![]()

Search Market Research Report

Aerospace and Defense Market Size, Share Global Analysis Report, 2026-2034

Aerospace and Defense Market Size, Share, Growth Analysis Report By Type (Air-based, Land-based, Sea-based, Space-based, and Others), By Application (Aviation, Military Operations, Maritime, Space Exploration, and Others), By End-User (Government & Military, Commercial Airlines, Space Agencies, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

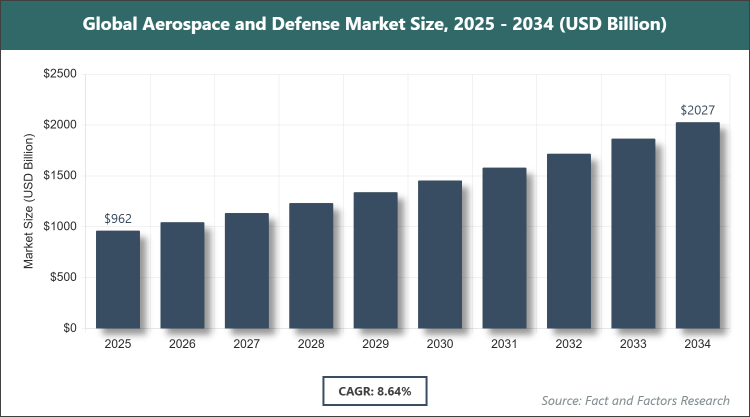

[242+ Pages Report] According to Facts & Factors, the global Aerospace and Defense market size was estimated at USD 961.7 billion in 2025 and is expected to reach USD 2027.39 billion by the end of 2034. The Aerospace and Defense industry is anticipated to grow by a CAGR of 8.64% between 2026 and 2034. The Aerospace and Defense Market is driven by rising geopolitical tensions and increasing demand for advanced military and commercial aircraft.

Market Overview

Market Overview

The aerospace and defense market comprises the design, manufacturing, and maintenance of aircraft, spacecraft, and related systems for both civilian and military purposes, encompassing advanced technologies for aviation, space exploration, and national security. This market integrates engineering innovations in aerodynamics, propulsion, and materials to create efficient, reliable platforms that support global transportation, satellite communications, and defense strategies. It involves a complex supply chain of components, software, and services, addressing needs from commercial air travel to strategic military operations, while emphasizing safety, sustainability, and technological superiority in a highly regulated environment.

Key Insights

- As per the analysis shared by our research analyst, the global Aerospace and Defense market is estimated to grow annually at a CAGR of around 8.64% over the forecast period (2026-2034).

- In terms of revenue, the global Aerospace and Defense market size was valued at around USD 961.7 billion in 2025 and is projected to reach USD 2027.39 billion, by 2034.

- The Aerospace and Defense market is projected to witness significant growth due to increasing global air travel demand and rising defense budgets amid geopolitical tensions.

- Based on the Type, the Air-based segment accounted for the largest market share of 34% due to high demand for commercial and military aircraft.

- Based on the Application, the Aviation segment dominated the market with the highest share owing to surging passenger traffic and fleet modernization efforts.

- Based on the End-User, the government and military segment held the leading position with a substantial share because of elevated defense spending and national security priorities.

- Based on the region, the North America region captured around 40% market share, driven by the presence of major industry players and substantial defense investments.

Growth Drivers

- Rising Geopolitical Tensions

Escalating conflicts and territorial disputes worldwide are prompting nations to bolster their military capabilities, driving demand for advanced defense systems like fighter jets, missiles, and surveillance technologies. This surge in procurement enhances national security postures and stimulates innovation in stealth, precision, and cyber-resilient platforms. As alliances like NATO strengthen collective defense, collaborative projects further amplify market growth, fostering international partnerships in R&D and production.

Moreover, the integration of AI and unmanned systems in response to asymmetric threats expands application scopes, reducing human risk while improving operational efficiency. These dynamics not only increase government spending but also attract private investments, positioning the market for sustained expansion through technological superiority and strategic deterrence.

Restraints

- Supply Chain Disruptions

Global dependencies on specialized materials and components make the industry vulnerable to disruptions from geopolitical events, natural disasters, or trade restrictions, leading to production delays and cost escalations. This fragility affects timelines for critical programs, potentially compromising delivery schedules and contractual obligations. Regulatory hurdles in sourcing rare earth elements further complicate logistics, increasing reliance on limited suppliers.

Additionally, the post-pandemic recovery has highlighted bottlenecks in skilled labor and manufacturing capacity, exacerbating backlogs. These issues constrain scalability, particularly for high-volume commercial aircraft production, necessitating diversified sourcing strategies to mitigate risks and ensure continuity in a volatile global environment.

Opportunities

- Advancements in Sustainable Aviation

The push for eco-friendly technologies, such as electric propulsion and sustainable fuels, opens avenues for innovation in reducing carbon emissions, aligning with global environmental goals. This shift attracts investments in hybrid aircraft and bio-based materials, expanding market reach to green-conscious operators. Regulatory incentives for low-emission solutions further accelerate adoption, creating new revenue streams.

Furthermore, collaborations with energy sectors enhance R&D in battery technologies and hydrogen systems, fostering cross-industry synergies. This opportunity not only addresses climate challenges but also differentiates players through sustainable offerings, enhancing competitiveness in an evolving regulatory landscape.

Challenges

- High Development Costs

The substantial investments required for R&D in cutting-edge technologies like hypersonics and space systems strain budgets, particularly for smaller firms, limiting the pace. Cost overruns in complex programs can lead to financial pressures and project cancellations. Stringent certification processes add to expenses, delaying market entry.

In addition, fluctuating raw material prices amplify economic uncertainties, impacting profitability. These challenges demand efficient cost management and public-private partnerships to share risks, ensuring viable progression in high-stakes developments.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 961.7 Billion |

Projected Market Size in 2034 |

USD 2027.39 Billion |

CAGR Growth Rate |

8.64% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Lockheed Martin, RTX Corporation, Boeing, Northrop Grumman, General Dynamics, Airbus, BAE Systems, Honeywell International, Safran, Leonardo S.p.A., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Aerospace and Defense market is segmented by type, application, end-user, and region.

Based on Type Segment, The Aerospace and Defense market is divided into Air-based, Land-based, Sea-based, Space-based, and others. The most dominant segment is Air-based, which holds the largest share due to extensive use in commercial aviation and military operations for transportation and combat superiority, driving the market by supporting global connectivity and defense strategies; the second most dominant is Space-based, growing rapidly for satellite communications and exploration, contributing to market expansion through advancements in navigation and earth observation technologies.

Based on Application Segment, The Aerospace and Defense market is divided into Aviation, Military Operations, Maritime, Space Exploration, and others. The most dominant segment is Aviation, commanding the highest share because of rising air passenger demand and fleet expansions, which drives the market by enhancing economic growth and tourism; the second most dominant is Military Operations, essential for national security with investments in advanced weaponry, propelling market growth via technological innovations in surveillance and strike capabilities.

Based on End-User Segment, The Aerospace and Defense market is divided into Government & Military, Commercial Airlines, Space Agencies, and others. The most dominant segment is Government & Military, holding the biggest share due to substantial defense budgets and procurement programs, driving the market by ensuring geopolitical stability and technological leadership; the second most dominant is Commercial Airlines, fueled by increasing travel needs, contributing to market growth through efficient aircraft designs and sustainable practices.

Recent Developments

- In November 2025, global defense spending rose by nearly 10 percent in 2024, marking its fastest growth rate in nearly four decades, driven by geopolitical tensions and technological advancements.

- In July 2025, the U.S. Department of Defense awarded contracts to four leading AI companies to accelerate AI adoption across critical mission areas.

Regional Analysis

- North America to dominate the global market

North America leads the aerospace and defense market, anchored by the United States as the dominant country with its unparalleled military spending and innovation ecosystem hosting giants like Boeing and Lockheed Martin. The region's focus on advanced technologies such as AI-integrated systems and hypersonic weapons strengthens national security while driving exports. Robust R&D investments through agencies like NASA and the DoD foster breakthroughs in space exploration and unmanned platforms. Strategic alliances enhance interoperability, while a skilled workforce sustains manufacturing excellence. The U.S. dominance arises from its vast defense budget and policy frameworks promoting technological superiority.

Europe maintains a strong position through collaborative efforts like Airbus and multinational defense projects, with France as the dominant country leveraging its engineering heritage and export prowess. The region's emphasis on sustainable aviation and joint military initiatives under NATO bolsters resilience against threats. Investments in green technologies align with EU environmental goals, promoting hybrid propulsion and biofuels. France's leadership stems from its role in Airbus and advanced fighter programs, supported by government incentives for innovation and international partnerships.

Asia Pacific emerges rapidly with expanding capabilities in commercial and military sectors, led by China as the dominant country through massive investments in indigenous aircraft and space programs. The region's growing air travel demand fuels fleet expansions, while geopolitical dynamics spur defense modernizations. Technological leaps in drones and satellites enhance surveillance and communication. China's dominance originates from state-driven initiatives and supply chain integrations, enabling cost-effective production and global competitiveness.

Latin America shows potential through resource-based manufacturing and regional collaborations, with Brazil dominating via Embraer and space agency developments. Infrastructure projects and security needs drive aircraft acquisitions, while partnerships with global players transfer technologies. Brazil's lead comes from its established aerospace cluster and export focus, aiding economic diversification.

The Middle East & Africa advances with oil-funded modernizations and strategic acquisitions, led by Saudi Arabia through Vision 2030's localization efforts. Increasing defense budgets support fighter jets and UAVs for regional stability. Saudi Arabia's position strengthens from ambitious reforms and international alliances, fostering local industry growth.

Competitive Analysis

The global Aerospace and Defense market is dominated by players:

- Lockheed Martin

- RTX Corporation

- Boeing

- Northrop Grumman

- General Dynamics

- Airbus

- BAE Systems

- Honeywell International

- Safran

- Leonardo S.p.A.

The global Aerospace and Defense market is segmented as follows:

By Type

- Air-based

- Land-based

- Sea-based

- Space-based

- Others

By Application

- Aviation

- Military Operations

- Maritime

- Space Exploration

- Others

By End-User

- Government & Military

- Commercial Airlines

- Space Agencies

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

- Lockheed Martin

- RTX Corporation

- Boeing

- Northrop Grumman

- General Dynamics

- Airbus

- BAE Systems

- Honeywell International

- Safran

- Leonardo S.p.A.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors