![]()

Search Market Research Report

Industrial Connectors Market Size, Share Global Analysis Report, 2026-2034

Industrial Connectors Market Size, Share, Growth Analysis Report By Type (PCB Connectors, I/O Connectors, Circular Connectors, Fiber Optic Connectors, RF Coaxial Connectors, and Others), By Application (Automation Systems, Power Transmission, Data Communication, and Others), By End-Use Industry (Manufacturing, Automotive, Aerospace and Defense, Renewable Energy, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

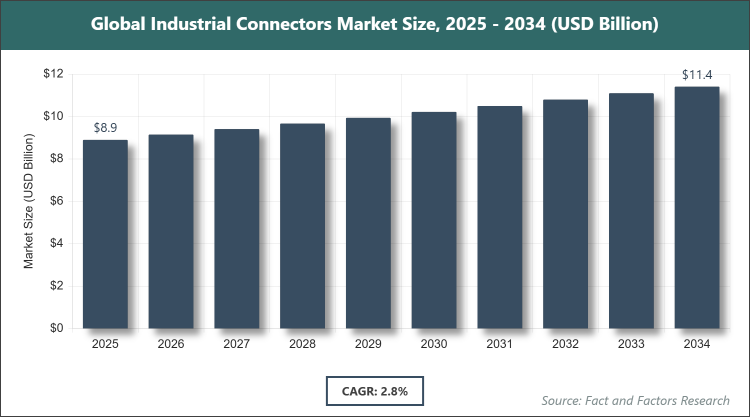

According to Facts & Factors, the global Industrial Connectors market size was estimated at USD 8.9 billion in 2025 and is expected to reach USD 11.6 billion by the end of 2034. The Industrial Connectors industry is anticipated to grow by a CAGR of 2.8% between 2026 and 2034. The Industrial Connectors Market is driven by increasing industrial automation and adoption of Industry 4.0.

Market Overview

Market Overview

Industrial connectors are specialized electrical and electronic components designed to establish secure and reliable connections between various devices, systems, and equipment in harsh industrial environments. These connectors facilitate the transmission of power, data, and signals while withstanding extreme conditions such as vibrations, moisture, dust, temperature fluctuations, and mechanical stress. They play a crucial role in enabling seamless integration and operation of machinery, automation systems, sensors, actuators, and control units across diverse sectors like manufacturing, energy, transportation, and aerospace. Unlike standard connectors used in consumer electronics, industrial variants prioritize durability, ingress protection, and compliance with stringent safety standards to ensure uninterrupted performance in demanding applications.

Key Insights

- As per the analysis shared by our research analyst, the global Industrial Connectors market is estimated to grow annually at a CAGR of around 2.8% over the forecast period (2026-2034).

- In terms of revenue, the global Industrial Connectors market size was valued at around USD 8.9 billion in 2025 and is projected to reach USD 11.6 billion, by 2034.

- The market is driven by increasing industrial automation, adoption of Industry 4.0 technologies, and growing demand for reliable connectivity in harsh environments.

- Based on the Type, Circular Connectors segment dominated the market in 2025 with a share of 35%, owing to their robust design, reliability in transmitting power and signals under extreme conditions like vibration and moisture, making them ideal for heavy machinery, defense, and automation applications.

- Based on the Application, Automation Systems segment dominated the market in 2025 with a share of 40%, due to the rising integration of sensors, actuators, and control units in smart factories, which requires high-performance connectors for real-time data exchange and operational efficiency.

- Based on the End-Use Industry, Manufacturing segment dominated the market in 2025 with a share of 45%, driven by the shift towards smart manufacturing, where connectors enable seamless connectivity in robotics, assembly lines, and IIoT systems to enhance productivity and reduce downtime.

- Based on region, Asia Pacific dominated the market in 2025 with a share of 45%, attributed to rapid industrialization, infrastructure expansion, and heavy investments in automation and renewable energy in countries like China and India.

Market Dynamics

Growth Drivers

- Rising Industrial Automation and Industry 4.0 Adoption

Industrial automation is transforming manufacturing and production processes by integrating advanced technologies such as robotics, sensors, and IoT devices, which rely heavily on reliable connectors for seamless data and power transmission. This trend is accelerating the demand for industrial connectors that can handle high-speed communication and withstand harsh operational environments, thereby boosting overall market growth.

The adoption of Industry 4.0 principles, including smart factories and digital twins, further amplifies the need for sophisticated connectivity solutions. As industries aim to improve efficiency, reduce downtime, and enable predictive maintenance, connectors with embedded intelligence and high durability become essential, driving innovation and expansion in the market.

Restraints

- Supply Chain Disruptions and Trade Tariffs

Global supply chain disruptions, often caused by geopolitical tensions, natural disasters, or pandemics, can lead to shortages of raw materials and components, increasing production costs and delaying deliveries for industrial connectors. This instability affects manufacturers' ability to meet demand, potentially slowing market growth.

Trade tariffs, such as those imposed on imports from key producing regions, escalate costs for end-users and encourage shifts to alternative sourcing, which may not always match quality standards. These economic barriers create uncertainty, restraining investment in new projects and limiting the market's expansion potential in price-sensitive sectors.

Opportunities

- Advancements in Connector Technology and Clean Energy Integration

Technological advancements, including the development of miniature, high-speed, and sensor-embedded connectors, open new avenues for applications in emerging fields like renewable energy and smart grids. These innovations allow for more efficient, compact designs that support the growing need for sustainable and intelligent industrial systems.

The integration of clean energy sources, such as wind and solar, requires robust connectors for power transmission to grids, presenting significant opportunities in infrastructure development. As governments and industries prioritize energy efficiency and environmental compliance, the demand for eco-friendly, high-performance connectors is expected to surge, fostering market growth.

Challenges

- High Costs and Technological Complexity

The high initial costs associated with advanced industrial connectors, including those with specialized features like IP67 protection or high-data-rate capabilities, can deter adoption in cost-constrained industries or regions. This financial barrier challenges widespread implementation, particularly for small and medium enterprises.

Technological complexity in designing and integrating connectors for diverse applications requires skilled expertise and rigorous testing, which can extend development timelines and increase expenses. As industries evolve rapidly, keeping pace with compatibility and standardization issues poses ongoing challenges, potentially hindering market penetration.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 8.9 Billion |

Projected Market Size in 2034 |

USD 11.6 Billion |

CAGR Growth Rate |

2.8% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

TE Connectivity, Lapp Group, 3M, AMETEK Inc., Amphenol Corporation, Aptiv PLC, AVX Corporation, Fischer Connectors, Foxconn Technology Group, GTK UK Ltd., Hirose Electric Co., Ltd., Japan Aviation Electronics Industry, Ltd., Luxshare Precision Industry Co., Ltd., Mencom Corporation, Molex, Inc., Phoenix Contact, Rosenberger Group, YAZAKI Corporation, and Others. |

Key Segment |

By Type, By Application, By End-Use Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Industrial Connectors market is segmented by type, application, end-user, and region.

Based on Type Segment, the Industrial Connectors market is divided into PCB Connectors, I/O Connectors, Circular Connectors, Fiber Optic Connectors, RF Coaxial Connectors, and Others. The most dominant segment is Circular Connectors, which excels in providing secure, weatherproof connections for power and signal transmission in demanding environments, driving the market through enhanced reliability in automation and heavy machinery. The second most dominant is PCB Connectors, which supports compact electronic assemblies in control systems and devices, contributing to market growth by enabling miniaturization and high-density interconnections in industrial electronics.

Based on Application Segment, the Industrial Connectors market is divided into Automation Systems, Power Transmission, Data Communication, and Others. The most dominant segment is Automation Systems, where connectors ensure seamless integration of sensors and actuators, propelling market expansion by facilitating real-time control and efficiency in smart factories. The second most dominant is Power Transmission, which relies on durable connectors for reliable energy distribution in renewable setups, aiding market growth through support for sustainable infrastructure and reduced energy losses.

Based on End-Use Industry Segment, the Industrial Connectors market is divided into Manufacturing, Automotive, Aerospace and Defense, Renewable Energy, and Others. The most dominant segment is Manufacturing, driven by the need for robust connectivity in robotics and assembly lines, boosting the market via improved productivity and IIoT adoption. The second most dominant is Automotive, where connectors enable electrification and advanced safety systems, contributing to growth by meeting demands for vehicle automation and efficiency.

Recent Developments

- In April 2025, Hirose extended its LF Series high-speed Ethernet connectors to a Cat.6a variant, supporting 10Gbps with a compact design and bayonet lock for vibration resistance, enhancing connectivity in industrial automation applications.

- In January 2025, Amphenol Communications Solutions launched Type 6 Charging Gun solutions and DuraSwap Concentric Connectors at the Bharat Mobility Global Expo in New Delhi, focusing on electric vehicle infrastructure and rugged industrial use.

- In January 2025, TE Connectivity released the Miniaturized Circular Industrial Connectors (MCIC) series, designed for space-saving automation with 10 Gbps data transfer, IP67 sealing, and embedded sensing for harsh outdoor environments.

- In April 2025, binder introduced new 823 (L-coded) and 813 (T-coded) M12 connectors with IP67 protection, stainless-steel locking, and over 100 mating cycles, targeting power and signal transmission in industrial settings.

- In December 2024, One Equity Partners invested in Comau, an Italian firm specializing in industrial automation and robotics, to expand capabilities in advanced connectivity solutions for manufacturing.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the global industrial connectors landscape, fueled by accelerated industrialization and a strong emphasis on technological advancements. The region's vast manufacturing hubs integrate cutting-edge automation and digital systems, creating a high demand for durable connectivity solutions. With robust supply chains and innovation-driven policies, Asia Pacific continues to attract investments, solidifying its position through efficient production and export capabilities. China emerges as the dominating country, leveraging its massive industrial base and initiatives like Made in China 2025 to modernize manufacturing, which amplifies the adoption of advanced connectors in sectors ranging from electronics to renewable energy.

North America maintains a prominent role, characterized by its leadership in technological innovation and adoption of smart manufacturing practices. The region benefits from a mature industrial ecosystem that prioritizes efficiency and reliability in connectivity. Investments in research and development, coupled with a focus on sustainable practices, enhance the integration of advanced connectors across various industries. The United States is the dominating country, with its advanced automation infrastructure and strong presence in aerospace and defense, driving the need for high-performance connectors that support complex systems and ensure operational resilience.

Europe exhibits rapid growth, supported by strategic partnerships and a commitment to industrial expansion. The region's emphasis on adopting new technologies and fostering innovation creates a fertile ground for connector advancements. Collaborative efforts between governments and industries promote the development of eco-friendly and efficient solutions, aligning with broader sustainability goals. Germany dominates as the key country, renowned for its engineering prowess and focus on Industry 4.0, where precision manufacturing and automotive sectors heavily rely on sophisticated connectors for seamless integration and enhanced productivity.

The Middle East & Africa region is gaining traction through diversification efforts away from traditional resources, with investments in smart grids and renewable energy infrastructure. This shift fosters the adoption of modern connectivity solutions to support emerging industrial applications. Collaborative international projects and policy reforms further accelerate growth in this area. Saudi Arabia leads as the dominating country, propelled by Vision 2030 initiatives that emphasize smart manufacturing and digital transformation, increasing the deployment of industrial connectors in energy and construction sectors.

Latin America is emerging as a significant player, driven by initiatives to enhance digital infrastructure and industrial automation. The region's focus on clean energy integration and economic diversification creates opportunities for connector technologies. Supportive government policies and international collaborations aid in building resilient industrial networks. Brazil is the dominating country, with its Plano Nacional de Internet das Coisas promoting IoT adoption, which boosts the use of connectors in manufacturing and energy sectors for improved connectivity and efficiency.

Competitive Analysis

The global Industrial Connectors market is dominated by players:

- TE Connectivity

- Lapp Group

- 3M

- AMETEK Inc.

- Amphenol Corporation

- Aptiv PLC

- AVX Corporation

- Fischer Connectors

- Foxconn Technology Group

- GTK UK Ltd.

- Hirose Electric Co., Ltd.

- Japan Aviation Electronics Industry, Ltd.

- Luxshare Precision Industry Co., Ltd.

- Mencom Corporation

- Molex, Inc.

- Phoenix Contact

- Rosenberger Group

- YAZAKI Corporation

The global Industrial Connectors market is segmented as follows:

By Type

- PCB Connectors

- I/O Connectors

- Circular Connectors

- Fiber Optic Connectors

- RF Coaxial Connectors

- Others

By Application

- Automation Systems

- Power Transmission

- Data Communication

- Others

By End-Use Industry

- Manufacturing

- Automotive

- Aerospace and Defense

- Renewable Energy

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global Industrial Connectors market is dominated by players:

- TE Connectivity

- Lapp Group

- 3M

- AMETEK Inc.

- Amphenol Corporation

- Aptiv PLC

- AVX Corporation

- Fischer Connectors

- Foxconn Technology Group

- GTK UK Ltd.

- Hirose Electric Co., Ltd.

- Japan Aviation Electronics Industry, Ltd.

- Luxshare Precision Industry Co., Ltd.

- Mencom Corporation

- Molex, Inc.

- Phoenix Contact

- Rosenberger Group

- YAZAKI Corporation

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors