![]()

Search Market Research Report

GPU as a Service Market Size, Share Global Analysis Report, 2026-2034

GPU as a Service Market Size, Share, Growth Analysis Report By Deployment Model (Private GPU Cloud, Public GPU Cloud, and Hybrid GPU Cloud), By Enterprise Type (Small & Medium-sized Enterprises and Large Enterprises), By Pricing Model (Pay-as-you-go and Subscription-based), By Application (Healthcare, BFSI, Manufacturing, IT & Telecommunication, Automotive, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

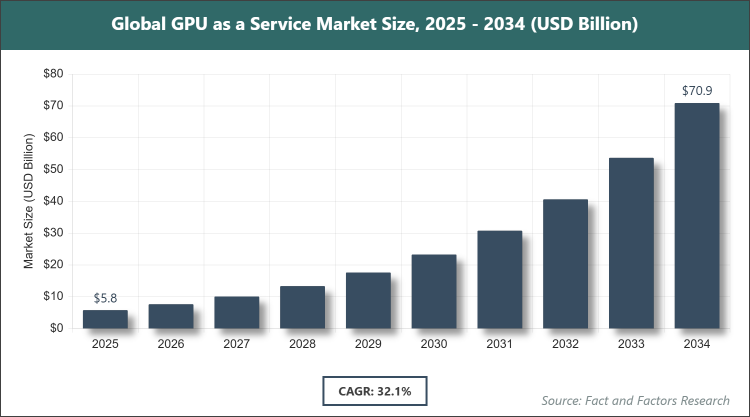

[220+ Pages Report] According to Facts & Factors, the global GPU as a Service market size was estimated at USD 5.79 billion in 2025 and is expected to reach USD 72.49 billion by the end of 2034. The GPU as a Service industry is anticipated to grow by a CAGR of 32.10% between 2026 and 2034. The GPU as a Service Market is driven by rising demand for GPU-intensive applications such as AI and ML.

Market Overview

Market Overview

The GPU as a Service market refers to the provision of cloud-based graphics processing units that allow users to access high-performance computing resources remotely without the need for owning physical hardware. This service enables scalable processing for data-intensive tasks in fields like artificial intelligence, machine learning, scientific simulations, and graphics rendering, offering flexibility and cost savings through on-demand usage models.

Key Insights

- As per the analysis shared by our research analyst, the global GPU as a Service market is estimated to grow annually at a CAGR of around 32.10% over the forecast period (2026-2034).

- In terms of revenue, the global GPU as a Service market size was valued at around USD 5.79 Billion in 2025 and is projected to reach USD 72.49 Billion by 2034.

- The market is driven by rapid cloud computing and AI/ML adoption across industries.

- Based on Deployment Model, Private GPU Cloud dominated with 53.07% share due to high security needs amid rising cyber threats.

- Based on Enterprise Type, Large Enterprises dominated with 61.30% share due to avoidance of hardware maintenance burdens.

- Based on Pricing Model, Pay-as-you-go dominated with 72.93% share due to cost-efficiency and flexibility for variable workloads.

- Based on Application, IT & Telecommunication dominated with 22.21% share due to massive data generation and need for analytics/ML.

- North America dominated the global market with a share of 38.90% due to strong AI investments and advanced cloud infrastructure.

Growth Drivers

- Rising Demand for GPU-Intensive Applications

The increasing reliance on applications such as artificial intelligence, machine learning, video editing, and blockchain has significantly boosted the need for powerful GPU resources. These applications require high computational power for processing large datasets and complex algorithms, which GPU as a Service provides efficiently without upfront hardware investments. This driver is particularly prominent in industries like IT and manufacturing, where real-time data processing and simulations are critical for innovation and operational efficiency.

Furthermore, the integration of IoT devices generates vast amounts of data that demand real-time analytics, further propelling the adoption of GPUaaS. Post-pandemic shifts toward remote work and digital transformation have accelerated this trend, as businesses seek scalable solutions to handle fluctuating workloads while minimizing costs.

Restraints

- Data Security Concerns

Cloud-based services inherently involve risks such as cyberattacks, unauthorized access, and data breaches, which deter some organizations from adopting GPU as a Service. With sensitive information stored remotely, concerns over compliance and privacy regulations amplify these issues, especially in sectors like healthcare and finance.

Additionally, the prevalence of malware and ransomware attacks on cloud infrastructures has led to hesitation among potential users, requiring providers to invest heavily in security measures. This restraint is more pronounced in regions with stringent data protection laws, potentially slowing market penetration.

Opportunities

- Growth in Generative AI

The surge in generative AI technologies for content creation, image synthesis, and natural language processing opens new avenues for GPUaaS, as these require immense computational resources for training and inference. Providers can capitalize on this by offering specialized services tailored to AI developers and enterprises.

Moreover, government initiatives promoting AI adoption in emerging economies present expansion opportunities, allowing market players to tap into underserved regions with customized, scalable solutions.

Challenges

- Low Awareness in Developing Economies

Limited understanding and slow adoption of AI and ML technologies in developing regions hinder market growth, as businesses may not recognize the benefits of GPUaaS over traditional computing. This challenge is compounded by inadequate infrastructure and skill gaps.

Overcoming this requires educational efforts and partnerships to demonstrate value, but it remains a barrier to achieving uniform global expansion.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 5.79 Billion |

Projected Market Size in 2034 |

USD 72.49 Billion |

CAGR Growth Rate |

32.10% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Amazon Web Services, Inc., Google, Microsoft, Vultr, IBM Corporation, Alibaba Cloud, Linode LLC., OVH SAS, Lambda Labs, Hewlett Packard Enterprise Development LP, CoreWeave, and Others. |

Key Segment |

By Deployment Model, By Enterprise Type, By Pricing Model, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The GPU as a Service market is segmented by deployment model, enterprise type, pricing model, application, and region.

Based on Deployment Model Segment, the GPU as a Service market is divided into Private GPU Cloud, Public GPU Cloud, Hybrid GPU Cloud, and others. The most dominant subsegment is Private GPU Cloud, holding a 53.07% share, primarily because it offers enhanced security and control over data, which is crucial for industries handling sensitive information amid increasing cyber threats. This dominance drives the market by enabling compliance with regulations and reducing breach risks, fostering trust among large enterprises. The second most dominant is Hybrid GPU Cloud, which is growing rapidly due to its balance of cost-effectiveness, scalability, and security, allowing users to leverage public cloud flexibility while maintaining private control for critical workloads, thus supporting diverse operational needs and accelerating overall market adoption.

Based on Enterprise Type Segment, the GPU as a Service market is divided into Small & Medium-sized Enterprises, Large Enterprises, and others. The most dominant subsegment is Large Enterprises, with a 61.30% share, as they benefit from avoiding the high costs and complexities of hardware maintenance, allowing focus on core business activities. This drives market growth by enabling seamless scaling for extensive data processing demands in global operations. The second most dominant is Small & Medium-sized Enterprises, experiencing the highest CAGR of 37.20%, due to their increasing digital adaptation and need for affordable, competitive computing solutions, which helps bridge technological gaps and promotes innovation in smaller businesses.

Based on Pricing Model Segment, the GPU as a Service market is divided into Pay-as-you-go, Subscription-based, and others. The most dominant subsegment is Pay-as-you-go, capturing 72.93% share, owing to its cost-efficiency and flexibility for handling variable workloads without long-term commitments. This model propels market expansion by attracting startups and seasonal users who prioritize budget control. The second most dominant is Subscription-based, preferred for consistent high-usage scenarios, providing predictable costs and dedicated resources that support stable, long-term projects and enhance user retention.

Based on Application Segment, the GPU as a Service market is divided into Healthcare, BFSI, Manufacturing, IT & Telecommunication, Automotive, and others. The most dominant subsegment is IT & Telecommunication, with 22.21% share, driven by the sector's massive data volumes and reliance on analytics and ML for network optimization and customer insights. This dominance fuels market growth through continuous innovation in data-driven services. The second most dominant is Manufacturing, boasting the highest CAGR of 38%, as it adopts HPC for simulations and modeling, improving efficiency and reducing time-to-market for products.

Recent Developments

- In April 2023, Catalyst Cloud launched NVIDIA A100 GPU as a Service in New Zealand to support high-performance computing needs.

- In May 2022, atNorth introduced GPU as a Service for HPC workloads, enhancing capabilities for data-intensive applications.

- In February 2023, Vultr expanded its NVIDIA A16 GPU offerings to cater to growing demand in graphics and AI processing.

- In January 2024, WekaIO partnered with NexGen Cloud for Hyperstack GPU as a Service, focusing on advanced AI infrastructure.

- In December 2023, Yotta Infrastructure collaborated with NVIDIA for GPU computing on Shakti Cloud, boosting AI development in India.

- In April 2023, CoreWeave raised USD 221 million for GPU expansion to scale cloud-based GPU resources.

- In March 2023, Lambda Labs raised USD 44 million to deploy NVIDIA H100 GPUs, advancing AI training capabilities.

- In September 2022, Super Micro Computer launched an 8U GPU server for AI training, supporting large-scale computations.

Regional Analysis

- North America to dominate the global market

North America leads the GPU as a Service market due to its robust technological ecosystem, substantial investments in AI research, and presence of major cloud providers. The region's advanced data centers and high adoption of cloud services facilitate seamless integration of GPUaaS for diverse applications. Dominating countries like the United States benefit from government funding in AI and a concentration of tech giants, driving innovation and market expansion. Canada contributes through its growing startup scene and focus on sustainable computing, while Mexico emerges with increasing foreign investments in IT infrastructure.

Asia Pacific ranks as the third-largest market but exhibits the highest growth potential, fueled by rapid digitalization and government-backed AI initiatives. China dominates within the region with massive investments in cloud infrastructure and AI development, supported by national strategies to become a global tech leader. Japan excels in automotive and manufacturing applications, leveraging GPUaaS for advanced simulations. India surges ahead with its booming IT sector and affordable cloud adoption among SMEs, while South Korea and ASEAN countries add momentum through electronics and e-commerce growth.

Europe holds the second-largest position with strong emphasis on AI ethics, data privacy, and HPC adoption across industries. Germany leads as the dominating country, driven by its manufacturing prowess and Industry 4.0 initiatives that integrate GPUaaS for smart factories. The United Kingdom advances through fintech and research institutions utilizing cloud GPUs for ML. France focuses on AI in healthcare and automotive, while Nordic countries prioritize sustainable tech solutions, contributing to regional innovation and regulatory compliance.

South America shows promising growth from emerging startup ecosystems and increasing cloud penetration in key sectors. Brazil dominates the region with its large economy and investments in digital transformation, particularly in agriculture and finance using GPUaaS for data analytics. Argentina follows with tech hubs fostering AI adoption, while the rest of South America benefits from multinational expansions and government efforts to bridge digital divides.

The Middle East & Africa represents the fourth-largest market, with growth centered on economic diversification through technology. The GCC countries, led by the UAE and Saudi Arabia, dominate with ambitious AI visions and investments in smart cities and oil analytics via GPUaaS. Israel excels in tech innovation and cybersecurity applications, while South Africa drives adoption in mining and healthcare, supported by improving infrastructure and international partnerships.

Competitive Analysis

The global GPU as a Service market is dominated by players:

- Amazon Web Services, Inc.

- Microsoft

- Vultr

- IBM Corporation

- Alibaba Cloud

- Linode LLC.

- OVH SAS

- Lambda Labs

- Hewlett Packard Enterprise Development LP

- CoreWeave

The global GPU as a Service market is segmented as follows:

By Deployment Model

- Private GPU Cloud

- Public GPU Cloud

- Hybrid GPU Cloud

By Enterprise Type

- Small & Medium-sized Enterprises

- Large Enterprises

By Pricing Model

- Pay-as-you-go

- Subscription-based

By Application

- Healthcare

- BFSI

- Manufacturing

- IT & Telecommunication

- Automotive

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global GPU as a Service market is dominated by players:

- Amazon Web Services, Inc.

- Microsoft

- Vultr

- IBM Corporation

- Alibaba Cloud

- Linode LLC.

- OVH SAS

- Lambda Labs

- Hewlett Packard Enterprise Development LP

- CoreWeave

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors