![]()

Search Market Research Report

5G Fixed Wireless Access (FWA) Market Size, Share Global Analysis Report, 2026-2034

5G Fixed Wireless Access (FWA) Market Size, Share, Growth Analysis Report By Offering (Hardware, Services), By Operating Frequency (Sub-6 GHz, 24 GHz - 39 GHz, Above 39 GHz), By Demography (Urban, Semi-Urban, Rural), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

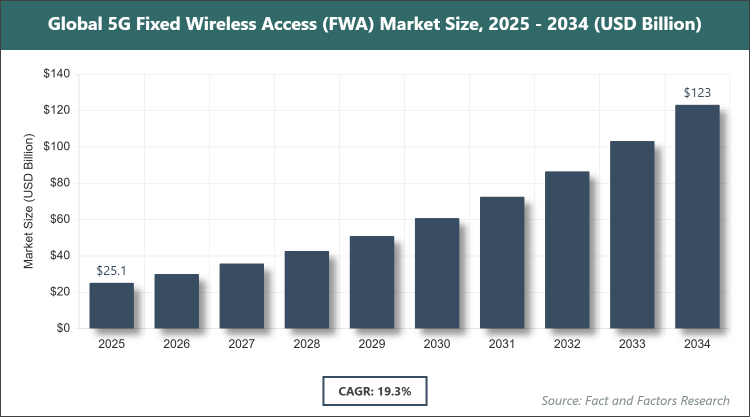

[250+ Pages Report] According to Facts & Factors, the global 5G Fixed Wireless Access (FWA) market size was estimated at USD 25.15 billion in 2025 and is expected to reach USD 121.59 billion by 2034, growing at a CAGR of 19.3% from 2026 to 2034. The 5G Fixed Wireless Access (FWA) Market is driven by surging demand for high-speed internet and cost-effective broadband alternatives in underserved areas.

The 5G Fixed Wireless Access (FWA) market refers to the provision of high-speed broadband internet using 5G wireless technology as a last-mile connectivity solution, delivering fiber-like speeds without the need for physical cables by leveraging radio spectrum to connect fixed locations such as homes and businesses to the network core. This technology bridges the digital divide in areas where traditional wired infrastructure is impractical or costly, enabling seamless data transmission for applications ranging from streaming to remote work through base stations and customer premises equipment that ensure low latency and high capacity.

Key Insights

Key Insights

- The global 5G Fixed Wireless Access (FWA) market was valued at USD 25.15 billion in 2025 and is projected to reach USD 121.59 billion by 2034.

- The market is expected to grow at a CAGR of 19.3% during the forecast period from 2026 to 2034.

- The market is driven by rapid 5G infrastructure rollout, increasing adoption of IoT devices, and government initiatives for rural connectivity.

- Based on the Offering segment, Services subsegment dominated with 65% share due to the growing need for installation, maintenance, and managed services in deploying complex 5G networks.

- Based on the Operating Frequency segment, Sub-6 GHz subsegment dominated with 55% share owing to its superior coverage and penetration in diverse terrains compared to higher frequencies.

- Based on the Demography segment, Semi-Urban subsegment dominated with 45% share because of balanced demand for high-speed internet in transitioning areas with limited wired options.

- North America dominated the global market with 40% share attributed to early 5G deployments, strong telecom investments, and supportive policies in the United States.

Growth Drivers

- Surging Demand for High-Speed Broadband

The escalating need for reliable, high-bandwidth connectivity driven by remote work, online education, and streaming services has propelled the adoption of 5G FWA as an efficient alternative to traditional broadband, particularly in regions lacking fiber optic infrastructure. This demand is further amplified by the proliferation of smart devices and IoT applications requiring low-latency connections.

Additionally, telecom operators are investing heavily in 5G spectrum and base stations to meet consumer expectations, fostering market expansion through scalable solutions that offer gigabit speeds without extensive trenching or cabling costs.

Restraints

- Spectrum Availability and Regulatory Hurdles

Limited access to suitable spectrum bands and varying regulatory frameworks across countries hinder widespread deployment, as operators face challenges in securing allocations for sub-6 GHz and mmWave frequencies essential for optimal performance. This constraint delays rollouts and increases operational complexities.

Moreover, environmental and health concerns related to radio frequency emissions lead to stricter approval processes, potentially stalling projects and raising compliance costs for providers aiming to expand coverage.

Opportunities

- Expansion in Rural and Underserved Areas

Government subsidies and initiatives for digital inclusion create avenues for 5G FWA to penetrate remote locations, offering cost-effective broadband where wired alternatives are uneconomical. This opens markets in developing regions with growing internet penetration.

Furthermore, partnerships between telecom firms and tech companies for integrated solutions like smart city projects enhance applicability, driving revenue through customized offerings for agriculture, healthcare, and education sectors.

Challenges

- Technical Limitations and Infrastructure Costs

Line-of-sight requirements for mmWave frequencies and susceptibility to weather interference pose reliability issues, necessitating advanced beamforming and additional equipment that elevate initial deployment expenses. This challenge affects adoption in dense or obstructed environments.

Ongoing needs for network densification and upgrades to support increasing data traffic add to capital burdens, requiring operators to balance innovation with affordability to maintain competitive edges.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 25.15 Billion |

Projected Market Size in 2034 |

USD 121.59 Billion |

CAGR Growth Rate |

19.3% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Huawei Technologies Co., Ltd., Nokia Corporation, Ericsson AB, Samsung Electronics Co., Ltd., Qualcomm Incorporated, Verizon Communications Inc., Intel Corporation, MediaTek Inc., CommScope Holding Company, Inc., Inseego Corp., and Others. |

Key Segment |

By Offering, By Operating Frequency, By Demography, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The 5G Fixed Wireless Access (FWA) market is segmented by offering, operating frequency, demography, and region.

Based on Offering Segment, the 5G Fixed Wireless Access (FWA) market is divided into Hardware and Services. The most dominant subsegment is Services, holding approximately 65% market share, primarily due to the essential role in network planning, deployment, and optimization that ensures seamless integration and performance; this dominance drives the market by enabling operators to focus on core competencies while outsourcing complex management, accelerating adoption, and reducing downtime. The second most dominant is Hardware, with around 35% share, crucial for providing customer premises equipment and base stations that deliver high-speed connectivity; it propels market growth through technological advancements in antennas and routers that enhance signal strength and capacity, supporting broader coverage.

Based on Operating Frequency Segment, the 5G Fixed Wireless Access (FWA) market is divided into Sub-6 GHz, 24 GHz - 39 GHz, and Above 39 GHz. Sub-6 GHz dominates with about 55% share, driven by its extensive range and better building penetration, ideal for widespread coverage in urban and rural settings; it contributes to market expansion by facilitating cost-effective deployments that reach more users without requiring dense infrastructure. 24 GHz - 39 GHz follows as the second dominant with 30% share, offering a balance of speed and coverage for high-capacity needs in semi-urban areas; this helps drive the market by enabling ultra-fast data rates for bandwidth-intensive applications like video conferencing.

Based on the Demography Segment, the 5G Fixed Wireless Access (FWA) market is divided into Urban, Semi-Urban, and Rural. Semi-Urban leads with roughly 45% share, attributed to growing populations in suburban areas seeking affordable high-speed alternatives to saturated wired networks; this segment boosts the overall market by addressing connectivity gaps in expanding communities, promoting digital inclusion. Rural ranks second with 30% share, benefiting from FWA's ability to serve remote locations economically without extensive cabling; it drives growth by connecting underserved populations to essential services like telemedicine and e-learning.

Recent Developments

- In January 2026, Verizon expanded its 5G FWA service to additional rural areas in the US, reporting a 20% increase in subscriber growth through enhanced mmWave technology integrations.

- In October 2025, Nokia partnered with a major Asian telecom provider to deploy Sub-6 GHz FWA solutions, focusing on semi-urban connectivity to support smart city initiatives.

- In July 2025, Huawei launched advanced CPE hardware with AI-driven beamforming, aimed at improving signal reliability in challenging environments.

Regional Analysis

- North America to dominate the global market

North America holds over 40% market share, fueled by aggressive 5G rollouts and federal funding for broadband expansion, with the United States dominating through operators like Verizon and T-Mobile that leverage extensive spectrum holdings to deliver multi-gigabit speeds, enhancing economic productivity and bridging urban-rural divides.

Europe follows with steady advancement, emphasizing sustainable connectivity under EU digital agendas, where Germany leads with investments in industrial IoT applications using FWA for manufacturing hubs, supported by regulatory incentives for green tech.

Asia-Pacific emerges rapidly, driven by urbanization and government-backed 5G plans, with China dominating via massive infrastructure builds by Huawei and ZTE, enabling high-density deployments in semi-urban zones to support e-commerce and education.

Latin America shows promising growth, focusing on affordability in emerging economies, with Brazil leading through Anatel-regulated expansions in rural broadband, aiding agriculture and remote work.

The Middle East & Africa region progresses, prioritizing connectivity in oil-rich and developing areas, with the UAE dominating in the Middle East through Etisalat's smart city projects, while South Africa leads in Africa with Vodacom's FWA for mining and urban extensions.

Competitive Analysis

The global 5G Fixed Wireless Access (FWA) market is dominated by players:

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Ericsson AB

- Samsung Electronics Co., Ltd.

- Qualcomm Incorporated

- Verizon Communications Inc.

- Intel Corporation

- MediaTek Inc.

- CommScope Holding Company, Inc.

- Inseego Corp.

The global 5G Fixed Wireless Access (FWA) market is segmented as follows:

By Offering

- Hardware

- Services

By Operating Frequency

- Sub-6 GHz

- 24 GHz - 39 GHz

- Above 39 GHz

By Demography

- Urban

- Semi-Urban

- Rural

By Regional

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors