![]()

Search Market Research Report

Closed System Transfer Device Market Size, Share Global Analysis Report, 2026-2034

Closed System Transfer Device Market Size, Share, Growth Analysis Report By Type (Membrane-to-Membrane Systems, Needleless Systems, and Others), By Component (Vial Access Devices, Syringe Safety Devices, Bag/Line Access Devices, and Others), By End-User (Hospitals, Oncology Centers & Clinics, Ambulatory Surgery Centers, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

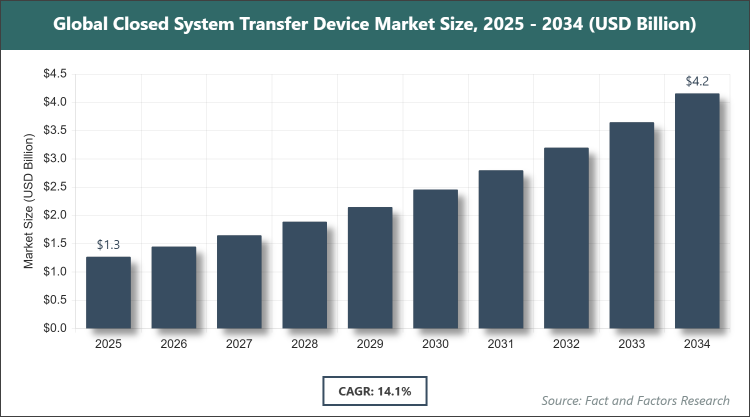

[230+ Pages Report] According to Facts & Factors, the global Closed System Transfer Device market size was estimated at USD 1.27 billion in 2025 and is expected to reach USD 4.75 billion by the end of 2034. The Closed System Transfer Device industry is anticipated to grow by a CAGR of 14.1% between 2026 and 2034. The Closed System Transfer Device Market is driven by increasing regulatory compliance for hazardous drug handling and rising cancer prevalence.

Market Overview

Market Overview

The closed system transfer device market involves the design, manufacturing, and distribution of specialized systems that ensure the safe handling and transfer of hazardous drugs, such as chemotherapy agents, by preventing environmental contamination and protecting healthcare workers from exposure. These devices create a sealed pathway during drug preparation, administration, and disposal, incorporating mechanisms like membranes or needleless connectors to maintain sterility and minimize aerosolization or spillage. The market serves primarily oncology and pharmacy settings, emphasizing compliance with safety standards while advancing through innovations in user-friendly designs and integration with existing workflows to enhance occupational safety and patient care.

Key Insights

- As per the analysis shared by our research analyst, the global Closed System Transfer Device market is estimated to grow annually at a CAGR of around 14.1% over the forecast period (2026-2034).

- In terms of revenue, the global Closed System Transfer Device market size was valued at around USD 1.27 billion in 2025 and is projected to reach USD 4.75 billion, by 2034.

- The Closed System Transfer Device market is projected to witness significant growth due to stringent regulations on hazardous drug handling and increasing oncology treatments.

- Based on the Type, the Membrane-to-Membrane Systems segment accounted for the largest market share of 55% due to its effective containment and ease of use in high-risk drug transfers.

- Based on the Component, the Vial Access Devices segment dominated the market with the highest share owing to its critical role in safe drug reconstitution and widespread adoption in pharmacies.

- Based on the End-User, the Hospitals segment held the leading position with a substantial share because of high patient volumes and regulatory mandates for worker safety.

- Based on the region, the North America region captured around 45% market share, driven by advanced healthcare infrastructure and strict USP <800> compliance requirements.

Growth Drivers

- Stringent Regulatory Compliance

Global regulations like USP <800> in the U.S. mandate the use of CSTDs for handling hazardous drugs, compelling healthcare facilities to adopt these devices to avoid penalties and ensure worker safety. This push is amplified by increasing awareness of occupational hazards from antineoplastic drugs, leading to widespread implementation in oncology centers. Innovations in device design, such as intuitive interfaces, further facilitate compliance without disrupting workflows.

Additionally, collaborations between regulators and manufacturers accelerate product approvals, expanding market access. This driver sustains growth by aligning with healthcare priorities, reducing exposure risks, and fostering trust in CSTD efficacy.

Restraints

- High Implementation Costs

The elevated costs of CSTDs, including device acquisition and training, deter adoption in resource-limited settings, particularly in developing regions with constrained healthcare budgets. Compatibility issues with existing equipment add to expenses, requiring system overhauls. Economic pressures post-pandemic exacerbate this, delaying upgrades.

Moreover, reimbursement limitations for these devices hinder financial viability for smaller facilities. These factors constrain market expansion, necessitating cost-reduction strategies and subsidies to broaden accessibility.

Opportunities

- Rising Cancer Prevalence

The global increase in cancer cases heightens demand for chemotherapy, necessitating CSTDs for safe drug administration and reducing exposure risks. Emerging markets with improving oncology infrastructure present untapped potential. Advancements in personalized medicine require precise handling, boosting CSTD integration.

Furthermore, partnerships with pharmaceutical firms for co-developed systems enhance compatibility. This opportunity drives innovation, positioning CSTDs as essential in expanding cancer care networks.

Challenges

- Technical Compatibility Issues

Variations in drug vial sizes and administration methods complicate CSTD integration, leading to inefficiencies and potential errors. Evolving drug formulations demand continuous device updates, straining R&D resources. User resistance due to learning curves adds operational challenges.

In addition, supply chain disruptions for specialized components affect availability. These issues require standardized protocols and adaptive designs to ensure seamless adoption.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.27 Billion |

Projected Market Size in 2034 |

USD 4.75 Billion |

CAGR Growth Rate |

14.1% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BD (Becton, Dickinson and Company), ICU Medical, Inc., B. Braun Melsungen AG, EQUASHIELD, Baxter International Inc., Teva Pharmaceutical Industries Ltd., Corvida Medical, JMS Co., Ltd., Yukon Medical, VICTUS, CODAN Medizinische Geräte GmbH & Co KG, Caragen Ltd., and Others. |

Key Segment |

By Type, By Component, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Closed System Transfer Device market is segmented by type, component, end-user, and region.

Based on Type Segment, the Closed System Transfer Device market is divided into Membrane-to-Membrane Systems, Needleless Systems, and others. The most dominant segment is Membrane-to-Membrane Systems, which holds the largest share due to its robust barrier protection against vapors and spills during drug transfer, driving the market by ensuring superior safety in high-volume oncology settings; the second most dominant is Needleless Systems, valued for reducing needlestick injuries and simplifying workflows, contributing to market growth through enhanced user safety and efficiency in hospitals.

Based on Component Segment, the Closed System Transfer Device market is divided into Vial Access Devices, Syringe Safety Devices, Bag/Line Access Devices, and others. The most dominant segment is Vial Access Devices, commanding the highest share because of their essential function in secure drug extraction from vials, which drives the market by preventing contamination in pharmacy compounding; the second most dominant is Syringe Safety Devices, critical for safe injection preparation, propelling market expansion via compliance with safety standards in clinical environments.

Based on End-User Segment, the Closed System Transfer Device market is divided into Hospitals, Oncology Centers & Clinics, Ambulatory Surgery Centers, and others. The most dominant segment is Hospitals, holding the biggest share due to their high patient throughput and regulatory requirements for hazardous drug handling, driving the market by integrating CSTDs into broad healthcare operations; the second most dominant is Oncology Centers & Clinics, focused on chemotherapy safety, contributing to market growth amid rising cancer treatments.

Recent Developments

- In September 2025, EQUASHIELD launched CellSHIELD, a new CSTD designed to enhance safety from hazardous drug exposure for healthcare workers and patients.

- In September 2025, Elcam Medical announced updates in its product line, focusing on improved compatibility for CSTDs in drug delivery.

- In October 2025, Takeda introduced HyHub and HyHub Duo devices, advancing safe handling in biologic drug administration.

- In February 2025, BD introduced the PhaSeal Optima Closed System Drug Transfer Device to improve safety in drug preparation and administration.

- In January 2025, BD showcased new delivery formats for biologics at Pharmapack 2025, emphasizing integration with CSTD technologies.

- In December 2024, NIOSH updated its List of Hazardous Drugs, expanding requirements for CSTD usage in healthcare facilities.

- In October 2024, BD and Ypsomed collaborated on self-injection systems compatible with CSTDs for high-viscosity biologics.

Regional Analysis

- North America to dominate the global market

North America emerges as the frontrunner in the closed system transfer device market, with the United States dominating through its rigorous regulatory framework like USP <800> that mandates CSTD use for hazardous drugs, coupled with advanced healthcare infrastructure supporting widespread adoption in hospitals and oncology centers. The region's emphasis on occupational safety drives innovation in user-friendly devices, while high cancer incidence fuels demand for secure chemotherapy handling. Investments in R&D by key players enhance product efficacy, ensuring compliance and efficiency. The U.S. benefits from robust reimbursement policies and a mature pharmaceutical sector, solidifying its lead.

Europe maintains a strong foothold with a focus on sustainable and compliant healthcare practices, led by Germany as the dominant country via its engineering prowess in medical devices and export-oriented economy. EU directives on worker protection accelerate CSTD integration in pharmacies, while collaborative research initiatives foster technological advancements. Germany's dominance stems from its pharmaceutical heritage and stringent safety standards, promoting eco-friendly designs amid green healthcare trends.

Asia Pacific shows rapid expansion driven by healthcare modernization and rising cancer rates, with China as the dominant country through massive investments in hospital infrastructure and domestic manufacturing of cost-effective CSTDs. Government policies enhancing drug safety protocols boost adoption, while increasing awareness of exposure risks supports market penetration. China's lead arises from its vast population and emerging oncology sector, enabling scalable production.

Latin America is progressing with improving healthcare access and regulatory alignments, led by Brazil as the dominant country via public health reforms and foreign investments in medical technology. Infrastructure developments in urban centers drive CSTD use in chemotherapy, offsetting economic challenges through partnerships. Brazil's position strengthens from its regional influence and growing pharmaceutical industry.

The Middle East & Africa region advances through oil-funded healthcare upgrades, with Saudi Arabia dominating via Vision 2030's emphasis on advanced medical facilities and safety protocols. Investments in oncology centers enhance CSTD demand, while international collaborations transfer technology. Saudi Arabia's lead comes from strategic diversification and policy-driven healthcare expansions.

Competitive Analysis

The global Closed System Transfer Device market is dominated by players:

- BD (Becton, Dickinson and Company)

- ICU Medical, Inc.

- B. Braun Melsungen AG

- EQUASHIELD

- Baxter International Inc.

- Teva Pharmaceutical Industries Ltd.

- Corvida Medical

- JMS Co., Ltd.

- Yukon Medical

- VICTUS

- CODAN Medizinische Geräte GmbH & Co KG

- Caragen Ltd.

The global Closed System Transfer Device market is segmented as follows:

By Type

- Membrane-to-Membrane Systems

- Needleless Systems

- Others

By Component

- Vial Access Devices

- Syringe Safety Devices

- Bag/Line Access Devices

- Others

By End-User

- Hospitals

- Oncology Centers & Clinics

- Ambulatory Surgery Centers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- BD (Becton, Dickinson and Company)

- ICU Medical, Inc.

- B. Braun Melsungen AG

- EQUASHIELD

- Baxter International Inc.

- Teva Pharmaceutical Industries Ltd.

- Corvida Medical

- JMS Co., Ltd.

- Yukon Medical

- VICTUS

- CODAN Medizinische Geräte GmbH & Co KG

- Caragen Ltd

Frequently Asked Questions

What are the various stages in the value chain of the global Closed System Transfer Device industry?

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors