introduce affordable yet feature-rich home elevators, supported by domestic manufacturing scale and export capabilities.

Latin America shows emerging expansion in the Home elevator market, fueled by increasing luxury home construction and awareness of mobility solutions. Brazil leads, with its vibrant high-end residential market adopting hydraulic and traction models to cater to multi-level properties in gated communities and coastal villas.

The Middle East & Africa region demonstrates strong potential in the Home elevator market, aligned with ambitious luxury real estate projects and smart-city developments. The United Arab Emirates leads, incorporating advanced home elevators into ultra-luxury villas and high-end apartments as standard features that enhance livability and property prestige.

Competitive Analysis

The global Home elevator market is dominated by players:

- Otis Elevator Company

- Schindler Group

- KONE Corporation

- Thyssenkrupp Elevator

- Mitsubishi Electric Corporation

- Fujitec Co., Ltd.

- Cibes Lift Group

- Kalea Lifts

- Nibav Lifts

- Waupaca Elevator Company

The global Home elevator market is segmented as follows:

By Type

- Hydraulic

- Traction

- Machine Room-Less

- Pneumatic

- Others

By Application

- New Construction

- Retrofit

By End-User

- Single-Family Homes

- Multi-Family Homes

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Otis Elevator Company

- Schindler Group

- KONE Corporation

- Thyssenkrupp Elevator

- Mitsubishi Electric Corporation

- Fujitec Co., Ltd.

- Cibes Lift Group

- Kalea Lifts

- Nibav Lifts

- Waupaca Elevator Company

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors