![]()

Search Market Research Report

Human Insulin Market Size, Share Global Analysis Report, 2026-2034

Human Insulin Market Size, Share, Growth Analysis Report By Type (Regular Human Insulin, NPH (Intermediate Acting) Insulin, Premixed Human Insulin, and Others), By Application (Type 1 Diabetes and Type 2 Diabetes), By End-User (Hospitals, Retail Pharmacies, Homecare Settings, Clinics, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

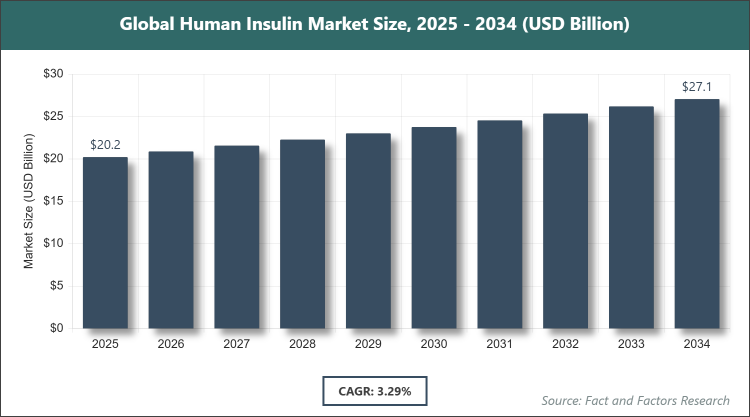

[224 Pages Report] According to Facts & Factors, the global Human Insulin market size was estimated at USD 20.22 billion in 2025 and is expected to reach USD 26.93 billion by the end of 2034. The Human Insulin industry is anticipated to grow by a CAGR of 3.29% between 2026 and 2034. The Human Insulin Market is driven by the rising global prevalence of diabetes and increasing demand for affordable, biosimilar human insulin formulations.

Market Overview

Market Overview

The Human Insulin market encompasses recombinant human insulin products that replicate the naturally occurring hormone produced by the human pancreas to regulate blood glucose levels. These products include regular short-acting insulin, intermediate-acting NPH insulin, and premixed formulations designed to provide flexible dosing options for patients with diabetes. Manufactured through advanced biotechnology processes using genetically engineered bacteria or yeast, human insulin offers a safer and more predictable alternative to animal-derived insulin with reduced risk of allergic reactions. Widely prescribed for both Type 1 and Type 2 diabetes management, these products are delivered via vials, pens, or pumps and play a foundational role in glycemic control, helping millions of patients achieve better long-term health outcomes while supporting the global shift toward cost-effective biosimilar options in both developed and emerging healthcare systems.

Key Insights

- As per the analysis shared by our research analyst, the Human Insulin market is estimated to grow annually at a CAGR of around 3.29% over the forecast period (2026-2034).

- In terms of revenue, the Human Insulin market size was valued at around USD 20.22 billion in 2025 and is projected to reach USD 26.93 billion by 2034.

- The Human Insulin Market is driven by increasing diabetes prevalence and demand for cost-effective biosimilars.

- Based on the Type, the Premixed Human Insulin segment dominated the market in 2025 with a share of 42% due to the convenience of fixed-ratio dosing for Type 2 diabetes patients requiring both basal and prandial coverage.

- Based on the Application, the Type 2 Diabetes segment dominated the market in 2025 with a share of 68% owing to the much larger patient population and growing adoption of insulin therapy in later-stage disease management.

- Based on the End-User, the Retail Pharmacies segment dominated the market in 2025 with a share of 55% because of widespread accessibility, patient preference for self-administration, and strong distribution networks for chronic therapies.

- North America dominated the global Human Insulin market in 2025 with a share of 45%, attributed to high diabetes awareness, advanced healthcare infrastructure, and the strong presence of leading manufacturers.

Growth Drivers

- Rising Global Diabetes Burden

The continuous increase in diabetes cases, particularly Type 2, driven by obesity, sedentary lifestyles, and aging populations, has created sustained demand for reliable and affordable insulin therapies worldwide.

Biosimilar approvals and government initiatives to improve insulin access in low- and middle-income countries have further expanded patient reach and boosted overall market volume.

Restraints

- Pricing Pressure and Reimbursement Challenges

Intense competition from biosimilars and insulin analogs has led to significant price erosion, squeezing margins for traditional human insulin manufacturers.

Inconsistent reimbursement policies across regions and out-of-pocket costs in developing markets limit patient adherence and restrict broader adoption.

Opportunities

- Expansion of Biosimilar Human Insulin in Emerging Markets

Growing healthcare infrastructure and supportive regulatory pathways for biosimilars in the Asia Pacific, Latin America, and Africa present substantial opportunities for cost-effective human insulin penetration.

Partnerships between global players and local manufacturers enable localized production, reducing costs and improving supply chain reliability in high-burden regions.

Challenges

- Competition from Insulin Analogs and Advanced Delivery Systems

Newer insulin analogs offering better glycemic control and reduced hypoglycemia risk continue to capture market share from traditional human insulin formulations.

Patient preference for convenient pens, pumps, and smart delivery devices adds pressure on vial-based human insulin products in developed markets.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 20.22 Billion |

Projected Market Size in 2034 |

USD 26.93 Billion |

CAGR Growth Rate |

3.29% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Novo Nordisk A/S, Eli Lilly and Company, Sanofi S.A., Biocon Limited, Wockhardt Ltd., Julphar, Tonghua Dongbao Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, ADOCIA, Boehringer Ingelheim, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Human Insulin market is segmented by type, application, end-user, and region.

Based on Type Segment, the Human Insulin market is divided into regular human insulin, NPH (intermediate-acting) insulin, premixed human insulin, and others. The most dominant segment is Premixed Human Insulin, driven by simplicity for patients requiring both basal and mealtime coverage. The second most dominant is NPH (Intermediate-Acting) Insulin. Premixed Human Insulin dominates due to its convenience in reducing injection frequency and dosing errors, helping drive market growth by improving patient compliance and adherence in large Type 2 diabetes populations worldwide.

Based on Application Segment, the Human Insulin market is divided into type 1 diabetes and type 2 diabetes. The most dominant segment is Type 2 Diabetes, reflecting the sheer volume of patients needing insulin supplementation. The second most dominant is Type 1 Diabetes. Type 2 Diabetes leads because of its higher prevalence and progressive nature, requiring insulin in advanced stages, propelling market expansion through sustained long-term therapy needs and increasing diagnosis rates globally.

Based on the End-User Segment, the Human Insulin market is divided into hospitals, retail pharmacies, homecare settings, clinics, and others. The most dominant segment is Retail Pharmacies, facilitated by easy access for chronic self-management. The second most dominant is Homecare Settings. Retail Pharmacies dominate due to widespread availability, patient convenience for refills, and strong pharmacy-led counseling programs that enhance adherence and drive repeat purchases in outpatient settings.

Recent Developments

- In March 2023, Sanofi launched Soliqua (insulin glargine/lixisenatide) in pre-filled pen format in India following CDSCO approval, expanding access to combination therapies.

- In December 2024, Eli Lilly and EVA Pharma secured regulatory approval for locally manufactured insulin glargine in Egypt, strengthening affordable supply in Africa.

- In November 2022, the U.S. FDA approved Rezvoglar, the second interchangeable biosimilar insulin glargine, enhancing competition in the human insulin space.

- In September 2023, Novo Nordisk partnered with Aspen Pharmacare to establish local human insulin production facilities in South Africa.

- In December 2024, Cipla received CDSCO approval to launch inhalation insulin in India, introducing a novel non-injectable delivery option.

Regional Analysis

- North America to dominate the global market

North America leads the Human Insulin market with advanced healthcare systems, high diabetes awareness, and strong reimbursement frameworks that support widespread access to both branded and biosimilar products. The region benefits from early adoption of new formulations and robust clinical research infrastructure. The United States dominates within North America, driven by large patient pools, the presence of major manufacturers, and policies promoting biosimilar competition that ensure affordability while maintaining high-quality standards across hospital and retail channels.

Europe represents a mature and regulated market for Human Insulin, supported by universal healthcare coverage and strict biosimilar approval pathways that encourage cost-effective options. Collaborative diabetes management programs enhance patient education and adherence. Germany leads the region, leveraging its strong pharmaceutical manufacturing base and focus on chronic disease management to integrate human insulin seamlessly into national health strategies for both Type 1 and Type 2 patients.

Asia Pacific is experiencing rapid expansion in the Human Insulin market due to surging diabetes incidence, improving healthcare access, and government initiatives for local biosimilar production. Rising middle-class populations drive demand for affordable therapies. China dominates, with its massive diabetic population and strategic push toward domestic manufacturing that reduces import dependency while expanding distribution networks to rural and urban areas alike.

Latin America shows steady progress in the Human Insulin market, supported by public health programs targeting diabetes and increasing availability of biosimilars. Brazil leads, with expanding insurance coverage and growing awareness campaigns that promote early insulin initiation and consistent supply through retail and hospital channels.

The Middle East & Africa region demonstrates emerging growth in the Human Insulin market, driven by rising urbanization, lifestyle changes, and investments in local production facilities. The United Arab Emirates and South Africa lead through strategic partnerships and public-private initiatives that improve the affordability and accessibility of essential human insulin products across diverse healthcare settings.

Competitive Analysis

The global Human Insulin market is dominated by players:

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi S.A.

- Biocon Limited

- Wockhardt Ltd.

- Julphar

- Tonghua Dongbao Pharmaceutical Co., Ltd.

- Gan & Lee Pharmaceuticals

- ADOCIA

- Boehringer Ingelheim

The global Human Insulin market is segmented as follows:

By Type

- Regular Human Insulin

- NPH (Intermediate-Acting) Insulin

- Premixed Human Insulin

By Application

- Type 1 Diabetes

- Type 2 Diabetes

By End-User

- Hospitals

- Retail Pharmacies

- Homecare Settings

- Clinics

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi S.A.

- Biocon Limited

- Wockhardt Ltd.

- Julphar

- Tonghua Dongbao Pharmaceutical Co., Ltd.

- Gan & Lee Pharmaceuticals

- ADOCIA

- Boehringer Ingelheim

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors