![]()

Search Market Research Report

Metal Powder Market Size, Share Global Analysis Report, 2026-2034

Metal Powder Market Size, Share, Growth Analysis Report By Type (Ferrous, Non-Ferrous, and Others), By Production Method (Atomization, Reduction, Electrolysis, and Others), By Application (Automotive, Aerospace, Electronics, Medical, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

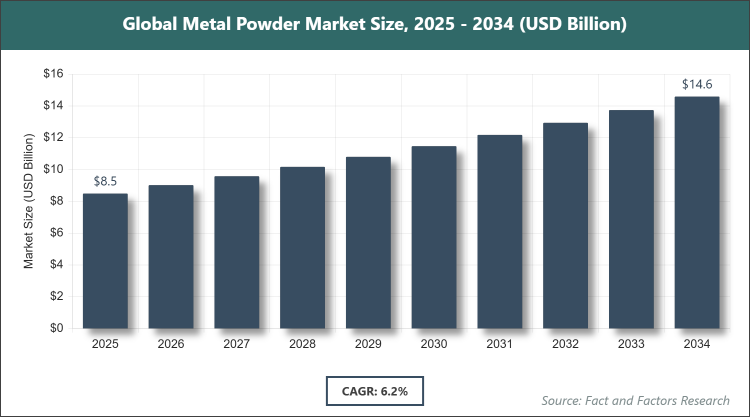

[242 Pages Report] According to Facts & Factors, the global Metal Powder market size was estimated at USD 8.49 billion in 2025 and is expected to reach USD 14.58 billion by the end of 2034. The Metal Powder industry is anticipated to grow by a CAGR of 6.2% between 2026 and 2034. The Metal Powder Market is driven by increasing demand in additive manufacturing and automotive lightweighting.

Market Overview

Market Overview

The metal powder market encompasses the production, distribution, and application of finely ground metallic particles derived from various metals such as iron, aluminum, copper, and nickel, which are utilized primarily in powder metallurgy processes including additive manufacturing, metal injection molding, and sintering to create complex components with enhanced mechanical properties for industries like automotive, aerospace, and electronics, focusing on achieving high precision, reduced waste, and improved material efficiency in manufacturing operations. This market involves a range of stakeholders from raw material suppliers to end-users, emphasizing innovation in particle size control and alloy compositions to meet evolving demands for lightweight and durable products across global supply chains.

Key Insights

- As per the analysis shared by our research analyst, the Metal Powder market is expected to grow at a CAGR of 6.2% during the forecast period of 2026-2034.

- In terms of revenue, the Metal Powder market size was valued at about USD 8.49 billion in 2025 and is expected to reach USD 14.58 billion by 2034.

- The Metal Powder market is driven by increasing demand in additive manufacturing and automotive lightweighting.

- Based on the type, the ferrous segment dominated the market with a share of 69% in 2025 due to its extensive use in automotive and industrial applications for high-strength components.

- Based on the production method, the atomization segment dominated the market with a share of 56% in 2025 owing to its ability to produce high-purity spherical powders ideal for 3D printing.

- Based on the application, the automotive segment dominated the market with a share of 64% in 2025 as it benefits from lightweight and durable parts production.

- Asia Pacific dominated the market with a share of 37% in 2025 due to rapid industrialization and high manufacturing output in countries like China.

Growth Drivers

- Rising Demand in Additive Manufacturing

The surge in adoption of 3D printing technologies across aerospace and medical sectors is propelling the market, as metal powders enable the creation of complex geometries with minimal waste, enhancing design flexibility and reducing production times. This driver is supported by ongoing advancements in printer capabilities that demand high-quality powders for precision applications.

Furthermore, investments in R&D by key players are leading to improved powder formulations, fostering innovation and expanding the scope of additive manufacturing into new industries, thereby sustaining long-term growth through enhanced performance and cost efficiencies.

- Automotive Lightweighting Trends

Increasing focus on fuel efficiency and emission reductions is driving the use of metal powders in producing lightweight components like gears and engine parts, as automakers shift towards electric vehicles requiring advanced materials. This is amplified by regulatory pressures globally pushing for sustainable manufacturing practices.

Additionally, collaborations between automotive OEMs and powder suppliers are accelerating the development of tailored alloys, supporting market expansion by addressing specific performance needs and integrating powder metallurgy into mainstream production lines.

- Expansion in Aerospace Sector

Growing aircraft production and demand for high-performance materials are boosting metal powder usage in turbine components and structural parts, where superior strength-to-weight ratios are critical. This driver benefits from increasing air travel and defense spending worldwide.

Moreover, technological integrations such as topology optimization are enhancing component durability, driving market growth through specialized applications that leverage metal powders' unique properties in harsh environments.

Restraints

- High Production Costs

Elevated expenses associated with advanced atomization and purification processes limit accessibility for smaller manufacturers, constraining market penetration in cost-sensitive regions. This restraint is compounded by fluctuating raw material prices impacting profitability.

Efforts to optimize production techniques and scale operations are essential to mitigate these costs, though they require significant upfront investments, potentially slowing adoption rates in emerging markets.

- Environmental Regulations

Stringent emission controls and waste management requirements increase operational complexities for powder producers, raising compliance costs and hindering expansion. This issue is particularly acute in regions with rigorous environmental standards.

Adapting to sustainable practices through recycling initiatives is crucial, yet transitioning demands technological upgrades, affecting short-term market dynamics.

Opportunities

- Emerging Markets Growth

Rapid industrialization in Asia and Latin America presents avenues for metal powder adoption in infrastructure and consumer goods, supported by favorable government policies. This opportunity allows for market diversification beyond traditional sectors.

Strategic partnerships and local manufacturing setups can capitalize on this trend, enhancing supply chain resilience and tapping into growing demand for advanced materials.

- Technological Innovations

Advancements in nanostructured powders offer enhanced properties for electronics and biomedical applications, opening new revenue streams. This fosters differentiation in competitive landscapes.

Investments in R&D can lead to breakthrough formulations, driving adoption in high-value niches and supporting overall market evolution.

Challenges

- Supply Chain Volatility

Dependence on raw metal supplies exposes the market to geopolitical disruptions and price fluctuations, affecting production stability. Diversified sourcing is needed to address this.

Building resilient networks through alternative suppliers and stockpiling strategies is vital, though it adds to operational complexities.

- Competition from Alternatives

Development of composite materials and traditional casting methods poses threats to metal powder applications, requiring continuous innovation to maintain relevance. This challenge demands focused R&D efforts.

Emphasizing unique benefits like waste reduction and precision can help counter alternatives, sustaining market position.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 8.49 Billion |

Projected Market Size in 2034 |

USD 14.58 Billion |

CAGR Growth Rate |

6.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Sandvik AB, Carpenter Technology Corporation, Rio Tinto Ltd, Allegheny Technologies Incorporated, Alcoa Inc., Hoganas AB, GKN PLC, BASF SE, Kymera International, MolyWorks Materials Corporation, and Others. |

Key Segment |

By Type, By Production Method, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Metal Powder market is segmented by type, production method, application, and region.

Based on Type Segment, the metal powder market is divided into ferrous, non-ferrous, and others. The most dominant segment is ferrous, holding the largest share due to its widespread application in automotive and industrial sectors for producing high-strength, cost-effective components that enhance durability and performance, driving the market by supporting mass production in lightweight vehicles and machinery; the second most dominant is non-ferrous, which excels in aerospace and electronics for its corrosion resistance and conductivity, contributing to market growth through specialized uses in high-tech industries requiring precision and reliability.

Based on Production Method Segment, themetal powder market is divided into atomization, reduction, electrolysis, and others. The most dominant segment is atomization, leading the market because it produces uniform, spherical particles ideal for additive manufacturing and powder metallurgy, propelling growth by enabling high-quality outputs in demanding applications like 3D printing; the second most dominant is reduction, valued for its efficiency in producing iron and copper powders, aiding market expansion through cost-effective solutions for large-scale industrial needs.

Based on Application Segment, the metal powder market is divided into automotive, aerospace, electronics, medical, and others. The most dominant segment is automotive, commanding the top position owing to the need for lightweight and durable parts in vehicle manufacturing, boosting market growth via integration in electric and hybrid models; the second most dominant is aerospace, which drives demand through its use in high-performance components, contributing to expansion by addressing stringent requirements for strength and weight reduction.

Recent Developments

- In December 2023, Kymera International acquired Metallisation Limited to strengthen its position in thermal spray applications and expand its specialty materials portfolio.

- In November 2023, Kymera International acquired KDF Fluid Treatment Inc. to enhance its product offerings and market presence in fluid treatment solutions.

- In October 2023, Sandvik AB acquired Buffalo Tungsten, Inc. to bolster its tungsten powder capabilities and increase its market footprint in the U.S.

- In April 2022, Kymera International acquired AmeriTi Manufacturing Company to expand its reach in aerospace, medical, and defense markets.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the metal powder market with China as the dominating country, where extensive manufacturing hubs and rapid automotive production fuel demand for ferrous and non-ferrous powders in components like gears and engine parts, supported by government initiatives promoting industrial growth and technological advancements that enhance production efficiency, while the region's expanding electronics sector further drives usage in precision applications, creating a robust ecosystem for suppliers and end-users alike.

North America maintains a strong position led by the United States, which dominates through its advanced aerospace and additive manufacturing industries utilizing high-performance powders for aircraft components and prototypes, bolstered by significant R&D investments and collaborations between tech firms and universities that foster innovation, alongside a focus on sustainable practices that integrate recycled materials into production chains for environmental compliance.

Europe exhibits steady growth with Germany as the key country, emphasizing automotive and engineering applications where metal powders are essential for lightweight vehicle designs and machinery, integrated with strict regulatory frameworks promoting green manufacturing and circular economy principles, enabling high-quality exports and partnerships in advanced materials development across the continent.

Latin America is progressing, dominated by Brazil, where growing infrastructure projects and automotive sectors require metal powders for construction and vehicle parts, aided by natural resource availability and increasing foreign investments that improve local production capabilities, supporting economic diversification and regional trade in industrial goods.

The Middle East & Africa region is emerging, with South Africa leading due to its mining heritage providing raw materials for powder production used in industrial and defense applications, complemented by infrastructure developments and international collaborations that enhance technological adoption and market integration in global supply networks.

Competitive Analysis

The global Metal Powder market is dominated by players:

- Sandvik AB

- Carpenter Technology Corporation

- Rio Tinto Ltd

- Allegheny Technologies Incorporated

- Alcoa Inc.

- Hoganas AB

- GKN PLC

- BASF SE

- Kymera International

- MolyWorks Materials Corporation

The global Metal Powder market is segmented as follows:

By Type

- Ferrous

- Non-Ferrous

- Others

By Production Method

- Atomization

- Reduction

- Electrolysis

- Others

By Application

- Automotive

- Aerospace

- Electronics

- Medical

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors