![]()

Search Market Research Report

Cling Film Market Size, Share Global Analysis Report, 2026-2034

Cling Film Market Size, Share, Growth Analysis Report By Material (Polyethylene, Polyvinyl Chloride, Polyvinylidene Chloride, Biaxially Oriented Polypropylene, and Others), By Form (Cast Cling Film, Blow Cling Film), By Thickness (Up to 10 Microns, 10-15 Microns, 15-20 Microns, Above 20 Microns), By End-User (Food, Healthcare, Consumer Goods, Industrial, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

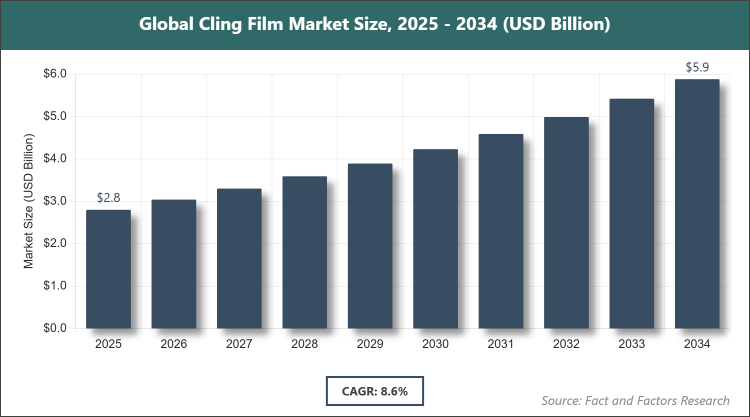

[224+ Pages Report] According to Facts & Factors, the global Cling Film market size was estimated at USD 2.8 billion in 2025 and is expected to reach USD 6.0 billion by the end of 2034. The Cling Film industry is anticipated to grow by a CAGR of 8.6% between 2026 and 2034. The Cling Film Market is driven by increasing demand in the food packaging and e-commerce sectors.

Market Overview

Market Overview

The cling film market encompasses the production, distribution, and utilization of thin plastic films designed to adhere to surfaces without adhesives, primarily used for wrapping and preserving food items to maintain freshness and prevent contamination. These films, often made from materials like polyethylene or PVC, offer flexibility, transparency, and moisture resistance, serving essential roles in household, commercial, and industrial packaging. The market focuses on innovations in biodegradable and recyclable variants to address environmental concerns, while ensuring compliance with food safety standards and enhancing usability through features like easy dispensing and anti-fog properties.

Key Insights

- As per the analysis shared by our research analyst, the global Cling Film market is estimated to grow annually at a CAGR of around 8.6% over the forecast period (2026-2034).

- In terms of revenue, the global Cling Film market size was valued at around USD 2.8 billion in 2025 and is projected to reach USD 6.0 billion, by 2034.

- The Cling Film market is projected to witness significant growth due to rising food preservation needs and expanding retail sectors.

- Based on the Material, the Polyvinyl Chloride segment accounted for the largest market share of 52% due to its superior cling properties and cost-effectiveness in food wrapping.

- Based on the Form, the Cast Cling Film segment dominated the market with the highest share owing to its high clarity and strength for commercial applications.

- Based on the Thickness, the 10-15 Microns segment held the leading position with a substantial share because of its optimal balance of durability and flexibility for everyday use.

- Based on the End-User, the Food segment accounted for the largest market share of 71% due to increasing demand for hygienic packaging in supermarkets and households.

- Based on the region, the Asia Pacific region captured around 40% market share, driven by rapid urbanization and growth in food processing industries.

Growth Drivers

- Increasing Demand in Food Packaging

The surge in ready-to-eat meals and fresh produce consumption is boosting cling film usage for extending shelf life and maintaining hygiene, particularly in supermarkets and e-commerce deliveries. Global urbanization and busy lifestyles amplify this trend, as consumers seek convenient preservation solutions. Innovations in antimicrobial films further enhance appeal by reducing bacterial growth.

Additionally, regulatory emphasis on food safety standards encourages adoption of high-quality films, fostering partnerships between manufacturers and retailers. This driver expands market reach into emerging economies, where rising disposable incomes support premium packaging demands.

Restraints

- Environmental Concerns and Regulations

Growing awareness of plastic pollution leads to bans on single-use plastics, increasing pressure to shift from traditional PVC films to costlier alternatives. This transition raises production expenses and disrupts supply chains. Consumer preference for eco-friendly options challenges market players.

Moreover, stringent recycling mandates in regions like Europe complicate compliance, potentially limiting exports. These restraints slow growth in mature markets, necessitating investments in sustainable R&D to mitigate impacts.

Opportunities

- Development of Biodegradable Films

Advancements in bio-based materials offer eco-friendly alternatives, attracting environmentally conscious consumers and aligning with global sustainability goals. Government incentives for green packaging accelerate innovation. This trend opens new segments in organic food wrapping.

Furthermore, collaborations with biotech firms enable scalable production, reducing costs over time. This opportunity positions the market for expansion in regulated areas, enhancing brand loyalty through green credentials.

Challenges

- Raw Material Price Volatility

Fluctuations in petroleum-based resin prices affect manufacturing costs, leading to unstable pricing for end-users. Supply disruptions from geopolitical issues exacerbate this. Alternative materials remain expensive at scale.

In addition, competition from reusable containers threatens demand. These challenges require diversified sourcing and hedging strategies to maintain profitability.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.8 Billion |

Projected Market Size in 2034 |

USD 6.0 Billion |

CAGR Growth Rate |

8.6% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Berry Global Inc., Amcor plc, Reynolds Consumer Products, Glad Products Company, Sealed Air Corporation, Anchor Packaging, Mitsubishi Chemical Corporation, Harwal Group, Wrapex Ltd., 3M, CeDo Ltd., Intertape Polymer Group, and Others. |

Key Segment |

By Material, By Form, By Thickness, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Cling Film market is segmented by material, form, thickness, end-user, and region.

Based on Material Segment, the Cling Film market is divided into Polyethylene, Polyvinyl Chloride, Polyvinylidene Chloride, Biaxially Oriented Polypropylene, and others. The most dominant segment is Polyvinyl Chloride, which holds the largest share due to its excellent adhesion and affordability for food applications, driving the market by enabling widespread use in retail packaging; the second most dominant is Polyethylene, favored for its recyclability and strength, contributing to market growth through sustainable options in industrial wrapping.

Based on Form Segment, the Cling Film market is divided into Cast Cling Film, Blow Cling Film. The most dominant segment is Cast Cling Film, commanding the highest share because of its superior clarity and quiet unwind for consumer use, which drives the market by improving user experience in households; the second most dominant is Blow Cling Film, used for its puncture resistance in heavy-duty applications, propelling market expansion via industrial demands.

Based on Thickness Segment, the Cling Film market is divided into Up to 10 Microns, 10-15 Microns, 15-20 Microns, Above 20 Microns, and others. The most dominant segment is 10-15 Microns, holding the biggest share due to its versatility for standard wrapping needs, driving the market by balancing cost and performance in food service; the second most dominant is Above 20 Microns, preferred for durable industrial uses, contributing to market growth amid heavy packaging requirements.

Based on End-User Segment, the Cling Film market is divided into Food, Healthcare, Consumer Goods, Industrial, and others. The most dominant segment is Food, with the largest share attributed to rising demand for fresh preservation in retail, driving the market by supporting global food supply chains; the second most dominant is Industrial, utilized for protective wrapping, helping drive the market through manufacturing efficiencies.

Recent Developments

- In April 2024, Berry Global released Omni Xtra+ polyethylene cling film as a recyclable alternative to PVC for fresh food packaging.

- In November 2023, Berry Global developed a new version of polyethylene cling film for fresh food applications.

- In February 2025, IPG launched Plastic Sheeting brand with Ultra and Performance film varieties.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the cling film market, with China dominating through its vast manufacturing base and export-oriented food processing industry that drives high-volume production of affordable films. Rapid urbanization increases supermarket penetration, boosting demand for convenient wrapping solutions. Government initiatives on food safety enhance adoption of quality films. China's leadership comes from integrated supply chains and low production costs.

North America demonstrates solid performance with advanced retail systems, led by the United States as the dominant country via innovative sustainable films and strong e-commerce growth. Regulatory focus on recyclability spurs bio-based developments. The U.S. excels through consumer demand for premium products and efficient distribution networks.

Europe emphasizes eco-friendly innovations, with Germany as the dominant country leveraging its engineering expertise in high-barrier films for food exports. EU regulations on plastics promote biodegradable options. Germany's position strengthens from export markets and sustainability commitments.

Latin America grows with expanding retail, led by Brazil through food industry expansions and urban consumer shifts. Investments in packaging infrastructure support demand. Brazil's dominance arises from natural resources and regional trade.

The Middle East & Africa advances via oil-based economies, with Saudi Arabia dominating through diversification into packaging manufacturing. Growing food imports enhance film usage. Saudi Arabia's lead stems from strategic investments and partnerships.

Competitive Analysis

The global Cling Film market is dominated by players:

- Berry Global Inc.

- Amcor plc

- Reynolds Consumer Products

- Glad Products Company

- Sealed Air Corporation

- Anchor Packaging

- Mitsubishi Chemical Corporation

- Harwal Group

- Wrapex Ltd.

- 3M

- CeDo Ltd.

- Intertape Polymer Group

The global Cling Film market is segmented as follows:

By Material

- Polyethylene

- Polyvinyl Chloride

- Polyvinylidene Chloride

- Biaxially Oriented Polypropylene

- Others

By Form

- Cast Cling Film

- Blow Cling Film

By Thickness

- Up to 10 Microns

- 10-15 Microns

- 15-20 Microns

- Above 20 Microns

- Others

By End-User

- Food

- Healthcare

- Consumer Goods

- Industrial

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Berry Global Inc.

- Amcor plc

- Reynolds Consumer Products

- Glad Products Company

- Sealed Air Corporation

- Anchor Packaging

- Mitsubishi Chemical Corporation

- Harwal Group

- Wrapex Ltd.

- 3M

- CeDo Ltd.

- Intertape Polymer Group

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors