![]()

Search Market Research Report

EV Traction Motor Market Size, Share Global Analysis Report, 2026-2034

EV Traction Motor Market Size, Share, Growth Analysis Report By Motor Type (Permanent Magnet Synchronous Motor, AC Induction Motor, Brushless DC Motor, and Others), By Vehicle Type (Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Hybrid Electric Vehicles, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

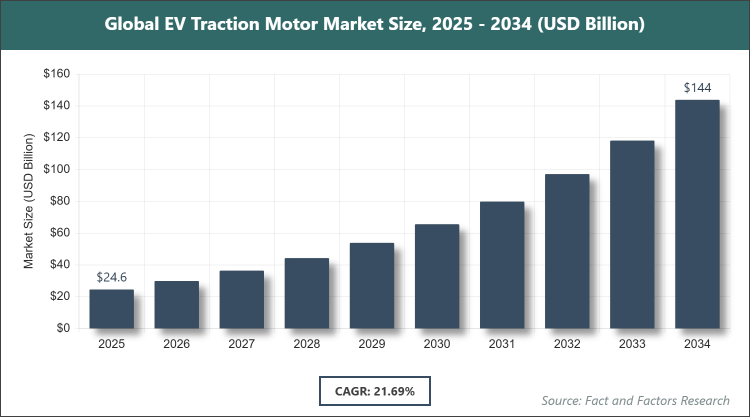

[250 Pages Report] According to Facts & Factors, the global EV Traction Motor market size was estimated at USD 24.58 billion in 2025 and is expected to reach USD 143.85 billion by 2034, growing at a CAGR of 21.69% from 2026 to 2034. The EV Traction Motor Market is driven by increasing electric vehicle penetration and supportive government policies.

EV Traction Motor Market: Overview

EV Traction Motor Market: Overview

The EV traction motor market encompasses the design, production, and distribution of electric motors specifically engineered to propel electric vehicles, converting electrical energy into mechanical torque to drive the wheels. These motors are integral to battery electric, hybrid, and plug-in hybrid vehicles, offering advantages such as high efficiency, instant torque delivery, and reduced maintenance compared to traditional internal combustion engines. The market focuses on innovations in motor technologies to enhance performance, range, and energy efficiency, catering to the growing demand for sustainable transportation solutions without relying on fossil fuels.

Key Insights

- The global EV traction motor market was valued at USD 24.58 billion in 2025 and is projected to reach USD 143.85 billion by 2034.

- The market is expected to grow at a CAGR of 21.69% during the forecast period.

- The EV traction motor market is driven by rising adoption of electric vehicles and advancements in battery technology.

- Based on the motor type segment, the permanent magnet synchronous motor dominates with 60% share due to its high efficiency, torque density, and compact design suitable for modern EVs.

- Based on the vehicle type segment, Battery electric vehicles dominate with 78% share owing to the global push for zero-emission transport and increasing consumer preference for fully electric models.

- Asia Pacific dominates with 54.6% share due to robust EV manufacturing ecosystems and government incentives in countries like China.

Growth Drivers

- Increasing Electric Vehicle Adoption and Government Incentives

The surge in electric vehicle sales worldwide, fueled by consumer awareness of environmental benefits and declining battery costs, has significantly boosted demand for traction motors. Governments are implementing subsidies, tax rebates, and infrastructure investments to promote EV uptake, directly impacting motor production volumes. Technological improvements in motors, such as enhanced cooling systems and higher power outputs, further support this growth by improving vehicle performance and range.

Additionally, stringent emission regulations in regions like Europe and North America are compelling automakers to shift toward electrification, creating a favorable environment for traction motor suppliers. Collaborations between OEMs and motor manufacturers are accelerating innovation, ensuring motors meet evolving standards for efficiency and durability in diverse applications from passenger cars to commercial fleets.

Restraints

- High Manufacturing Costs and Supply Chain Vulnerabilities

The production of advanced traction motors involves expensive rare-earth materials like neodymium, leading to high costs that can hinder market penetration in price-sensitive segments. Volatility in raw material prices, exacerbated by geopolitical factors, poses risks to manufacturers' profitability and supply stability.

Dependency on a limited number of suppliers for critical components, such as magnets and semiconductors, exposes the market to disruptions from events like trade disputes or natural disasters. Moreover, the need for specialized manufacturing facilities adds to capital expenditures, potentially slowing expansion for smaller players and delaying widespread adoption in emerging markets.

Opportunities

- Advancements in Motor Technologies and Emerging Markets

Innovations like axial-flux motors and silicon carbide inverters present opportunities to enhance efficiency and reduce weight, appealing to premium EV segments. The integration of AI for predictive maintenance and smart motor controls can open new revenue streams through value-added services.

Rapid urbanization in Asia and Latin America is driving demand for affordable EVs, creating opportunities for localized production and partnerships. Expanding charging networks and fleet electrification in logistics sectors further amplify potential, allowing manufacturers to diversify into commercial applications and capitalize on sustainability trends.

Challenges

- Thermal Management and Performance Limitations

Effective heat dissipation in high-power motors remains a challenge, as overheating can reduce efficiency and lifespan, particularly in demanding conditions like heavy loads or extreme weather. Balancing power density with thermal constraints requires ongoing R&D investments, complicating design processes.

Competition from alternative technologies, such as hydrogen fuel cells, and the need for standardization across global markets add complexity. Skill shortages in advanced engineering and regulatory variations across regions further impede seamless market growth, necessitating adaptive strategies from industry players.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 24.58 Billion |

Projected Market Size in 2034 |

USD 143.85 Billion |

CAGR Growth Rate |

21.69% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Tesla Inc., BYD Company Ltd., Bosch Mobility Solutions, Siemens AG, Nidec Motor Corporation, ABB Ltd., Magna International Inc., Mitsubishi Electric Corporation, ZF Friedrichshafen AG, BorgWarner Inc., Aisin Seiki Co. Ltd., Continental AG, and Others. |

Key Segment |

By Motor Type, By Vehicle Type, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Segmentation Analysis

The EV Traction Motor market is segmented by motor type, vehicle type, and region.

Based on Motor Type Segment, the EV Traction Motor market is divided into permanent magnet synchronous motor, AC induction motor, brushless DC motor, and others. Permanent magnet synchronous motor emerges as the most dominant subsegment, holding approximately 60% market share, followed by AC induction motor as the second most dominant with around 25%. Permanent magnet synchronous motor's dominance arises from its superior energy efficiency, high torque at low speeds, and compact size, which are crucial for extending EV range and improving acceleration; this drives the market by enabling manufacturers to meet consumer demands for better performance while complying with efficiency regulations, thus accelerating overall EV adoption. AC induction motor, valued for its robustness and lower cost without rare-earth materials, supports market growth in cost-sensitive segments like commercial vehicles, where durability under continuous operation helps expand electrification in logistics and public transport.

Based on Vehicle Type Segment, the EV Traction Motor market is divided into battery electric vehicles, plug-in hybrid electric vehicles, hybrid electric vehicles, and others. Battery electric vehicles is the most dominant subsegment with about 78% share, while plug-in hybrid electric vehicles is the second most dominant at roughly 15%. Battery electric vehicles dominate due to their zero-emission profile, simpler drivetrain, and alignment with global sustainability goals, making them ideal for urban mobility; this subsegment propels the market through high-volume production spurred by incentives and infrastructure development, fostering economies of scale in motor manufacturing. Plug-in hybrid electric vehicles gain traction for offering extended range without full reliance on charging, aiding market expansion by bridging the gap for consumers in regions with limited infrastructure, thus broadening EV accessibility.

Recent Developments

- In October 2024, Nidec Motor Corporation and Ashok Leyland announced a partnership to accelerate commercial vehicle electrification in India, involving the supply of Nidec's E-Drive motor-controller systems for Ashok Leyland's vehicles.

- In December 2024, Toyota introduced the Toyota Urban Cruiser EV, featuring advanced traction motors for improved efficiency, set for launch in mid-2025.

- In December 2024, JSW MG Motor launched the electric sports car Cyberster in India, equipped with high-performance traction motors for enhanced driving dynamics.

- In May 2025, ABB launched the AMXE250 motor and HES580 inverter package, reducing motor losses by up to 12% for better performance in electric buses.

- In July 2024, Parker Hannifin extended its GVM310 motor range to 351 kW, offering higher power density for on- and off-road EVs.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific commands the largest share in the global EV traction motor market, propelled by massive investments in EV production and supportive government policies. China, as the dominating country, leads with its extensive supply chain, subsidies for EV purchases, and dominance in battery manufacturing, enabling cost-effective motor production and export. The region's rapid urbanization and focus on reducing air pollution further drive demand, while India's growing EV incentives and manufacturing hubs like those in Tamil Nadu contribute to diversified growth.

North America demonstrates robust expansion, driven by technological innovation and federal incentives like the Inflation Reduction Act. The United States dominates this region, with major players like Tesla advancing in-house motor development and benefiting from reshoring initiatives. Canada's mineral resources for motor components and Mexico's automotive assembly strengths enhance regional synergy, supporting growth in premium EVs and commercial electrification.

Europe maintains a strong position through its commitment to carbon neutrality and advanced R&D in motor efficiency. Germany stands out as the dominating country, leveraging expertise from companies like Bosch and Volkswagen to pioneer integrated e-drive systems. The UK's focus on post-Brexit green tech and France's subsidies for domestic production bolster the market, amid challenges from energy transitions.

Latin America exhibits emerging potential, fueled by resource availability and urban mobility needs. Brazil dominates, with its ethanol heritage transitioning to hybrids and EVs, supported by investments in local assembly. Argentina's lithium reserves aid supply chains, while economic incentives in Chile promote fleet electrification, though infrastructure gaps remain a hurdle.

The Middle East & Africa region shows nascent growth, primarily from energy diversification efforts. South Africa leads as the dominating country, with automotive clusters adopting EV technologies for exports. UAE's Vision 2031 emphasizes sustainable transport, attracting investments in motor assembly, while oil-dependent economies gradually shift toward electrification to reduce import reliance.

Competitive Analysis

The global EV Traction Motor market is dominated by players:

- Tesla Inc.

- BYD Company Ltd.

- Bosch Mobility Solutions

- Siemens AG

- Nidec Motor Corporation

- ABB Ltd.

- Magna International Inc.

- Mitsubishi Electric Corporation

- ZF Friedrichshafen AG

- BorgWarner Inc.

- Aisin Seiki Co. Ltd.

- Continental AG

The global EV Traction Motor market is segmented as follows:

By Motor Type

- Permanent Magnet Synchronous Motor

- AC Induction Motor

- Brushless DC Motor

- Others

By Vehicle Type

- Battery Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Hybrid Electric Vehicles

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors