![]()

Search Market Research Report

Bulk Container Packaging Market Size, Share Global Analysis Report, 2026-2034

Bulk Container Packaging Market Size, Share, Growth Analysis Report By Product Type (Flexible Intermediate Bulk Containers (FIBCs), Rigid Intermediate Bulk Containers (RIBCs), Flexitanks, Drums, Pails, and Others), By Application (Storage, Transportation, and Others), By End-User (Chemicals, Food & Beverages, Pharmaceuticals, Petroleum & Lubricants, Paints & Dyes, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

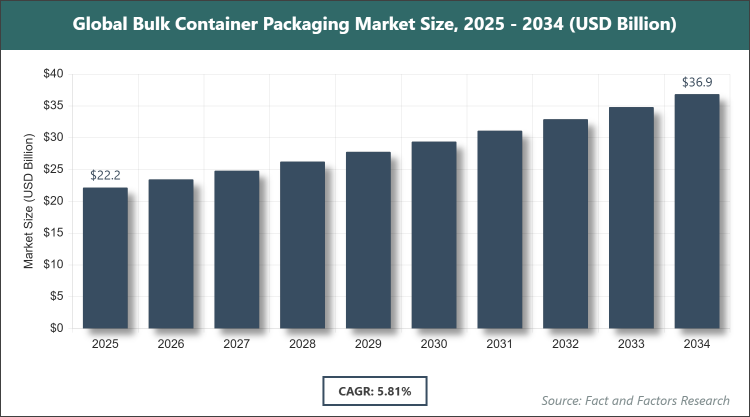

[235+ Pages Report] According to Facts & Factors, the global bulk container packaging market size was estimated at USD 22.17 billion in 2025 and is expected to reach USD 36.85 billion by the end of 2034. The bulk container packaging industry is anticipated to grow by a CAGR of 5.81% between 2026 and 2034. The bulk container packaging Market is driven by increasing demand from end-use industries such as chemicals and food & beverages.

Market Overview

Market Overview

Bulk container packaging refers to the systems and solutions designed for the storage, transportation, and handling of large volumes of materials, typically in industrial settings. It encompasses a variety of containers that ensure safe, efficient, and cost-effective movement of bulk goods, protecting them from contamination, damage, and environmental factors while optimizing logistics and supply chain operations.

Key Insights

-

As per the analysis shared by our research analyst, the global bulk container packaging market is expected to grow annually at a CAGR of around 5.81% during the forecast period 2026-2034.

- In terms of revenue, the global bulk container packaging market size was valued at around USD 22.17 billion in 2025 and is projected to reach USD 36.85 billion by 2034.

- The market is driven by rising global trade, industrialization, and demand for sustainable packaging solutions.

- Based on the product type, the Flexible Intermediate Bulk Containers (FIBCs) segment dominated the market with a share of 61% due to their lightweight, cost-effective nature, and versatility in handling dry bulk materials across various industries.

- Based on the application, the transportation segment dominated with a share of 65% as it facilitates efficient logistics and supply chain management for bulk goods.

- Based on the end-user, the chemicals segment dominated with a share of 38% owing to the need for safe and compliant packaging for hazardous materials.

- Asia Pacific dominated the global market with a share of 42% primarily due to rapid industrialization, expanding manufacturing sectors, and increasing exports in countries like China and India.

Growth Drivers

- Increasing Global Trade and Industrialization

The expansion of international trade and the growth of manufacturing sectors worldwide have significantly boosted the demand for bulk container packaging. As industries scale up production and distribution, the need for reliable, large-scale packaging solutions becomes essential to handle the volume of goods efficiently.

This trend is particularly evident in emerging economies where infrastructure development and export-oriented industries drive the adoption of advanced packaging systems. Furthermore, the integration of bulk containers in supply chains reduces handling costs and improves operational efficiency, making them indispensable for global commerce.

Restraints

- High Initial Costs and Maintenance Requirements

The substantial upfront investment required for high-quality bulk containers, along with ongoing maintenance to ensure compliance and safety, can deter smaller enterprises from adopting these solutions. This financial barrier limits market penetration in cost-sensitive regions and industries.

Additionally, the complexity of recycling or disposing of certain container materials adds to the overall cost, potentially slowing adoption rates among budget-constrained users.

Opportunities

- Advancements in Sustainable and Recyclable Materials

Innovations in eco-friendly materials and designs offer significant opportunities for market growth, as regulatory pressures and consumer preferences shift towards sustainability. Companies investing in biodegradable or recyclable bulk containers can capture a growing segment of environmentally conscious clients.

This shift not only aligns with global sustainability goals but also opens new revenue streams through premium pricing for green products and partnerships with eco-focused industries.

Challenges

- Stringent Regulatory Compliance and Safety Standards

Navigating diverse international regulations on packaging for hazardous materials poses a challenge, requiring continuous adaptation and investment in compliance measures. Failure to meet these standards can result in penalties and operational disruptions.

Moreover, varying regional requirements complicate global operations, demanding specialized knowledge and resources to maintain market access and competitiveness.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 22.17 Billion |

Projected Market Size in 2034 |

USD 36.85 Billion |

CAGR Growth Rate |

5.81% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Greif, Inc., Mauser Packaging Solutions, Schütz GmbH & Co. KGaA, Berry Global, Inc., Mondi Group, Sonoco Products Company, International Paper Company, Myers Industries, Inc., Novvia Group, Rapid Packaging Inc., and Others. |

Key Segment |

By Product Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The bulk container packaging market is segmented by product type, application, end-user, and region.

Based on Product Type Segment, the bulk container packaging market is divided into Flexible Intermediate Bulk Containers (FIBCs), Rigid Intermediate Bulk Containers (RIBCs), Flexitanks, Drums, Pails, and Others. The most dominant segment is Flexible Intermediate Bulk Containers (FIBCs), followed by Rigid Intermediate Bulk Containers (RIBCs). FIBCs dominate due to their flexibility, low cost, and high capacity for storing and transporting dry bulk goods like grains, powders, and chemicals, which drives market growth by enabling efficient handling and reducing transportation expenses. RIBCs, as the second dominant, offer durability for liquids and hazardous materials, contributing to market expansion through enhanced safety and reusability in demanding industrial applications.

Based on Application Segment, the bulk container packaging market is divided into Storage, Transportation, and Others. The most dominant segment is Transportation, followed by Storage. Transportation dominates because it supports global supply chains by providing secure and efficient movement of bulk materials, driving the market through optimized logistics and reduced spoilage risks. Storage, as the second dominant, aids in inventory management and protection of goods, fostering market growth by extending shelf life and minimizing warehouse space requirements.

Based on End-User Segment, the bulk container packaging market is divided into Chemicals, Food & Beverages, Pharmaceuticals, Petroleum & Lubricants, Paints & Dyes, and Others. The most dominant segment is Chemicals, followed by Food & Beverages. Chemicals dominate owing to the critical need for safe, compliant packaging to handle hazardous substances, propelling market growth via specialized designs that prevent leaks and contamination. Food & Beverages, as the second dominant, benefit from hygienic and protective packaging, boosting the market by ensuring product quality during transit and storage.

Recent Developments

- In February 2024, Rapid Packaging Inc. acquired Lawgix International to enhance its national supply chain for Flexible Intermediate Bulk Containers (FIBCs) and industrial bags, aiming to improve distribution efficiency and product offerings.

- In April 2023, Greif, Inc. acquired an 80% stake in Centurion Container LLC, a leader in reconditioning intermediate bulk containers and plastic drums in North America, for USD 145 million to expand its recycling and sustainability capabilities.

- In December 2023, Novvia Group acquired JWJ Packaging, a supplier of drums, pails, and other rigid container products, to strengthen its position in the rigid packaging distribution market.

- In December 2022, New Water Capital invested in the FIBC sector by acquiring Bulk Lift International LLC and Bagwell Supply Ltd., focusing on expanding production and market reach in flexible bulk packaging.

- In May 2022, Myers Industries expanded its production capacity by acquiring a Rotational Molding Facility in Georgia to meet growing demand for bulk containers.

- In 2022, Greif acquired Lee Container for USD 300 million to integrate operations and achieve efficiency gains of at least USD 6 million over two years.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region holds the largest share in the bulk container packaging market, driven by its robust manufacturing base and export activities. Countries like China and India lead due to their extensive chemical and food processing industries, which rely heavily on efficient bulk handling solutions. The region's strategic location facilitates global trade, further amplifying demand for durable packaging.

North America follows closely, with strong growth in pharmaceuticals and chemicals sectors. The United States dominates here, benefiting from advanced logistics infrastructure and stringent safety regulations that promote high-quality container adoption. Innovation in sustainable materials also supports market expansion in this region.

Europe emphasizes sustainability, with Germany and the UK leading through investments in recyclable packaging. The focus on environmental compliance and efficient supply chains in food and beverage industries drives steady growth, positioning Europe as a key player in premium bulk solutions.

Latin America shows potential through agricultural exports, with Brazil dominating via demand for food-grade containers. Infrastructure improvements and increasing industrialization contribute to gradual market development, though economic volatility poses some challenges.

The Middle East & Africa region grows through oil and chemical exports, with Saudi Arabia and South Africa leading. Investments in petrochemicals and mining sectors boost the need for specialized bulk packaging, supported by improving trade networks.

Competitive Analysis

The global bulk container packaging market is dominated by players:

- Greif, Inc.

- Mauser Packaging Solutions

- Schütz GmbH & Co. KGaA

- Berry Global, Inc.

- Mondi Group

- Sonoco Products Company

- International Paper Company

- Myers Industries, Inc.

- Novvia Group

- Rapid Packaging Inc.

- And Others

The global bulk container packaging market is segmented as follows:

By Product Type

- Flexible Intermediate Bulk Containers (FIBCs)

- Rigid Intermediate Bulk Containers (RIBCs)

- Flexitanks

- Drums

- Pails

- Others

By Application

- Storage

- Transportation

- Others

By End-User

- Chemicals

- Food & Beverages

- Pharmaceuticals

- Petroleum & Lubricants

- Paints & Dyes

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global bulk container packaging market is dominated by players:

- Greif, Inc.

- Mauser Packaging Solutions

- Schütz GmbH & Co. KGaA

- Berry Global, Inc.

- Mondi Group

- Sonoco Products Company

- International Paper Company

- Myers Industries, Inc.

- Novvia Group

- Rapid Packaging Inc.

- And Others

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors