![]()

Search Market Research Report

3D Animation Software Market Size, Share Global Analysis Report, 2026-2034

3D Animation Software Market Size, Share, Growth Analysis Report By Technology (3D Modeling, Motion Graphics, 3D Rendering, Visual Effects (VFX), and Others), By Service (Consulting, Support and Maintenance, Integration and Deployment, Education and Training), By Deployment (On-premises, Cloud-based), By Vertical (Media and Entertainment, Construction and Architecture, Healthcare and Lifesciences, Manufacturing, Education and Research, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

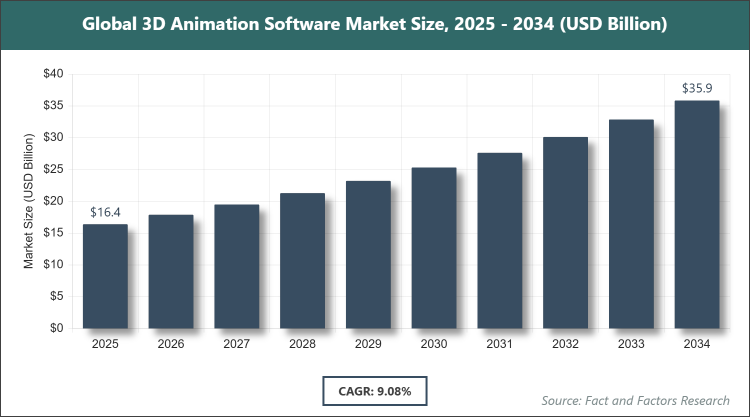

[245+ Pages Report] According to Facts & Factors, the global 3D animation software market size was estimated at USD 16.4 billion in 2025 and is expected to reach USD 36.8 billion by the end of 2034. The 3D animation software industry is anticipated to grow by a CAGR of 9.08% between 2026 and 2034. The 3D animation software Market is driven by escalating demand for visual content in entertainment, gaming, and advertising.

Market Overview

Market Overview

3D animation software refers to specialized computer programs designed to create three-dimensional moving images and visual effects. These tools enable artists, designers, and animators to model, texture, light, animate, and render objects in a virtual 3D space, simulating real-world physics and behaviors. Widely used across various industries, this software facilitates the production of realistic animations for films, video games, architectural visualizations, medical simulations, and educational content. It typically includes features like keyframe animation, motion capture integration, particle systems, and advanced rendering engines to produce high-quality outputs.

Key Insights

- As per the analysis shared by our research analyst, the global 3D animation software market is estimated to grow annually at a CAGR of around 9.08% over the forecast period (2026-2034).

- In terms of revenue, the global 3D animation software market size was valued at around USD 16.4 billion in 2025 and is projected to reach USD 36.8 billion by 2034.

- The market is driven by increasing demand for high-quality visual effects in media and entertainment, advancements in AI and cloud computing, and growth in gaming and VR/AR applications.

- Based on the technology, the 3D modeling segment dominated with 33.2% share due to its fundamental role in creating base structures for animations.

- Based on the deployment, the on-premises segment dominated with 58.7% share owing to data security concerns and customization needs in large enterprises.

- Based on the vertical, the media and entertainment segment dominated with 37.6% share because of the high demand for VFX in films and games.

- North America dominated the global market with 38.9% share attributed to the presence of major animation studios and technological advancements.

Growth Drivers

- Escalating Need for Visual Content

The rising demand for engaging visual content across entertainment, gaming, advertising, and marketing sectors is a primary driver for the 3D animation software market. This surge is fueled by the proliferation of digital platforms, where high-quality animations enhance user experiences and brand storytelling. As consumers increasingly prefer immersive and realistic media, industries are investing heavily in advanced software to produce captivating visuals that stand out in a competitive landscape.

Furthermore, the integration of 3D animations in e-learning and virtual simulations has expanded the market's scope, allowing for interactive and educational content that improves retention and understanding. This driver not only boosts adoption among large enterprises but also empowers small creators through accessible tools, fostering innovation and market expansion.

- Technological Advancements in AI and ML

Advancements in artificial intelligence and machine learning are revolutionizing 3D animation by automating complex processes like rigging, texturing, and motion capture, reducing production time and costs. These technologies enable more realistic animations with minimal human intervention, making high-end effects accessible to a broader range of users, including independent developers.

In addition, AI-powered tools facilitate predictive analytics for animation outcomes, enhancing efficiency and creativity. This driver is particularly impactful in fast-paced industries like gaming, where quick iterations are essential, driving overall market growth by lowering barriers to entry and encouraging widespread adoption.

- Growth of VR and AR Applications

The expanding use of virtual reality and augmented reality in gaming, education, and training is propelling the demand for sophisticated 3D animation software. These technologies require seamless, real-time animations to create immersive environments, pushing software developers to innovate with features like real-time rendering and spatial audio integration.

Moreover, AR/VR's application in sectors like healthcare for surgical simulations and architecture for virtual walkthroughs further amplifies this driver. By enabling lifelike interactions, it not only drives market revenue but also opens new avenues for software customization and integration with emerging hardware.

Restraints

- High Costs of Implementation

The substantial initial investment required for high-end 3D animation software, including licenses, hardware, and training, acts as a significant restraint, particularly for small and medium-sized enterprises. This financial barrier limits accessibility in emerging markets where budget constraints are prevalent, slowing overall adoption rates.

Additionally, ongoing maintenance and upgrade costs exacerbate this issue, as rapid technological evolution necessitates frequent investments. This restraint hinders market penetration in cost-sensitive regions and industries, potentially stifling innovation among smaller players who cannot afford premium tools.

- Cybersecurity and Data Privacy Concerns

Increasing reliance on cloud-based deployments raises vulnerabilities to cyber threats and data breaches, restraining market growth as organizations prioritize security over convenience. In industries handling sensitive intellectual property, such as media and entertainment, these concerns lead to hesitation in adopting cloud solutions.

Furthermore, regulatory compliance with data protection laws adds complexity and costs, deterring potential users. This restraint impacts global expansion, especially in regions with stringent privacy regulations, limiting the shift from on-premises to more scalable cloud options.

Opportunities

- Expansion in Emerging Markets

Rapid digitalization in regions like Asia Pacific presents opportunities for market growth, with increasing investments in film, gaming, and e-learning industries. Local content creation and government initiatives supporting digital media create a fertile ground for software providers to expand their footprint.

Moreover, affordable mobile devices and improving internet infrastructure enable broader access to 3D tools, fostering a new wave of creators. This opportunity allows companies to tailor solutions for regional needs, driving revenue through localized partnerships and training programs.

- Integration with 5G Technology

The rollout of 5G networks offers opportunities for enhanced cloud gaming, real-time collaboration, and AR/VR experiences, boosting demand for advanced 3D animation software. Faster data speeds and lower latency enable seamless remote workflows, appealing to global teams in animation production.

In addition, 5G facilitates mobile-optimized animations, expanding market reach to handheld devices. This opportunity encourages innovation in software features, positioning providers to capture growth in telecommunications and interactive media sectors.

Challenges

- Shortage of Skilled Workforce

The complex nature of 3D animation requires specialized skills, and the global shortage of trained professionals poses a challenge to market growth. This gap leads to longer project timelines and higher training costs for enterprises adopting new software.

Furthermore, rapid advancements in tools outpace educational curricula, exacerbating the skills mismatch. This challenge affects industries reliant on high-quality outputs, potentially delaying adoption and innovation in regions with limited access to training resources.

- Competition from Open-Source Alternatives

The availability of free or low-cost open-source 3D animation tools intensifies competition, challenging premium software providers to differentiate through advanced features. Users, especially independents, opt for these alternatives to avoid high costs, eroding market share for established players.

Additionally, open-source communities drive rapid innovations, pressuring commercial vendors to invest heavily in R&D. This challenge requires strategic pricing and value-added services to retain customers in a democratized market landscape.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 16.4 Billion |

Projected Market Size in 2034 |

USD 36.8 Billion |

CAGR Growth Rate |

9.08% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Adobe Systems Inc., Autodesk Inc., Autodessys Inc., Corel Corporation, Maxon Computer, Newtek Inc., Nvidia Corporation, Pixologic Inc., Sidefx Software, The Foundry Visionmongers Ltd., Toon Boom Animation Inc., Trimble Navigation Ltd., Zco Corporation, and Others. |

Key Segment |

By Technology, By Service, By Deployment, By Vertical, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The 3D animation software market is segmented by technology, service, deployment, vertical, and region.

Based on Technology Segment, the 3D animation software market is divided into 3D modeling, motion graphics, 3D rendering, visual effects (VFX), and others. The most dominant segment is 3D modeling, which serves as the foundational step in animation pipelines, allowing users to create detailed digital assets essential for all subsequent processes; its dominance stems from its versatility across industries, driving market growth by enabling efficient workflows and realistic simulations that enhance overall production quality. The second most dominant is visual effects (VFX), which integrates seamlessly with live-action footage to produce stunning cinematic experiences, dominating due to surging demand in blockbuster films and streaming content, thereby propelling the market through increased investments in high-fidelity visuals that captivate audiences and boost revenue.

Based on Service Segment, the 3D animation software market is divided into consulting, support and maintenance, integration and deployment, education and training. The most dominant segment is support and maintenance, critical for ensuring software reliability and uptime in mission-critical applications; it dominates because ongoing technical assistance minimizes disruptions, driving market expansion by building user trust and encouraging long-term subscriptions. The second most dominant is integration and deployment, which facilitates seamless incorporation into existing systems, leading due to the complexity of modern IT environments, thus accelerating market growth through customized solutions that optimize performance and reduce implementation time.

Based on Deployment Segment, the 3D animation software market is divided into on-premises, cloud-based. The most dominant segment is on-premises, preferred for its control over data security and customization in sensitive industries; its dominance arises from regulatory compliance needs, contributing to market drive by supporting large-scale operations that require robust, localized infrastructure. The second most dominant is cloud-based, offering scalability and remote access, gaining traction with collaborative workflows; it helps drive the market by lowering entry barriers for SMEs and enabling real-time updates that foster innovation.

Based on Vertical Segment, the 3D animation software market is divided into media and entertainment, construction and architecture, healthcare and lifesciences, manufacturing, education and research, and others. The most dominant segment is media and entertainment, where high-demand for immersive content like films and games fuels adoption; it dominates owing to massive investments in VFX, driving the market by generating high revenue through blockbuster productions and streaming platforms. The second most dominant is construction and architecture, utilizing software for virtual visualizations; its position stems from efficiency in design processes, propelling market growth via reduced project costs and enhanced client presentations.

Recent Developments

- In October 2024, Autodesk acquired Wonder Dynamics and introduced Wonder Animation, a tool that transforms videos into editable 3D sequences, enhancing efficiency in animation workflows and enabling creators to integrate AI for faster production.

- In August 2024, Viggle AI, a Toronto-based company, raised $19 million in Series A funding to advance AI-powered character animation, aiming to democratize high-quality animations for indie developers and small studios.

- In December 2023, Spaceblock released new 3D animations on the Unreal Engine Marketplace, utilizing motion capture technology to provide ready-to-use assets that accelerate game development and visual effects creation.

- In September 2024, Adobe Systems Inc. added innovative tools to the 3D workspace in Adobe After Effects, improving integration with other Creative Cloud applications and streamlining motion graphics for professionals.

- In January 2022, AT&T partnered with NVIDIA to enhance 5G cloud gaming experiences, leveraging advanced rendering for immersive animations that support real-time interactions in virtual environments.

- In February 2021, Disney+ launched the Star brand in multiple regions, expanding access to animated content and driving demand for sophisticated 3D software in global content production.

Regional Analysis

- North America to dominate the global market

North America continues to lead the 3D animation software market, primarily driven by the United States, which hosts major animation studios and tech giants innovating in VFX and gaming. The region's advanced infrastructure supports seamless adoption of cutting-edge tools, fostering a vibrant ecosystem of creative professionals. Collaborations between software developers and entertainment industries enhance product development, while strong educational institutions produce skilled talent. This dominance stems from a culture of innovation and high consumer demand for immersive media experiences.

Europe exhibits strong growth in the 3D animation software market, with the United Kingdom emerging as a key player due to its thriving film and gaming sectors. The region's emphasis on cultural content and interactive media drives software utilization in diverse applications. Supportive policies for digital arts and collaborations with global tech firms bolster market expansion. Educational programs focused on digital skills further strengthen the workforce, enabling intricate animations for advertising and education.

Asia Pacific is rapidly advancing in the 3D animation software market, led by China, where booming film and gaming industries fuel demand for advanced tools. Local content creation and government initiatives in digital media accelerate adoption across entertainment and education sectors. The region's youthful demographic embraces VR/AR technologies, promoting innovative applications. Partnerships with international players enhance technological capabilities, positioning Asia Pacific as a hub for cost-effective yet high-quality animation production.

Latin America shows promising potential in the 3D animation software market, with Brazil dominating through its vibrant media landscape and growing streaming platforms. Increasing investments in local productions and interactive content drive software integration for visual storytelling. The region's cultural diversity inspires unique animations, attracting global collaborations. Improving digital infrastructure supports remote workflows, enabling small studios to compete internationally and expand market reach.

The Middle East and Africa are emerging in the 3D animation software market, with the United Arab Emirates leading through ambitious entertainment projects and tech hubs. Rapid mobile penetration facilitates access to animation tools for gaming and education. Government efforts to diversify economies into digital media foster skill development and innovation. Collaborations with global firms bring advanced technologies, enhancing local capabilities for creating engaging content tailored to regional audiences.

Competitive Analysis

The global 3D animation software market is dominated by players:

- Adobe Systems Inc.

- Autodesk Inc.

- Autodessys Inc.

- Corel Corporation

- Maxon Computer

- Newtek Inc.

- Nvidia Corporation

- Pixologic Inc.

- Sidefx Software

- The Foundry Visionmongers Ltd.

- Toon Boom Animation Inc.

- Trimble Navigation Ltd.

- Zco Corporation

The global 3D animation software market is segmented as follows:

By Technology

- 3D Modeling

- Motion Graphics

- 3D Rendering

- Visual Effects (VFX)

- Others

By Service

- Consulting

- Support and Maintenance

- Integration and Deployment

- Education and Training

By Deployment

- On-premises

- Cloud-based

By Vertical

- Media and Entertainment

- Construction and Architecture

- Healthcare and Lifesciences

- Manufacturing

- Education and Research

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table of Content

Industry Major Market Players

The global 3D animation software market is dominated by players:

- Adobe Systems Inc.

- Autodesk Inc.

- Autodessys Inc.

- Corel Corporation

- Maxon Computer

- Newtek Inc.

- Nvidia Corporation

- Pixologic Inc.

- Sidefx Software

- The Foundry Visionmongers Ltd.

- Toon Boom Animation Inc.

- Trimble Navigation Ltd.

- Zco Corporation

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors