![]()

Search Market Research Report

Petroleum Coke Market Size, Share Global Analysis Report, 2026-2034

Petroleum Coke Market Size, Share, Growth Analysis Report By Type (Fuel Grade Petroleum Coke and Calcined Petroleum Coke), By Application (Aluminum Industry, Cement Industry, Power Generation, Steel Industry, and Others), By End-User (Industrial), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

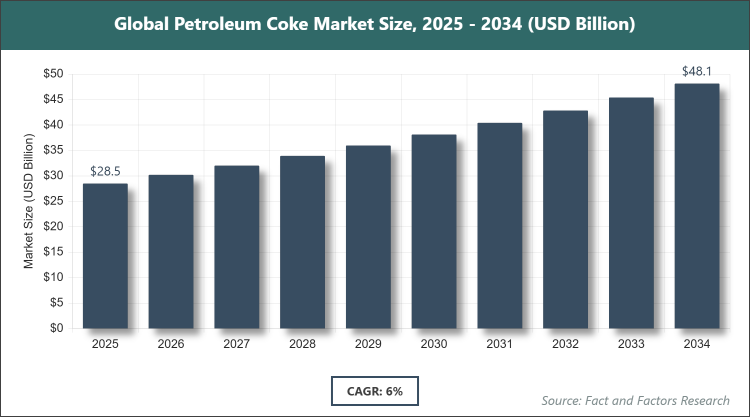

[244 Pages Report] According to Facts & Factors, the global Petroleum Coke market size was estimated at USD 28.5 billion in 2025 and is expected to reach USD 48.2 billion by the end of 2034. The Petroleum Coke industry is anticipated to grow by a CAGR of 6.0% between 2026 and 2034. The Petroleum Coke Market is driven by robust expansion in aluminum smelting, cement production, and power generation sectors across emerging economies.

Market Overview

Market Overview

The Petroleum Coke market involves the production, trading, and utilization of a solid carbon-rich byproduct generated during the thermal cracking of heavy crude oil residues in delayed coking units at oil refineries. Petroleum coke, commonly known as petcoke, is available in two primary forms: fuel-grade (high-sulfur, high-metal content used primarily as a low-cost fuel) and calcined-grade (low-sulfur, purified form used as a carbon source in anodes and electrodes). It serves as a high-calorific-value energy source and essential raw material in energy-intensive industries, offering economic advantages over coal or natural gas in specific applications while contributing to refinery profitability by converting low-value residues into marketable products.

Key Insights

- As per the analysis shared by our research analyst, the Petroleum Coke market is estimated to grow annually at a CAGR of around 6.0% over the forecast period (2026-2034).

- In terms of revenue, the Petroleum Coke market size was valued at around USD 28.5 billion in 2025 and is projected to reach USD 48.2 billion by 2034.

- The Petroleum Coke Market is driven by expanding aluminum and cement industries in emerging economies.

- Based on the Type, the Fuel Grade Petroleum Coke segment dominated the market in 2025 with a share of 72% due to its cost-effectiveness and widespread use as an alternative fuel in cement kilns and power plants.

- Based on the Application, the Cement Industry segment dominated the market in 2025 with a share of 41%, owing to high energy demand and petcoke’s superior calorific value that reduces overall fuel costs in clinker production.

- Based on the End-User, the Industrial segment dominated the market in 2025 with a share of 95% because petroleum coke is almost exclusively consumed by heavy industrial processes requiring high-temperature combustion or carbon feedstock.

- Asia Pacific dominated the global Petroleum Coke market in 2025 with a share of 51% attributed to massive refining capacity, rapid industrialization, and dominant aluminum and cement production in China and India.

Growth Drivers

- Industrial Expansion in Emerging Economies

Rapid growth in aluminum smelting capacity and cement production across Asia and the Middle East has significantly increased demand for both calcined coke in anodes and fuel-grade coke as a cost-effective energy source.

Rising global energy needs and the preference for high-calorific fuels in power generation have further supported petcoke consumption, particularly in regions with limited access to cheaper coal alternatives.

Restraints

- Environmental Regulations and Carbon Emissions

Strict emission norms and carbon pricing mechanisms in developed regions have restricted the use of high-sulfur fuel-grade petcoke, increasing compliance costs and limiting market growth in Europe and North America.

Public and regulatory pressure to reduce reliance on fossil-based fuels has prompted some industries to explore biomass or natural gas substitutes, slowing volume growth in certain applications.

Opportunities

- Rising Demand for Calcined Coke in New Applications

Growing lithium-ion battery and graphite electrode markets are creating new high-value outlets for high-purity calcined petroleum coke beyond traditional aluminum and steel sectors.

Technological advancements in desulfurization and gasification processes are enabling cleaner utilization of fuel-grade petcoke, opening opportunities in regions previously constrained by environmental regulations.

Challenges

- Price Volatility and Refinery Output Fluctuations

Dependence on crude oil refining patterns means petcoke supply is directly tied to refinery utilization rates and crude slate changes, leading to periodic shortages or oversupply that affect pricing stability.

Competition from lower-cost coal and natural gas in the power and cement sectors, combined with the shift toward renewable energy, poses long-term demand risks for fuel-grade petcoke.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 28.5 Billion |

Projected Market Size in 2034 |

USD 48.2 Billion |

CAGR Growth Rate |

6.0% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

ExxonMobil Corporation, Chevron Corporation, BP p.l.c., Reliance Industries Limited, Saudi Arabian Oil Company (Saudi Aramco), Valero Energy Corporation, Phillips 66, China National Petroleum Corporation (CNPC), Indian Oil Corporation Limited, Shell plc, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Petroleum Coke market is segmented by type, application, end-user, and region.

Based on Type Segment, the Petroleum Coke market is divided into fuel-grade petroleum coke and calcined petroleum coke. The most dominant segment is Fuel Grade Petroleum Coke, followed by Calcined Petroleum Coke. Fuel Grade Petroleum Coke dominates because of its significantly lower production cost and high calorific value, which makes it an economical fuel substitute for coal in cement kilns and power plants, thereby generating the largest consumption volumes and driving overall market growth through steady demand from energy-intensive industries in developing regions.

Based on Application Segment, the Petroleum Coke market is divided into the aluminum industry, cement industry, power generation, steel industry, and others. The most dominant segment is the Cement Industry, followed by the Aluminum Industry. Cement Industry leads the segment due to its massive global scale and the ability of fuel-grade petcoke to replace more expensive fuels while maintaining kiln performance, which creates a consistent high-volume offtake and stimulates refinery investments in coker units to maximize petcoke yield for this key end-use.

Based on the End-User Segment, the Petroleum Coke market is divided into industrial. The most dominant segment is Industrial. Industrial dominates because virtually all petroleum coke is consumed by heavy manufacturing and energy sectors that require either high-carbon anodes or low-cost combustible fuel, creating a highly concentrated demand base that supports large-scale production economics and continuous capacity additions across refining hubs worldwide.

Recent Developments

- In January 2025, ExxonMobil announced a 20% expansion of petroleum coke production capacity at its U.S. Gulf Coast refineries to meet rising demand from domestic cement and power sectors.

- In June 2025, Reliance Industries commissioned a new delayed coker unit at its Jamnagar refinery in India, increasing calcined-grade petcoke output for aluminum industry exports.

- In March 2025, Saudi Aramco signed long-term supply agreements with major Chinese aluminum smelters for low-sulfur calcined petroleum coke.

- In September 2025, Valero Energy launched a desulfurization technology pilot for fuel-grade petcoke to comply with tightening emission standards in European markets.

- In November 2025, China National Petroleum Corporation expanded its petcoke gasification project to supply cleaner syngas for industrial power generation.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the Petroleum Coke market through its massive refining throughput, dominant position in global aluminum and cement production, and rapid industrialization that sustains high demand for both fuel-grade and calcined grades. The region benefits from integrated refinery-petrochemical complexes that maximize petcoke yield and from government policies supporting heavy industries. Strong intra-regional trade and export capabilities to other developing markets further reinforce its leadership. China dominates within Asia Pacific with the world’s largest refining capacity, enormous cement and aluminum output, and strategic investments in steel and power infrastructure that consume vast quantities of petroleum coke while also serving as a major exporter of calcined products to global markets.

North America holds a notable share in the Petroleum Coke market, supported by advanced refining technology, significant domestic cement and power demand, and established export channels for fuel-grade material. The region leads in innovation for cleaner utilization technologies and benefits from integrated supply chains linked to major oil producers. The United States dominates within North America owing to its extensive Gulf Coast refining cluster, large industrial base, and position as a key supplier of high-quality petcoke to international aluminum and steel customers.

Europe maintains steady consumption in the Petroleum Coke market, driven by regulated industrial applications, focus on circular economy principles, and imports of low-sulfur calcined coke for specialized uses. Environmental compliance drives adoption of cleaner grades while limiting high-sulfur fuel-grade volumes. Germany dominates within Europe through its advanced chemical and steel industries, sophisticated import infrastructure, and leadership in developing low-emission petcoke utilization technologies for industrial processes.

Latin America is experiencing growing uptake in the Petroleum Coke market, fueled by expanding cement production, mining activities, and power generation needs amid economic recovery. Increasing refinery modernization projects are boosting local supply. Brazil dominates the region with its large cement and steel sectors, growing energy demand, and strategic refining investments that enhance domestic petcoke availability for industrial consumers.

The Middle East & Africa region shows strong potential in the Petroleum Coke market, supported by world-class refining complexes, abundant crude resources, and expanding downstream industries, including aluminum and cement. Strategic diversification initiatives are increasing local consumption. Saudi Arabia leads within the region through its massive refining capacity, Vision 2030 industrial projects, and role as a major global exporter of both fuel-grade and calcined petroleum coke to Asia and other markets.

Competitive Analysis

The global Petroleum Coke market is dominated by players:

- ExxonMobil Corporation

- Chevron Corporation

- BP p.l.c.

- Reliance Industries Limited

- Saudi Arabian Oil Company (Saudi Aramco)

- Valero Energy Corporation

- Phillips 66

- China National Petroleum Corporation (CNPC)

- Indian Oil Corporation Limited

- Shell plc

The global Petroleum Coke market is segmented as follows:

By Type

- Fuel Grade Petroleum Coke

- Calcined Petroleum Coke

By Application

- Aluminum Industry

- Cement Industry

- Power Generation

- Steel Industry

- Others

By End-User

- Industrial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- ExxonMobil Corporation

- Chevron Corporation

- BP p.l.c.

- Reliance Industries Limited

- Saudi Arabian Oil Company (Saudi Aramco)

- Valero Energy Corporation

- Phillips 66

- China National Petroleum Corporation (CNPC)

- Indian Oil Corporation Limited

- Shell plc

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors