![]()

Search Market Research Report

Optical Chain Stores Market Size, Share Global Analysis Report, 2026-2034

Optical Chain Stores Market Size, Share, Growth Analysis Report By Product (Eyeglasses, Sunglasses, Contact Lenses, and Others), By Customer Segment (Children, Adults, Seniors, and Others), By Distribution Channel (Offline and Online), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

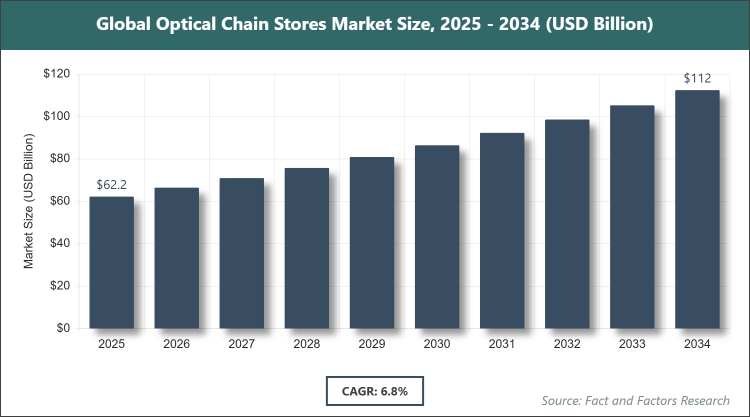

[237 + Pages Report] According to Facts & Factors, the global Optical Chain Stores market size was estimated at USD 62.2 billion in 2025 and is expected to reach USD 112.7 billion by the end of 2034. The Optical Chain Stores industry is anticipated to grow by a CAGR of 6.8% between 2026 and 2034. The Optical Chain Stores Market is driven by rising screen time, increasing prevalence of refractive errors, and growing consumer focus on eye health and fashionable eyewear.

Market Overview

Market Overview

The Optical Chain Stores market encompasses organized retail networks specializing in the sale of vision correction products and protective eyewear, along with comprehensive eye care services. These chains operate multiple branded outlets that offer eyeglasses, sunglasses, contact lenses, and related accessories while providing professional services such as eye examinations, prescription dispensing, frame customization, and after-sales support. Optical chain stores differentiate themselves through standardized store formats, trained optometrists on-site, wide product assortments from premium to value segments, and integrated omnichannel experiences that combine in-store fittings with online browsing capabilities. The market serves diverse consumer needs ranging from medical vision correction to lifestyle and fashion requirements, operating under a vertically integrated model that ensures quality control, brand consistency, and efficient supply of lenses and frames across global locations.

Key Insights

- As per the analysis shared by our research analyst, the Optical Chain Stores market is estimated to grow annually at a CAGR of around 6.8% over the forecast period (2026-2034).

- In terms of revenue, the Optical Chain Stores market size was valued at around USD 62.2 billion in 2025 and is projected to reach USD 112.7 billion by 2034.

- The Optical Chain Stores Market is driven by increasing digital device usage and an aging population worldwide.

- Based on the Product, the Eyeglasses segment dominated the market in 2025 with a share of 56% due to its essential role in daily vision correction and widespread prescription requirements across all age groups.

- Based on the Customer Segment, the Adults segment dominated the market in 2025 with a share of 48%, owing toa higher incidence of refractive errors among working professionals, combined with higher disposable income for premium frames and lenses.

- Based on the Distribution Channel, the Offline segment dominated the market in 2025 with a share of 72% because of the necessity for professional eye examinations, accurate fittings, and immediate product trials that build consumer trust.

- North America dominated the global Optical Chain Stores market in 2025 with a share of 35%, attributed to well-established retail chains, high consumer awareness of eye health, and strong reimbursement support for vision care services.

Growth Drivers

- Rising Prevalence of Vision Impairments

Prolonged exposure to digital screens has significantly increased cases of myopia, presbyopia, and digital eye strain, particularly among younger populations and office workers, creating sustained demand for corrective eyewear and specialized lenses. This trend is further amplified by growing health consciousness that encourages regular eye check-ups and early adoption of vision aids.

Technological advancements in lens materials, such as blue-light blocking coatings and photochromic options, enhance product appeal and encourage upgrades, boosting average transaction values within chain stores. Government initiatives promoting eye health awareness in schools and workplaces additionally support higher footfall and repeat visits to optical retail outlets.

Restraints

- Intense Competition from Online Retailers

Pure-play e-commerce platforms offering lower prices, virtual try-on tools, and home delivery challenge traditional chain stores by capturing price-sensitive customers and reducing in-store traffic. This shift pressures margins as physical locations incur higher operational costs related to rent, staffing, and inventory management.

Supply chain volatility for high-quality lenses and frames, coupled with raw material price fluctuations, further constrains profitability and limits the ability of chains to maintain competitive pricing against digital disruptors.

Opportunities

- Expansion in Emerging Markets

Rapid urbanization and rising middle-class incomes in the Asia-Pacific and Latin America present significant untapped potential for optical chain stores to establish a presence through franchising and strategic partnerships with local retailers.

Integration of telemedicine-enabled eye exams and AI-powered recommendation systems can lower entry barriers in underserved regions while improving customer engagement and personalization, driving long-term loyalty and market penetration.

Challenges

- Regulatory and Compliance Requirements

Strict regulations governing the sale of prescription eyewear, licensing of optometrists, and quality standards for medical devices create operational complexities and increase compliance costs for multi-country chain operations.

Shortage of qualified optometrists and opticians in certain regions hampers service quality and store expansion plans, while evolving data privacy laws related to customer vision records add layers of administrative burden for retail chains.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 62.2 Billion |

Projected Market Size in 2034 |

USD 112.7 Billion |

CAGR Growth Rate |

6.8% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

EssilorLuxottica, GrandVision, Specsavers, Fielmann AG, National Vision Holdings Inc., Visionworks, MyEyeDr., Warby Parker, Costco Optical, Alcon Vision Care, and Others. |

Key Segment |

By Product, By Customer Segment, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Optical Chain Stores market is segmented by product, customer segment, distribution channel, and region.

Based on Product Segment, the Optical Chain Stores market is divided into eyeglasses, sunglasses, contact lenses, and others. The most dominant segment is Eyeglasses, driven by the universal need for vision correction and frequent replacement cycles due to fashion and prescription changes. The second most dominant is Contact Lenses, propelled by convenience for active lifestyles and advancements in daily disposables. Eyeglasses dominate because they serve as both functional and style statements, enabling chains to offer bundled services like eye exams and custom fittings that increase customer dwell time and cross-selling opportunities, thereby driving overall market revenue growth through higher basket sizes and repeat purchases.

Based on Customer Segment, the Optical Chain Stores market is divided into children, adults, seniors, and others. The most dominant segment is Adults, owing to occupational screen exposure and higher purchasing power for premium products. The second most dominant is Seniors, supported by age-related vision decline and increased healthcare focus. Adults lead the segment as they represent the largest working population requiring progressive lenses and blue-light protection, allowing chains to leverage targeted marketing campaigns and loyalty programs that enhance lifetime value and stimulate consistent demand for upgrades.

Based on the Distribution Channel Segment, the Optical Chain Stores market is divided into offline and online. The most dominant segment is Offline, due to the critical requirement for in-person eye examinations and precise frame adjustments. The second most dominant is Online, growing rapidly with virtual try-on technologies. Offline dominates because it combines professional consultation with immediate product availability and after-sales services, fostering trust and enabling chains to differentiate through experiential retail that drives higher conversion rates and premium product sales.

Recent Developments

- In May 2025, Walmart expanded its optical offerings by introducing Nuance Audio Glasses and eureka Daily contact lenses across its stores while enhancing AR try-on technology to cover over 1,700 frames.

- In February 2025, Kering Eyewear acquired Visard and took a minority stake in Mistral to strengthen its luxury eyewear distribution network across Europe.

- In July 2025, Fielmann Group completed the acquisition of Shopko Optical assets, significantly expanding its footprint in the U.S. market and raising its full-year revenue guidance.

- In November 2025, Specsavers launched a new chain of premium stores in Southeast Asia featuring AI-assisted eye testing kiosks to accelerate regional expansion.

- In January 2026, EssilorLuxottica partnered with a leading tele-optometry platform to integrate remote prescription renewal services across its LensCrafters and Pearle Vision locations.

Regional Analysis

- North America to dominate the global market

North America leads the Optical Chain Stores market through its mature retail infrastructure, high consumer awareness regarding preventive eye care, and widespread presence of established branded chains offering integrated vision services. The region benefits from favorable insurance coverage for eye exams and a culture that values both functional and fashionable eyewear. The United States dominates within North America, supported by dense networks of optical outlets in malls and standalone locations, advanced lens technology adoption, and strong marketing collaborations with fashion brands that drive premium sales while maintaining accessibility for mass-market consumers.

Europe holds a substantial share in the Optical Chain Stores market, characterized by stringent quality regulations, aging demographics, and emphasis on sustainable eyewear materials. Consumers prioritize professional service and long-lasting products. Germany dominates the region with its engineering precision in lens manufacturing and widespread acceptance of value-oriented optical chains that combine affordability with high-quality fittings, enabling efficient scaling of store formats across urban and rural areas.

Asia-Pacific exhibits the fastest growth in the Optical Chain Stores market, fueled by massive populations, rising myopia rates among youth, and increasing disposable incomes that support premium eyewear purchases. Government initiatives for school eye health programs further boost early adoption. China dominates this region through rapid urbanization, expansion of domestic and international chains, and integration of e-commerce with physical stores that cater to both urban millennials and rural consumers seeking accessible vision care.

Latin America is gaining momentum in the Optical Chain Stores market as healthcare awareness improves and middle-class expansion drives demand for branded eyewear. Retail modernization and franchising models accelerate penetration. Brazil leads the region with its large consumer base, vibrant fashion culture influencing sunglass sales, and a growing number of specialized optical outlets that combine eye care with lifestyle retail experiences.

The Middle East & Africa region shows emerging opportunities in the Optical Chain Stores market, supported by urban development, expatriate populations, and investments in modern healthcare retail. Rising tourism and retail mall culture aid visibility. South Africa dominates through its developed commercial infrastructure and established optical chains that serve diverse socioeconomic groups while introducing advanced lens technologies suited to local climate and lifestyle needs.

Competitive Analysis

The global Optical Chain Stores market is dominated by players:

- EssilorLuxottica

- GrandVision

- Specsavers

- Fielmann AG

- National Vision Holdings Inc.

- Visionworks

- MyEyeDr.

- Warby Parker

- Costco Optical

- Alcon Vision Care

The global Optical Chain Stores market is segmented as follows:

By Product

- Eyeglasses

- Sunglasses

- Contact Lenses

By Customer Segment

- Children

- Adults

- Seniors

By Distribution Channel

- Offline

- Online

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- EssilorLuxottica

- GrandVision

- Specsavers

- Fielmann AG

- National Vision Holdings Inc.

- Visionworks

- MyEyeDr.

- Warby Parker

- Costco Optical

- Alcon Vision Care

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors