![]()

Search Market Research Report

Rubber Compound Market Size, Share Global Analysis Report, 2026-2034

Rubber Compound Market Size, Share, Growth Analysis Report By Type (Synthetic Rubber, Natural Rubber), By Rubber Type (Silicone Rubber, Fluoro Rubber, Butyronitrile Rubber, EPDM Rubber, Chloroprene Rubber, Others), By Processing Method (Compression Molding, Injection Molding, Other Methods), By Application (Tires, Hose and Belting, Roofing and Geo Membranes, Footwear, Wire and Cable Insulation, Others), By End-User (Building & Construction, Automotive & Transportation, Industrial Machinery Equipment, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

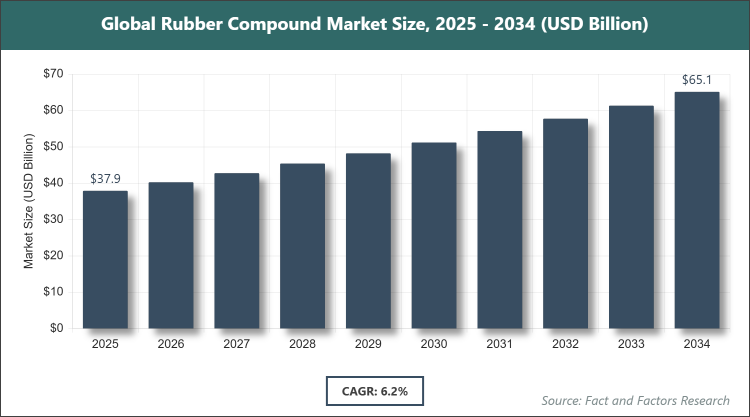

[250+ Pages Report] According to Facts & Factors, the global Rubber Compound market size was estimated at USD 37.9 billion in 2025 and is expected to reach USD 65.2 billion by 2034, growing at a CAGR of 6.2% from 2026 to 2034. Rubber Compound Market is driven by rising demand from automotive and industrial sectors.

Market Overview

Market Overview

Rubber compounds are specialized mixtures created by blending raw rubber polymers with various additives such as fillers, accelerators, antioxidants, and curing agents to enhance properties like elasticity, durability, abrasion resistance, and chemical stability, tailored for specific applications across industries. These compounds serve as the foundational material for manufacturing a wide array of products, from tires and seals to hoses and vibration isolators, enabling customization to meet performance requirements in demanding environments while ensuring processability during molding, extrusion, or calendering without compromising on end-product quality or functionality.

Key Insights

- The Rubber Compound market was valued at USD 37.9 Billion in 2025 and is projected to reach USD 65.2 Billion by the end of 2034.

- The market is expected to grow at a CAGR of 6.2% between 2026 and 2034.

- The Rubber Compound market is driven by rising demand from automotive and industrial sectors.

- Based on the Type segment, the Synthetic Rubber subsegment dominated the market in 2025 with a share of 57.0% because of its superior performance characteristics and versatility in various applications.

- Based on the Rubber Type segment, the EPDM Rubber subsegment dominated the market in 2025 with a share of 30.0% because of its excellent weather resistance and use in automotive seals.

- Based on the Processing Method segment, the Injection Molding subsegment dominated the market in 2025 with a share of 45.0% because of its efficiency in high-volume production.

- Based on the Application segment, the Tires subsegment dominated the market in 2025 with a share of 58.7% because of high demand from the automotive industry.

- Based on the End-User segment, the Automotive & Transportation subsegment dominated the market in 2025 with a share of 50.0% because of extensive use in vehicle components.

- Asia Pacific held the largest market share of 53.75% in 2025 due to rapid industrialization and major rubber production hubs like China and India.

Growth Drivers

- Rising Applications in the Automotive Sector

The automotive industry's expansion, particularly in tire production and components like seals and hoses, has significantly increased demand for high-performance rubber compounds that offer enhanced durability and fuel efficiency. This driver is supported by the growth in electric vehicles and stringent emission regulations, pushing manufacturers to innovate with lightweight and sustainable compounds to meet evolving standards.

- Industrial Applications and Infrastructure Development

Growing use in industrial machinery, construction, and building materials for vibration isolation and sealing has propelled market growth, as these sectors require robust, weather-resistant compounds. This is amplified by global infrastructure investments and urbanization in emerging economies, fostering demand for reliable rubber solutions in harsh environments.

- Advancements in Sustainable and Bio-Based Compounds

Innovations in eco-friendly rubber compounds using recycled materials and bio-based polymers are driving adoption, aligning with environmental regulations and consumer preferences for green products. This trend encourages R&D investments, enabling companies to differentiate offerings and capture premium segments in automotive and consumer goods.

Restraints

- Environmental Impact of Industry Operations

The production process's high carbon footprint and waste generation pose restraints, as stricter environmental regulations increase compliance costs and limit traditional methods. This challenge affects profitability, compelling shifts to sustainable practices that may initially raise expenses and disrupt supply chains.

- Volatile Raw Material Prices

Fluctuations in natural rubber and petrochemical prices, influenced by geopolitical factors and supply disruptions, hinder cost stability for manufacturers. This restraint impacts pricing strategies and margins, particularly in price-sensitive markets, potentially slowing expansion.

Opportunities

- Growth in Electric Vehicles and Advanced Mobility

The rise of EVs creates opportunities for specialized compounds with thermal management and lightweight properties, tailored for battery seals and insulation. This can be capitalized on through collaborations with automakers, unlocking new revenue streams in high-growth sectors.

- Expansion in Emerging Markets

Increasing industrialization in Asia-Pacific and Latin America offers opportunities for affordable, customized compounds in automotive and construction. This enables market penetration via local production and partnerships, addressing regional demands efficiently.

Challenges

- Raw Material Supply Disruptions

Dependence on natural rubber from specific regions exposes the market to weather-related shortages and trade issues, causing inconsistencies. This requires diversified sourcing and inventory management, straining operations for smaller players.

- Regulatory Compliance and Sustainability Mandates

Evolving global standards on recyclability and emissions challenge manufacturers to reformulate products without compromising performance. This demands significant R&D investment, potentially delaying innovations and market entry.

Report Scope

Report Attribute |

Details |

Market Size in 2025 |

USD 37.9 Billion |

Projected Market Size in 2034 |

USD 65.2 Billion |

CAGR Growth Rate |

6.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Hexpol Compounding, AirBoss Rubber Compounding, DynaSol Elastomers, General Seal Corporation, Hutchinson, Cooper Standard, Continental AG, Sumitomo Rubber Industries Ltd., The Goodyear Tire and Rubber Company, Avon Rubber Plc., Fenner PLC, Yokohama Rubber Company Ltd., Parker Hannifin Corporation, Federal-Mogul Corporation, Eaton Corporation PLC, Gates Corporation, Freudenberg Group, Trelleborg AB, ExxonMobil Chemical, LANXESS AG, and Others. |

Key Segment |

By Type, By Rubber Type, By Processing Method, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East &, Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Rubber Compound market is segmented by type, application, end-user, and region.

Based on Type Segment, The Rubber Compound market is divided into Synthetic Rubber, and Natural Rubber. The most dominant segment is Synthetic Rubber, holding 57.0% share, due to its customizable properties like heat resistance and strength, driving market growth through applications in high-demand industries such as automotive and electronics; the second most dominant is Natural Rubber, which supports market expansion by offering biodegradability and elasticity, essential for eco-friendly products and traditional uses like tires.

Based on Rubber Type Segment, The Rubber Compound market is divided into Silicone Rubber, Fluoro Rubber, Butyronitrile Rubber, EPDM Rubber, Chloroprene Rubber, and Others. The most dominant segment is EPDM Rubber, with 30.0% share, owing to its superior weather and ozone resistance, propelling market growth in roofing and automotive seals; the second most dominant is Silicone Rubber, contributing through its high-temperature stability, enhancing applications in medical and electrical insulation.

Based on Processing Method Segment, The Rubber Compound market is divided into Compression Molding, Injection Molding, and Other Methods. The most dominant segment is Injection Molding, capturing 45.0% share, because of its precision and efficiency in mass production, fueling market expansion for complex parts; the second most dominant is Compression Molding, aiding growth by enabling cost-effective manufacturing for large components.

Based on Application Segment, The Rubber Compound market is divided into Tires, Hose and Belting, Roofing and Geo Membranes, Footwear, Wire and Cable Insulation, and Others. The most dominant segment is Tires, with 58.7% share, driven by global vehicle demand and performance requirements, accelerating market growth via innovation in tread compounds; the second most dominant is Hose and Belting, boosting the market through industrial durability needs.

Based on End-User Segment, The Rubber Compound market is divided into Building & Construction, Automotive & Transportation, Industrial Machinery Equipment, and Others. The most dominant segment is Automotive & Transportation, holding 50.0% share, due to extensive component usage and EV trends, driving market growth with lightweight solutions; the second most dominant is Industrial Machinery Equipment, contributing via vibration control applications.

Recent Developments

- In January 2025, Hexpol launched GreenTread MX, a bio-based rubber compound developed using natural oils and recycled elastomers for use in passenger vehicle tires.

- In February 2025, AirBoss of America introduced ThermoFlex EV, a high-performance rubber compound engineered for electric vehicle battery insulation and thermal management.

- In March 2025, Synthos S.A. announced the commercial availability of DuraSil 920, a new generation of silane-modified SBR compounds optimized for high-load industrial hoses and belts.

- In April 2025, EcoRub Technologies AB unveiled ReTreadX Neo, a recycled rubber compound for lightweight mobility applications including scooters and e-bikes.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific dominates the Rubber Compound market with a 53.75% share, driven by rapid industrialization, major rubber production, and booming automotive sectors; China leads the region as the largest producer and consumer, with its manufacturing hubs in Shanghai and Guangdong supporting low-cost production, government policies on EVs, and high demand for tires and industrial components.

North America shows steady growth, fueled by technological innovations and sustainability focus; the United States dominates, with advanced R&D in states like Ohio and Michigan, where automotive giants drive demand for high-performance compounds, supported by regulations on recycled materials.

Europe emphasizes eco-friendly practices and regulatory compliance; Germany leads, leveraging automotive excellence in Stuttgart and Munich for specialized compounds in luxury vehicles and machinery, aligned with EU sustainability directives.

Latin America exhibits potential with resource availability; Brazil dominates, utilizing natural rubber plantations in the Amazon for local production in Sao Paulo, addressing automotive and construction needs amid economic growth.

The Middle East and Africa are emerging, focused on diversification; South Africa leads in Africa with mining applications in Johannesburg, while Saudi Arabia drives in the Middle East through petrochemical integrations in Riyadh for export-oriented compounds.

Competitive Analysis

The global Rubber Compound market is dominated by players:

- Hexpol Compounding

- AirBoss Rubber Compounding

- DynaSol Elastomers

- General Seal Corporation

- Hutchinson

- Cooper Standard

- Continental AG

- Sumitomo Rubber Industries Ltd.

- The Goodyear Tire and Rubber Company

- Avon Rubber Plc.

- Fenner PLC

- Yokohama Rubber Company Ltd.

- Parker Hannifin Corporation

- Federal-Mogul Corporation

- Eaton Corporation PLC

- Gates Corporation

- Freudenberg Group

- Trelleborg AB

- ExxonMobil Chemical

- LANXESS AG

The global Rubber Compound market is segmented as follows:

By Type

- Synthetic Rubber

- Natural Rubber

By Rubber Type

- Silicone Rubber

- Fluoro Rubber

- Butyronitrile Rubber

- EPDM Rubber

- Chloroprene Rubber

- Others

By Processing Method

- Compression Molding

- Injection Molding

- Other Methods

By Application

- Tires

- Hose and Belting

- Roofing and Geo Membranes

- Footwear

- Wire and Cable Insulation

- Others

By End-User

- Building & Construction

- Automotive & Transportation

- Industrial Machinery Equipment

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors