![]()

Search Market Research Report

Hardware Products of Doors and Windows Market Size, Share Global Analysis Report, 2026-2034

Hardware Products of Doors and Windows Market Size, Share, Growth Analysis Report By Product (Locks, Handles, Hinges, Fasteners, Latches, and Others), By Material (Aluminum, Stainless Steel, Zinc, Brass, and Plastic), By End-User (Residential, Commercial, and Industrial), By Distribution Channel (Offline and Online), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

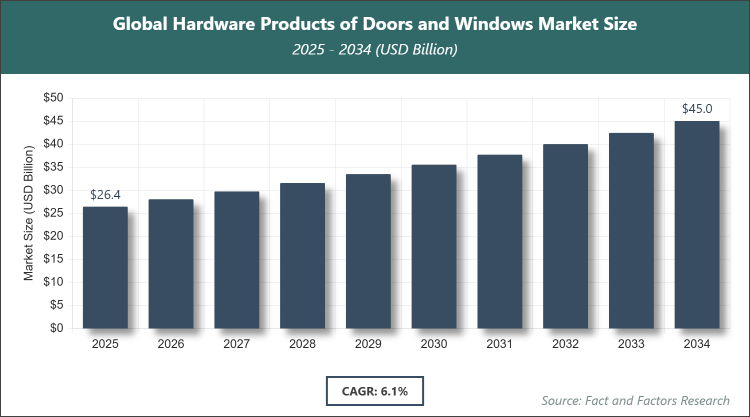

According to Facts & Factors, the global Hardware Products of Doors and Windows market size was estimated at USD 26.44 billion in 2025 and is expected to reach USD 47.14 billion by the end of 2034. The Hardware Products of Doors and Windows industry is anticipated to grow by a CAGR of 6.1% between 2026 and 2034. The Hardware Products of Doors and Windows Market is driven by rising construction activities and increasing adoption of smart and automated door and window solutions.

Market Overview

Market Overview

The Hardware Products of Doors and Windows market encompasses a wide range of components essential for the functionality, security, and aesthetics of doors and windows in residential, commercial, and industrial settings. This market includes items such as locks, handles, hinges, fasteners, and latches, which are critical for ensuring smooth operation, durability, and safety in building structures. These hardware products are manufactured from various materials like metals and plastics to meet diverse requirements, from basic mechanical needs to advanced smart features integrated with modern technology. The market serves as a vital part of the broader construction and building materials industry, supporting everything from new builds to renovations by providing reliable and innovative solutions that enhance user experience and building efficiency.

Key Insights

- As per the analysis shared by our research analyst, the global Hardware Products of Doors and Windows market is expected to grow annually at a CAGR of around 6.1% (2026-2034).

- In terms of revenue, the global Hardware Products of Doors and Windows market size was valued at around USD 26.44 billion in 2025 and is expected to reach USD 47.14 billion by 2034.

- Hardware Products of Doors and Windows market is projected to grow at a significant rate due to the rising construction of commercial establishments and growing investments in automated doors and windows.

- Based on product, the locks segment is anticipated to hold the largest market share of 30%.

- The locks segment dominates due to heightened global security concerns, increasing demand for advanced locking mechanisms in both residential and commercial buildings, and the integration of smart locks with IoT technology, which enhances user convenience and drives overall market expansion.

- Based on material, the aluminum segment is anticipated to hold the largest market share of 40%.

- The aluminum segment leads because of its lightweight, corrosion-resistant properties, cost-effectiveness, and versatility in modern architectural designs, making it ideal for high-volume applications in urban construction projects and contributing significantly to market growth through improved durability and energy efficiency.

- Based on end-user, the residential segment is anticipated to hold the largest market share of 50%.

- The residential segment is dominant owing to rapid urbanization, rising home ownership rates, and extensive renovation activities, where hardware products are essential for enhancing home security and aesthetics, thereby fueling market demand through large-scale consumer adoption.

- Based on distribution channel, the offline segment is anticipated to hold the largest market share of 70%.

- The offline segment prevails due to the preference for physical inspection of products, immediate availability, and expert guidance from retailers, which builds consumer trust and supports bulk purchases in construction sectors, accelerating market penetration.

- Regionally, the Asia Pacific is leading the market in 2025 with a market share of 45%.

- The Asia Pacific region dominates because of booming construction industries in emerging economies, massive urbanization projects, and government initiatives for infrastructure development, which create substantial demand for durable and innovative hardware solutions.

Market Dynamics

Growth Drivers

- Rising Construction of Commercial Establishments

The surge in construction of commercial spaces such as hotels, shopping malls, and restaurants is a primary driver for the Hardware Products of Doors and Windows market. This trend is fueled by global economic growth and urbanization, leading to increased demand for high-quality, functional hardware that ensures security, accessibility, and aesthetic appeal in these establishments. As businesses expand, the need for robust doors and windows equipped with advanced hardware becomes essential to meet regulatory standards and customer expectations, thereby propelling market growth.

Furthermore, the integration of hardware with modern architectural designs in commercial projects enhances operational efficiency and user experience. Innovations in hardware, such as automated systems and energy-efficient components, align with the sustainability goals of commercial developers, reducing long-term costs and environmental impact. This driver not only boosts immediate demand but also encourages ongoing investments in research and development for more advanced products.

Restraints

- Longer Replacement Rate of Hardware Products

The durability and long lifespan of hardware products for doors and windows act as a significant restraint, as they reduce the frequency of replacements and limit recurring revenue streams. Once installed, these items often last for decades with minimal maintenance, leading to slower market turnover and challenges for manufacturers in sustaining continuous sales growth. This factor is particularly pronounced in mature markets where existing infrastructure is already equipped with high-quality hardware.

Additionally, the extended replacement cycle discourages rapid adoption of new technologies, as end-users may delay upgrades due to the reliability of current installations. This can hinder innovation diffusion and market expansion, especially in cost-sensitive segments where budget constraints prioritize longevity over frequent updates. Manufacturers must navigate this by focusing on value-added features to encourage voluntary replacements.

Opportunities

- Increasing Launch of New-Age Products

The frequent introduction of innovative hardware products, such as smart locks and digital handles, presents substantial opportunities for market expansion. Companies are leveraging technology to create user-friendly, connected solutions that appeal to tech-savvy consumers and integrate seamlessly with smart home ecosystems. This trend opens new revenue channels through premium pricing and partnerships with tech firms, driving differentiation in a competitive landscape.

Moreover, these new-age products address evolving consumer needs for convenience, security, and customization, fostering loyalty and repeat business. As awareness grows, particularly in emerging markets, the opportunity to capture untapped segments increases, supported by marketing strategies that highlight benefits like remote access and energy savings. This positions the market for sustained growth through continuous product evolution.

Challenges

- Extreme Competitiveness in the Industry

The intense competition among international, regional, and domestic players poses a major challenge, leading to price wars and market saturation. Companies must constantly innovate to maintain differentiation, which increases operational costs and pressures profit margins. This environment demands strategic agility to balance quality, pricing, and distribution in a fragmented market.

In addition, managing product differentiation amid similar offerings requires robust branding and supply chain efficiency. Challenges are amplified in price-sensitive regions where low-cost alternatives from unorganized sectors undermine established players. Overcoming this involves investing in R&D and building strong customer relationships to secure market share.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 26.44 Billion |

Projected Market Size in 2034 |

USD 47.14 Billion |

CAGR Growth Rate |

6.1% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Dormakaba, Assa Abloy, Andersen Corporation, Allegion, Stanley Black & Decker, Yale, Roto Frank AG, Schlage, SIEGENIA Group, Pella Corporation, Masonite International, Marvin Windows and Doors, HOPPE AG, Emtek Products Inc., Jeld-Wen, and Others. |

Key Segment |

By Product, By Material, By End-User, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Hardware Products of Doors and Windows market is segmented by product, material, end-user, distribution channel, and region.

Based on Product Segment, the Hardware Products of Doors and Windows market is divided into locks, handles, hinges, fasteners, latches, and others. The most dominant segment is locks, followed by handles as the second most dominant. The locks segment is most dominant because it addresses critical security needs in an era of rising crime rates and smart home integration, driving market growth through demand for advanced, tamper-proof mechanisms that enhance overall building safety and user confidence. The handles segment is the second most dominant due to its essential role in daily usability and aesthetic enhancement, contributing to market expansion by offering customizable designs that align with modern interior trends and improve accessibility in diverse applications.

Based on Material Segment, the Hardware Products of Doors and Windows market is divided into aluminum, stainless steel, zinc, brass, and plastic. The most dominant segment is aluminum, followed by stainless steel as the second most dominant. The aluminum segment is most dominant owing to its superior strength-to-weight ratio, resistance to corrosion, and affordability, which make it ideal for large-scale construction projects, thereby propelling market growth through widespread adoption in energy-efficient and sustainable building practices. The stainless steel segment is the second most dominant because of its exceptional durability, aesthetic appeal, and hygiene properties, supporting market development by catering to high-end applications where longevity and low maintenance are prioritized.

Based on End-User Segment, the Hardware Products of Doors and Windows market is divided into residential, commercial, and industrial. The most dominant segment is residential, followed by commercial as the second most dominant. The residential segment is most dominant due to the global housing boom and renovation trends, where hardware enhances home security and style, driving market growth via increased consumer spending on personalized and smart solutions. The commercial segment is the second most dominant as it benefits from expanding business infrastructures like offices and retail spaces, contributing to market advancement through demand for reliable, high-traffic hardware that ensures operational efficiency.

Based on Distribution Channel Segment, the Hardware Products of Doors and Windows market is divided into offline and online. The most dominant segment is offline, followed by online as the second most dominant. The offline segment is most dominant because it allows for tactile product evaluation and expert consultations, fostering trust in purchases for construction needs and accelerating market growth through established retail networks. The online segment is the second most dominant with its convenience and wide reach, aiding market expansion by enabling easy access to diverse products and competitive pricing for global consumers.

Recent Developments

- In June 2023, Godrej Locks & Architectural Fittings and Systems (GLAFS) expanded its Architectural Fittings Category with new Home Décor Handles and digital locks, aiming to meet the growing demand for stylish and tech-integrated hardware solutions in residential spaces.

- In June 2022, Tesa Assa Abloy launched a new range of doors and window handles suited for state-of-the-art surroundings, enhancing product offerings with modern designs that cater to contemporary architectural requirements and user preferences.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region stands out for its rapid urbanization and massive infrastructure investments, particularly in countries like China and India, where booming populations drive extensive residential and commercial construction. China, as the dominating country, leads with government-backed projects such as smart cities and high-speed rail networks that require advanced hardware for doors and windows. This region's focus on affordable yet durable materials fosters innovation in manufacturing, attracting global suppliers and creating a vibrant ecosystem for hardware production. The blend of traditional craftsmanship with modern technology further strengthens its position, enabling efficient supply chains that cater to both domestic and export demands. Cultural emphasis on security and aesthetics also plays a role, encouraging the adoption of multifunctional products that enhance living standards.

North America exhibits steady growth through its emphasis on renovation and energy-efficient building practices, with the United States as the dominating country due to its large housing market and stringent building codes. The region's advanced technological landscape promotes the integration of smart hardware, such as automated locks and sensors, into everyday structures. Strong consumer awareness about sustainability drives demand for eco-friendly materials, supporting local manufacturers in developing innovative solutions. Economic stability allows for consistent investments in commercial real estate, where high-quality hardware ensures compliance with safety standards. Collaborative efforts between industry players and regulatory bodies further enhance market maturity, positioning North America as a hub for premium hardware advancements.

Europe maintains a strong presence with its heritage in architectural excellence and focus on sustainable development, led by Germany as the dominating country through its engineering prowess and export-oriented economy. The region's strict environmental regulations encourage the use of recyclable and low-emission hardware materials, aligning with green building initiatives. Historical preservation projects blend traditional designs with modern functionality, creating niche opportunities for specialized products. Collaborative research in materials science drives innovations like corrosion-resistant alloys, benefiting diverse climates across the continent. Consumer preferences for high-end, customizable hardware in residential and commercial spaces underscore Europe's role in setting global quality benchmarks.

Latin America shows promising potential amid economic recovery and urban expansion, with Brazil as the dominating country due to its vast construction sector and natural resource abundance. Infrastructure projects, including housing programs and tourism developments, increase demand for cost-effective hardware solutions. The region's tropical climates necessitate weather-resistant products, spurring local innovations in durable materials. Growing middle-class populations boost residential renovations, incorporating security-focused hardware to address urban challenges. Trade agreements facilitate imports of advanced technologies, enhancing product diversity and market competitiveness.

The Middle East & Africa region is emerging with investments in mega-projects and diversification efforts, dominated by the United Arab Emirates through ambitious developments like smart cities and luxury resorts. Oil-rich economies fund high-profile constructions requiring premium hardware for security and aesthetics. Africa's urbanization wave, particularly in South Africa, drives affordable housing initiatives that rely on basic yet reliable components. Climate adaptability is key, with products designed for extreme conditions gaining traction. International partnerships bring technological transfers, supporting local manufacturing growth and job creation in the sector.

Competitive Analysis

The global Hardware Products of Doors and Windows market is dominated by players:

- Dormakaba

- Assa Abloy

- Andersen Corporation

- Allegion

- Stanley Black & Decker

- Yale

- Roto Frank AG

- Schlage

- SIEGENIA Group

- Pella Corporation

- Masonite International

- Marvin Windows and Doors

- HOPPE AG

- Emtek Products Inc.

- Jeld-Wen

The global Hardware Products of Doors and Windows market is segmented as follows:

By Product

- Locks

- Handles

- Hinges

- Fasteners

- Latches

- Others

By Material

- Aluminum

- Stainless Steel

- Zinc

- Brass

- Plastic

By End-User

- Residential

- Commercial

- Industrial

By Distribution Channel

- Offline

- Online

By Regional Segment Analysis

-

North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global Hardware Products of Doors and Windows market is dominated by players:

- Dormakaba

- Assa Abloy

- Andersen Corporation

- Allegion

- Stanley Black & Decker

- Yale

- Roto Frank AG

- Schlage

- SIEGENIA Group

- Pella Corporation

- Masonite International

- Marvin Windows and Doors

- HOPPE AG

- Emtek Products Inc.

- Jeld-Wen

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors