![]()

Search Market Research Report

Fire Retardant Treated Wood Market Size, Share Global Analysis Report, 2026-2034

Fire Retardant Treated Wood Market Size, Share, Growth Analysis Report By Treatment Type (Pressure-impregnated FRTW, Surface-coated FRTW, Non-pressure/diffusion treatments, and Others), By Product Type (Plywood, Dimensional lumber, Oriented strand board (OSB), Decking and fencing, and Others), By Application (Interior applications, Exterior applications, and Others), By End-User Industry (Residential construction, Commercial buildings, Institutional buildings, Industrial facilities, Public infrastructure and transport hubs, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

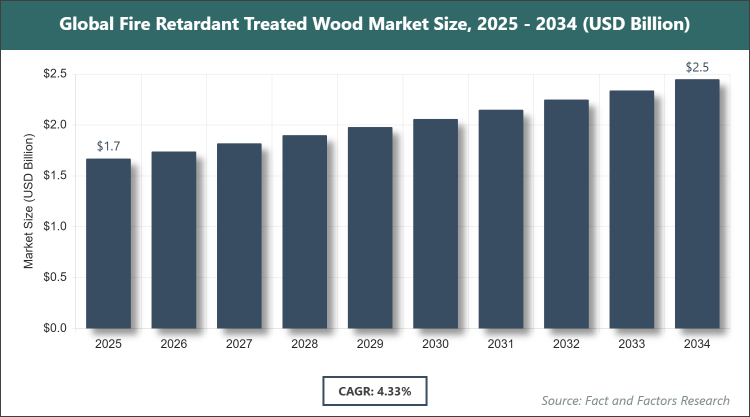

[220+ Pages Report] According to Facts & Factors, the global Fire Retardant Treated Wood market size was estimated at USD 1.67 billion in 2025 and is expected to reach USD 2.44 billion by the end of 2034. The Fire Retardant Treated Wood industry is anticipated to grow by a CAGR of 4.33% between 2026 and 2034. The Fire Retardant Treated Wood Market is driven by increasing demand for fire-safe construction materials.

Market Overview

Market Overview

Fire-retardant-treated wood refers to lumber and wood-based products that have undergone chemical treatments to enhance their resistance to ignition, flame spread, and combustion, making them suitable for applications where fire safety is a priority. This market encompasses the production, distribution, and utilization of such treated wood across various sectors, focusing on materials that meet stringent building codes and safety standards without compromising structural integrity or aesthetic appeal. The industry involves specialized processes like pressure impregnation or surface coatings to infuse fire-retardant chemicals into the wood fibers, thereby reducing the risk of fire propagation in buildings and infrastructure.

Key Insights

- As per the analysis shared by our research analyst, the Fire Retardant Treated Wood market is estimated to grow annually at a CAGR of around 4.33% over the forecast period (2026-2034).

- In terms of revenue, the Fire Retardant Treated Wood market size was valued at around USD 1.67 billion in 2025 and is projected to reach USD 2.44 billion by 2034.

- Due to a variety of driving factors, the market is predicted to rise at a significant rate. The Fire Retardant Treated Wood Market is driven by growing demand for fire-safe construction materials, strict building codes, and increasing use in commercial and institutional buildings.

- Based on the Treatment Type, the Pressure-impregnated segment dominated the market in 2025 with a market share of 61.83% and why it is due to its superior durability in structural applications and effectiveness in anchoring chemicals deep into the wood for long-term fire resistance.

- Based on the Product Type, the Plywood segment dominated the market in 2025 with a market share of 46.71% and why it is dominated because of its widespread use in mature supply chains, proven compatibility with fasteners, and versatility in both interior and exterior constructions.

- Based on the Application, the Interior applications segment dominated the market in 2025 with a market share of 59.28% and this is dominated owing to life-safety codes emphasizing egress and structural integrity in elements like flooring, sub-floors, and roof trusses.

- Based on the End-User Industry, the Commercial buildings segment dominated the market in 2025 with a market share of 38.65% and why it is because it integrates fire-retardant-treated wood for framing in office towers, retail malls, and data centers to optimize leasable spaces while ensuring compliance.

- Based on region, North America was the leading revenue generator in 2025, holding a market share of 43.36%, due to intensified wildfire seasons, insurer-driven retrofits, and code convergence facilitating cross-border supply chains.

Growth Drivers

- Increasing Demand for Fire-Safe Construction Materials

The rising awareness of fire hazards in urban and wildfire-prone areas has propelled the adoption of fire-retardant-treated wood as a critical component in modern construction practices. This demand stems from the need to enhance building resilience against fire outbreaks, particularly in regions experiencing climate-induced risks, where traditional wood materials fall short in providing adequate protection.

Furthermore, the integration of these materials into sustainable building designs aligns with global efforts to reduce carbon footprints while prioritizing safety, driving innovation in treatment technologies that offer both environmental benefits and superior performance.

Restraints

- High Cost Compared to Non-Treated Wood

The premium pricing of fire retardant treated wood, often 25-40% higher than untreated alternatives, poses a significant barrier, especially in cost-sensitive markets or during economic downturns when lumber prices fluctuate. This cost differential arises from specialized manufacturing processes, including additional kiln drying and chemical impregnation, which increase production expenses.

Additionally, the need for segregated storage and handling to maintain certification standards further elevates operational costs, limiting accessibility for smaller-scale projects and hindering broader market penetration in developing economies.

Opportunities

- Integration with Green Building and LEED-Certified Projects

The growing emphasis on sustainable construction opens avenues for fire retardant treated wood in eco-friendly initiatives, where it supports carbon-credentialed materials in mass-timber structures and resilient infrastructure. This opportunity is amplified by certifications that highlight low-emission treatments, appealing to environmentally conscious developers.

Moreover, partnerships with green building councils can facilitate market expansion, as treated wood meets criteria for energy-efficient and low-impact designs, fostering innovation in non-toxic formulations that enhance appeal in premium segments.

Challenges

- Limited Moisture Resistance in Exterior Applications

Exposure to wet-dry cycles in outdoor settings can lead to chemical leaching, compromising the fire-retardant properties and requiring additional protective measures like sealants, which add complexity and cost. This challenge is particularly acute in humid or coastal climates, restricting reliable use in unprotected facades or decks.

Ongoing research into advanced coatings aims to mitigate this, but the lack of long-term field data tempers architect and specifier confidence, potentially slowing adoption in high-exposure applications.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.67 Billion |

Projected Market Size in 2034 |

USD 2.44 Billion |

CAGR Growth Rate |

4.33% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Viance, Flameproof Company, Arxada, HOOVER TREATED WOOD PRODUCTS, Koppers, and Others. |

Key Segment |

By Treatment Type, By Product Type, By Application, By End-User Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Fire Retardant Treated Wood market is segmented by Treatment Type, Product Type, Application, End-User Industry, and region.

Based on Treatment Type Segment, the Fire Retardant Treated Wood market is divided into Pressure-impregnated FRTW, Surface-coated FRTW, Non-pressure/diffusion treatments, and others. The most dominant segment is Pressure-impregnated FRTW, which leads due to its deep penetration of chemicals, ensuring long-lasting fire resistance and suitability for structural elements, driving the market by enabling compliance with stringent safety codes in high-risk buildings. The second most dominant is Surface-coated FRTW, prominent for its ease of application and aesthetic preservation, contributing to market growth through expanded use in decorative and weathering-exposed scenarios where quick retrofits are needed.

Based on Product Type Segment, the Fire Retardant Treated Wood market is divided into Plywood, Dimensional lumber, Oriented strand board (OSB), Decking and fencing, and others. The most dominant segment is Plywood, excelling because of its layered construction that enhances fire-retardant efficacy and broad applicability in sheathing and panels, propelling the market via efficient supply chains and reduced labor in modular builds. The second most dominant is Dimensional lumber, valued for its strength in framing and load-bearing roles, boosting market expansion by supporting taller timber structures under evolving codes.

Based on Application Segment, the Fire Retardant Treated Wood market is divided into Interior applications, Exterior applications, and others. The most dominant segment is Interior applications, leading owing to mandatory codes for flame-spread control in enclosed spaces like walls and ceilings, advancing the market through safer indoor environments in commercial and residential settings. The second most dominant is Exterior applications, gaining traction from wildfire mitigation requirements, fueling growth via durable claddings and decks that qualify for insurance incentives.

Based on End-User Industry Segment, the Fire Retardant Treated Wood market is divided into Residential construction, Commercial buildings, Institutional buildings, Industrial facilities, Public infrastructure and transport hubs, and others. The most dominant segment is Commercial buildings, dominating due to high-volume use in optimizing space and meeting occupancy safety standards, driving the market with large-scale projects like malls and offices. The second most dominant is Institutional buildings, essential for public safety in schools and hospitals, contributing to market progress through government-funded upgrades emphasizing egress and integrity.

Recent Developments

- In April 2025, T2EARTH, LLC introduced OnWood Plywood, an innovative, eco-friendly fire-retardant treated wood product that eliminates toxic chemicals while delivering exceptional strength, Class A fire retardancy, and sustainability features tailored for builders operating in fire-prone regions.

- In May 2025, Culpeper Wood Preservers announced the expansion of its FlamePRO fire-retardant treated lumber line into the Northeast United States, targeting multifamily and commercial construction sectors with improved delivery timelines and enhanced product availability to meet rising demand.

Regional Analysis

- North America to dominate the global market

North America stands as the dominant region in the Fire Retardant Treated Wood market, driven by robust regulatory frameworks and heightened awareness of fire risks. The United States leads as the dominating country, where wildfire-prone states like California enforce strict codes such as Chapter 7A, promoting widespread adoption in residential and commercial builds. This region's emphasis on insurer incentives for retrofits further solidifies its position, with Canada contributing through harmonized standards that facilitate efficient supply chains across borders.

Asia-Pacific emerges as the fastest-growing region, fueled by rapid urbanization and evolving safety regulations. China dominates here, with mandates like GB 55037-2022 requiring Class B1 performance in mid-rise structures, accelerating demand in densely populated cities. Japan's focus on long-term timber durability in seismic zones complements this growth, while India's infrastructure boom in urban centers adds momentum through affordable fire-safe materials.

Europe maintains steady growth, supported by sustainability goals and carbon targets in construction. Germany leads as the key country, leveraging advanced mass-timber innovations in eco-buildings, with the United Kingdom following suit through post-Grenfell reforms emphasizing fire-resistant materials in high-rises. Nordic countries enhance this with their timber heritage, prioritizing treated wood in energy-efficient designs.

South America shows emerging potential, particularly in infrastructure development amid climate challenges. Brazil dominates, driven by urban expansion in fire-vulnerable areas like the Amazon fringe, where treated wood aids in sustainable housing and commercial projects. Argentina contributes through regulatory alignments that encourage safer building practices in growing metropolitan regions.

The Middle East and Africa region experiences gradual uptake, influenced by modernization efforts. Saudi Arabia leads, incorporating fire retardant treated wood in Vision 2030 projects for public hubs and residential complexes, addressing arid climate risks. South Africa supports this with institutional builds in urban centers, focusing on cost-effective safety solutions.

Competitive Analysis

The global Fire Retardant Treated Wood market is dominated by players:

- Viance

- Flameproof Company

- Arxada

- HOOVER TREATED WOOD PRODUCTS

- Koppers

The global Fire Retardant Treated Wood market is segmented as follows:

By Treatment Type

- Pressure-impregnated FRTW

- Surface-coated FRTW

- Non-pressure/diffusion treatments

- Others

By Product Type

- Plywood

- Dimensional lumber

- Oriented strand board (OSB)

- Decking and fencing

- Others

By Application

- Interior applications

- Exterior applications

- Others

By End-User Industry

- Residential construction

- Commercial buildings

- Institutional buildings

- Industrial facilities

- Public infrastructure and transport hubs

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Viance

- Flameproof Company

- Arxada

- HOOVER TREATED WOOD PRODUCTS

- Koppers

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors