![]()

Search Market Research Report

Beer Market Size, Share Global Analysis Report, 2026-2034

Beer Market Size, Share, Growth Analysis Report By Type (Lager, Ale, Stout & Porter, Malt, and Others), By Packaging (Glass, PET Bottle, Metal Can, and Others), By Production (Macro-brewery, Micro-brewery, Craft Brewery, and Others), By Distribution Channel (On-Trade, Off-Trade), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

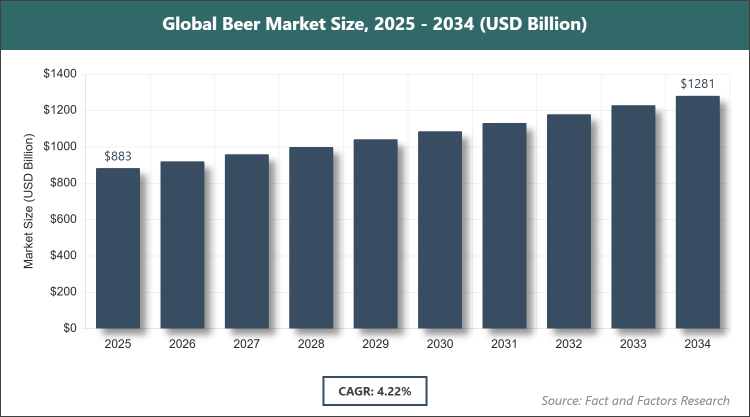

[235+ Pages Report] According to Facts & Factors, the global beer market size was estimated at USD 882.80 billion in 2025 and is expected to reach USD 1275.52 billion by the end of 2034. The Beer industry is anticipated to grow by a CAGR of 4.22% between 2026 and 2034. The Beer Market is driven by increasing demand for premium and craft beers amid rising disposable incomes.

Market Overview

Market Overview

The beer market encompasses the production, distribution, and consumption of beer, an alcoholic beverage brewed primarily from malted barley, hops, water, and yeast through fermentation processes that yield a variety of styles ranging from light lagers to robust ales, serving both social and recreational purposes while also incorporating non-alcoholic variants to cater to health-conscious consumers and diverse cultural preferences across global regions. This market involves a spectrum of stakeholders from large-scale breweries to craft producers, focusing on innovation in flavors, packaging, and sustainability to meet evolving demands in both on-trade and off-trade channels.

Key Insights

- As per the analysis shared by our research analyst, the Beer market is expected to grow at a CAGR of 4.22% during the forecast period of 2026-2034.

- In terms of revenue, the Beer market size was valued at about USD 882.80 billion in 2025 and is expected to reach USD 1275.52 billion by 2034.

- The Beer market is driven by increasing demand for premium and craft beers amid rising disposable incomes.

- Based on the type, the Lager segment dominated the market with a share of 87.09% in 2025 due to its mass-market appeal, crisp taste, and widespread availability in both emerging and mature markets.

- Based on the packaging, the Glass segment dominated the market with a share of 74.64% in 2025, owing to its premium perception, recyclability, and traditional association with quality beer consumption.

- Based on the production, the Macro-brewery segment dominated the market with a share of 67.2% in 2025 because of large-scale efficiency, global distribution networks, and the ability to produce consistent volumes at lower costs.

- Based on the distribution channel, the Off-Trade segment dominated the market with a share of 55% in 2025 as it offers convenience through retail channels like supermarkets and online sales, catering to at-home consumption trends.

- Asia Pacific dominated the market with a share of 30.12% in 2025 due to rapid urbanization, expanding middle-class populations, and high consumption volumes in countries like China and India.

Growth Drivers

- Rising Demand for Premium and Craft Beers

The increasing consumer preference for premium and craft beers, driven by a desire for unique flavors and higher-quality ingredients, is significantly boosting market growth, as millennials and urban professionals seek artisanal experiences over mass-produced options, supported by the proliferation of craft breweries worldwide. This trend is further enhanced by social media influence and experiential marketing that highlight storytelling and innovation in brewing.

Additionally, investments in R&D for new styles, such as flavored and low-alcohol variants, are attracting health-conscious consumers, expanding the market beyond traditional demographics and fostering loyalty through limited-edition releases and collaborations.

- Expanding E-Commerce and Delivery Platforms

The growth of online alcohol sales and on-demand delivery services is facilitating easier access to diverse beer options, particularly in urban areas, driving convenience-led consumption and enabling smaller brands to reach wider audiences without heavy reliance on physical retail. This driver is amplified by partnerships with platforms like Uber Eats and Drizly, which offer promotions and subscriptions.

Moreover, digital marketing and data analytics allow brewers to personalize recommendations, enhancing customer engagement and repeat purchases, while navigating regulatory changes to expand e-commerce presence in emerging markets.

- Increasing Social Acceptance of Moderate Drinking

Shifting cultural norms towards responsible alcohol consumption are promoting beer as a social beverage, especially in emerging economies, where rising disposable incomes enable more frequent gatherings and celebrations incorporating beer. This is supported by campaigns emphasizing moderation and low-ABV options.

Furthermore, tourism and events like beer festivals are creating experiential opportunities, boosting demand through immersive activities that educate consumers on beer varieties and pair them with food, sustaining long-term interest.

Restraints

- Stringent Government Regulations

Strict advertising restrictions and taxation policies in various regions limit marketing strategies and increase operational costs, hindering market penetration, particularly for new entrants in highly regulated areas like Europe and North America. This restraint is compounded by age verification requirements in online sales.

Ongoing policy changes, such as higher excise duties, further strain profitability, requiring brewers to adapt pricing models and explore alternative markets to offset impacts.

- Health Concerns and Moderation Trends

Rising awareness of alcohol-related health risks is leading to reduced consumption among younger generations, who prefer non-alcoholic alternatives, impacting traditional beer sales volumes. This is influenced by wellness movements and sober-curious lifestyles.

Brewers must innovate with healthier options like low-calorie beers to retain market share, though this involves R&D costs and potential cannibalization of core products.

Opportunities

- Growth in Non-Alcoholic Beer Segment

The expanding demand for non-alcoholic beers presents opportunities to capture health-focused consumers, with innovations in taste mimicking traditional beers to appeal to a broader audience. This aligns with global wellness trends.

Strategic marketing as inclusive options for social settings can drive adoption, supported by retail expansions and collaborations with fitness brands.

- Sustainability Initiatives

Adopting eco-friendly practices, such as recyclable packaging and renewable energy in brewing, can attract environmentally conscious consumers, enhancing brand loyalty. This opportunity is ripe for differentiation in competitive markets.

Investments in sustainable sourcing can reduce costs long-term and meet regulatory demands for green operations.

Challenges

- Raw Material Price Volatility

Fluctuations in prices of key ingredients like barley and hops due to climate impacts and supply chain disruptions pose challenges to cost management and profitability. This requires hedging strategies.

Global trade issues further exacerbate availability, demanding diversified sourcing to maintain production stability.

- Intense Competition from Alternatives

The rise of ready-to-drink cocktails and hard seltzers is diverting consumer spending from beer, particularly among younger demographics seeking variety. This challenge necessitates product diversification.

Brewers must innovate to reclaim share, though rapid trend shifts increase R&D demands and market risks.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 882.80 Billion |

Projected Market Size in 2034 |

USD 1275.52 Billion |

CAGR Growth Rate |

4.22% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Anheuser-Busch InBev, Heineken N.V., Carlsberg Group, Molson Coors Beverage Company, Asahi Group Holdings Ltd., China Resources Snow Breweries, Tsingtao Brewery Group, Beijing Yanjing Beer Group Corporation, Kirin Holdings Company Limited, Constellation Brands Inc., Diageo plc, Boston Beer Company Inc., Sierra Nevada Brewing Co., New Belgium Brewing Company, BrewDog plc, and Others. |

Key Segment |

By Type, By Packaging, By Production, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Beer market is segmented by type, packaging, production, distribution channel, and region.

Based on Type Segment, the beer market is divided into Lager, Ale, Stout & Porter, Malt, and others. The most dominant segment is Lager, holding the largest share due to its refreshing taste, broad appeal across diverse demographics, and suitability for mass production, which drives market growth by ensuring high-volume sales in both developed and emerging economies; the second most dominant is Ale, gaining traction for its complex flavors and craft variations that attract premium-seeking consumers, contributing to market expansion through innovation and higher pricing margins.

Based on Packaging Segment, the beer market is divided into Glass, PET Bottle, Metal Can, and others. The most dominant segment is Glass, leading the market because of its premium image, excellent preservation of flavor, and recyclability, propelling growth via consumer preference for traditional packaging in social settings; the second most dominant is Metal Can, favored for its portability, durability, and eco-friendly recycling, aiding market drive by enabling convenient consumption in outdoor and on-the-go scenarios.

Based on Production Segment, the beer market is divided into Macro-brewery, Micro-brewery, Craft Brewery, and others. The most dominant segment is Macro-brewery, commanding the top position owing to economies of scale, global branding, and extensive distribution, boosting overall market growth through consistent supply and affordability; the second most dominant is Craft Brewery, which supports expansion by offering unique, localized products that cater to niche tastes and premium trends.

Based on Distribution Channel Segment, the beer market is divided into On-Trade and Off-Trade. The most dominant segment is Off-Trade, dominating due to convenience in retail purchases like supermarkets and online platforms, driving growth through at-home consumption and bulk buying; the second most dominant is On-Trade, enhancing market reach via bars and restaurants where social experiences encourage higher spending.

Recent Developments

- In April 2023, Heineken launched Heineken Silver with low-carb, low-calorie labels in the U.S. market to cater to health-conscious consumers.

- In November 2022, Kenya Breweries Limited introduced Rockshire Tropical Lager, infused with tropical fruit flavors like pineapple and passion fruit.

- In April 2022, BIRA 91 released the Imagined in India series, including four limited-edition beers such as Kokum Sour and Mango Lassi.

- In March 2023, BIRA 91 launched two limited-edition beers, 022 Session Ale and 011 Gully Pilsner, tied to cricket teams.

- In January 2023, Anheuser-Busch introduced Michelob ULTRA Zero, an alcohol-free beer option.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the beer market with China as the dominating country, where massive population growth and urbanization fuel high consumption volumes through affordable local brands and expanding retail networks, while cultural shifts towards social drinking in urban settings like bars and events drive demand, supported by government policies promoting domestic production and foreign investments that enhance brewing technology and variety to meet diverse tastes across regions.

North America follows, dominated by the United States, which benefits from a strong craft beer culture and premium imports integrated into social lifestyles, with robust on-trade channels in bars and restaurants complemented by e-commerce growth, while health trends boost low-ABV options, backed by advanced marketing and festivals that engage consumers in experiential drinking.

Europe maintains prominence, led by Germany, where deep-rooted beer traditions and festivals like Oktoberfest sustain high per-capita consumption, with emphasis on quality lagers and ales through regulated brewing standards, alongside increasing exports and innovations in sustainable packaging that align with eco-conscious preferences across the continent.

Latin America exhibits growth potential, with Brazil as the key country, driven by tropical climates favoring light beers in social gatherings, supported by large-scale production and affordable pricing, while rising tourism and urban expansion increase on-trade demand in vibrant nightlife scenes.

The Middle East & Africa region is emerging, dominated by South Africa, where growing middle-class incomes support premium beer adoption, with local breweries adapting to diverse climates through resilient supply chains, aided by international partnerships that introduce global brands and boost consumption in urban hubs.

Competitive Analysis

The global Beer market is dominated by players:

- Anheuser-Busch InBev

- Heineken N.V.

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings Ltd.

- China Resources Snow Breweries

- Tsingtao Brewery Group

- Beijing Yanjing Beer Group Corporation

- Kirin Holdings Company Limited

- Constellation Brands Inc.

- Diageo plc

- Boston Beer Company Inc.

- Sierra Nevada Brewing Co.

- New Belgium Brewing Company

- BrewDog plc

The global Beer market is segmented as follows:

By Type

- Lager

- Ale

- Stout & Porter

- Malt

- Others

By Packaging

- Glass

- PET Bottle

- Metal Can

- Others

By Production

- Macro-brewery

- Micro-brewery

- Craft Brewery

- Others

By Distribution Channel

- On-Trade

- Off-Trade

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global Beer market is dominated by players:

Anheuser-Busch InBev

Heineken N.V.

Carlsberg Group

Molson Coors Beverage Company

Asahi Group Holdings Ltd.

China Resources Snow Breweries

Tsingtao Brewery Group

Beijing Yanjing Beer Group Corporation

Kirin Holdings Company Limited

Constellation Brands Inc.

Diageo plc

Boston Beer Company Inc.

Sierra Nevada Brewing Co.

New Belgium Brewing Company

BrewDog plc

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors