![]()

Search Market Research Report

Deep Grain Processing Market Size, Share Global Analysis Report, 2026-2034

Deep Grain Processing Market Size, Share, Growth Analysis Report By Product (Starch, Syrup, Oil, Gluten Meal, Bioethanol, and Others), By Application (Food & Beverage, Animal Feed, Biofuel, Pharmaceutical, Industrial, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

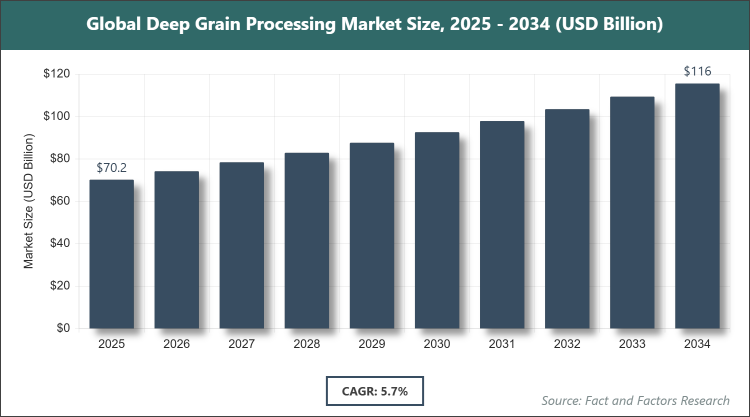

[235+ Pages Report] According to Facts & Factors, the global Deep Grain Processing market size was estimated at USD 70.2 billion in 2025 and is expected to reach USD 115.4 billion by the end of 2034. The Deep Grain Processing industry is anticipated to grow by a CAGR of 5.7% between 2026 and 2034. The Deep Grain Processing Market is driven by increasing demand for value-added grain products in food, feed, and biofuel sectors.

Market Overview

Market Overview

Deep Grain Processing involves the advanced conversion of grains like corn, wheat, barley, and sorghum into refined products through sophisticated techniques such as wet milling, dry milling, fermentation, and extraction. This process goes beyond basic grinding or cleaning, focusing on breaking down grains into components like starches, proteins, oils, and fibers to create high-value ingredients. It plays a crucial role in enhancing food quality, extending shelf life, and enabling the production of biofuels and industrial materials, serving as a bridge between agriculture and diverse end-use industries.

Key Insights

- As per the analysis shared by our research analyst, the global Deep Grain Processing market is estimated to grow annually at a CAGR of around 5.7% over the forecast period (2026-2034).

- In terms of revenue, the global Deep Grain Processing market size was valued at around USD 70.2 billion in 2025 and is projected to reach USD 115.4 billion, by 2034.

- The market is driven by rising consumption of processed foods, expanding biofuel production, and growing industrial applications of grain derivatives.

- Based on the Product, Starch is the dominating subsegment with a 40% share, as it serves as a versatile thickener, stabilizer, and binder in food and non-food applications.

- Based on the Application, Food & Beverage is the dominating subsegment with a 45% share, driven by the widespread use of processed grain ingredients in convenience foods, beverages, and bakery products.

- Based on the region, Asia Pacific holds the largest share at 38%, owing to high grain production volumes in countries like China and India, coupled with rapid industrialization and urbanization boosting demand.

Growth Drivers

- Increasing Demand for Processed and Convenience Foods

The surge in urban lifestyles and busy schedules has heightened the need for ready-to-eat and processed foods, which rely heavily on deep-processed grain ingredients like starches and syrups for texture and sweetness. This trend is particularly evident in emerging economies where rising disposable incomes enable consumers to opt for premium food products.

Furthermore, advancements in food technology have allowed for the development of innovative products such as gluten-free alternatives and fortified foods, further propelling the market. Government initiatives promoting food security and nutritional enhancement also contribute to this driver by encouraging investments in processing infrastructure.

Restraints

- Volatility in Raw Material Prices

Fluctuations in grain prices due to weather uncertainties, trade policies, and supply chain disruptions pose significant challenges, increasing production costs and affecting profitability for processors. This volatility can lead to inconsistent supply and pricing for end-products, deterring long-term investments.

Additionally, dependency on specific grains like corn makes the market vulnerable to regional crop failures or global commodity market shifts, compelling companies to seek alternative sourcing strategies or hedging mechanisms to mitigate risks.

Opportunities

- Expansion in Biofuel and Renewable Energy Sectors

The global push towards sustainable energy sources has amplified the use of bioethanol derived from deep-processed grains, creating new revenue streams amid rising environmental regulations and incentives for green fuels. This opportunity is bolstered by technological improvements in fermentation processes that enhance yield and efficiency.

Moreover, partnerships between agricultural and energy sectors are fostering innovation in biofuel production, with potential for market expansion in regions investing in renewable energy infrastructure to reduce carbon footprints and achieve energy independence.

Challenges

- Stringent Regulatory and Environmental Standards

Compliance with food safety regulations and environmental norms requires substantial investments in quality control and waste management, which can be burdensome for smaller players in the market. These standards vary across regions, complicating international trade and operations.

In addition, concerns over water usage and emissions in processing plants necessitate the adoption of eco-friendly technologies, which may increase operational costs and require skilled labor, posing hurdles to market entry and expansion.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 70.2 Billion |

Projected Market Size in 2034 |

USD 115.4 Billion |

CAGR Growth Rate |

5.7% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Cargill, Incorporated, Archer Daniels Midland Company (ADM), Ingredion Incorporated, Tate & Lyle PLC, Bunge Limited, Grain Processing Corporation, Roquette Frères, Louis Dreyfus Company, The Andersons, Inc., AGRANA Beteiligungs-AG, and Others. |

Key Segment |

By Product, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Deep Grain Processing market is segmented by Product, Application, and region.

Based on Product Segment, the Deep Grain Processing market is divided into Starch, Syrup, Oil, Gluten Meal, Bioethanol, and Others. The most dominant segment is Starch, holding a significant market share due to its extensive applications in food thickening, paper manufacturing, and adhesives. The second most dominant is Bioethanol, which drives the market through its role in sustainable fuel production, supported by government policies on renewable energy. Starch's dominance stems from its cost-effectiveness and multifunctionality, enabling widespread adoption across industries, while Bioethanol contributes to market growth by addressing energy demands and reducing reliance on fossil fuels.

Based on Application Segment, the Deep Grain Processing market is divided into Food & Beverage, Animal Feed, Biofuel, Pharmaceutical, Industrial, and Others. The most dominant segment is Food & Beverage, capturing the largest share owing to the essential use of grain derivatives in enhancing flavor, texture, and shelf life of products. The second most dominant is Biofuel, which propels market expansion through increasing demand for eco-friendly alternatives to petroleum. Food & Beverage leads because of rising consumer preferences for processed foods, while Biofuel's growth is fueled by global efforts to combat climate change and promote sustainable practices.

Recent Developments

- In 2025, Cargill announced a major expansion of its corn processing facility in the U.S., investing USD 200 million to enhance starch and sweetener production capacity, aiming to meet growing demand in the food sector.

- Archer Daniels Midland Company (ADM) partnered with a biotech firm in early 2026 to develop advanced fermentation technologies for bioethanol, focusing on improving yield and reducing environmental impact.

- Ingredion launched a new line of sustainable grain-based ingredients in 2025, derived from non-GMO corn, targeting the clean-label trend in food and beverages.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific is poised to lead the Deep Grain Processing market, driven by robust agricultural output and rapid industrialization. China stands out as the dominating country, with its massive corn production and government support for value-added processing industries. The region's growth is fueled by increasing urbanization, which boosts demand for processed foods and biofuels, alongside investments in modern processing technologies to enhance efficiency and product quality.

North America follows closely, with the United States as the key player due to its advanced processing infrastructure and strong biofuel sector. The emphasis on innovation and sustainability, coupled with favorable policies for ethanol production, supports steady market expansion. Europe focuses on regulatory compliance and eco-friendly practices, with Germany leading in pharmaceutical and industrial applications of processed grains. Latin America benefits from abundant grain resources, particularly in Brazil, where biofuel initiatives drive growth. The Middle East & Africa region is emerging, with South Africa pioneering in animal feed processing amid efforts to improve food security.

Competitive Analysis

The global Deep Grain Processing market is dominated by players:

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Bunge Limited

- Grain Processing Corporation

- Roquette Frères

- Louis Dreyfus Company

- The Andersons, Inc.

- AGRANA Beteiligungs-AG

The global Deep Grain Processing market is segmented as follows:

By Product

- Starch

- Syrup

- Oil

- Gluten Meal

- Bioethanol

- Others

By Application

- Food & Beverage

- Animal Feed

- Biofuel

- Pharmaceutical

- Industrial

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global Deep Grain Processing market is dominated by players:

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Bunge Limited

- Grain Processing Corporation

- Roquette Frères

- Louis Dreyfus Company

- The Andersons, Inc.

- AGRANA Beteiligungs-AG

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors