![]()

Search Market Research Report

Reprocessed Digital Health Devices Market Size, Share Global Analysis Report, 2026-2034

Reprocessed Digital Health Devices Market Size, Share, Growth Analysis Report By Product (Cardiovascular, Laparoscopic, Gastroenterology, General Surgery Devices, Orthopedic), By Type (Third-party Reprocessing, In-house Reprocessing), By End-use (Hospitals, Home Healthcare, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

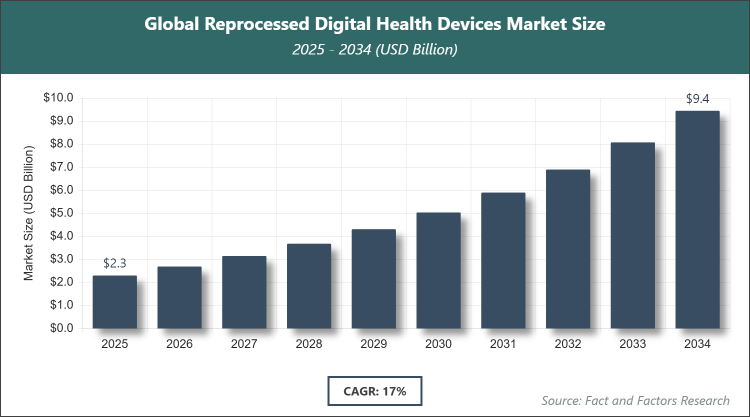

[220+ Pages Report] According to Facts & Factors, the global Reprocessed Digital Health Devices market size was estimated at USD 2.3 billion in 2025 and is expected to reach USD 9.5 billion by the end of 2034. The Reprocessed Digital Health Devices industry is anticipated to grow by a CAGR of 17% between 2026 and 2034. The Reprocessed Digital Health Devices Market is driven by the growing need to reduce medical waste and achieve cost savings in healthcare settings.

Market Overview

Market Overview

The Reprocessed Digital Health Devices market involves the systematic refurbishment of used digital health equipment, such as monitoring systems, diagnostic tools, and wearable technologies, through cleaning, sterilization, and functional testing to restore them to a safe and effective state for reuse. This market focuses on devices that incorporate digital components for data collection, analysis, and transmission in healthcare settings, ensuring they meet original manufacturer standards while promoting eco-friendly practices in the medical field.

Key Insights

- As per the analysis shared by our research analyst, the global Reprocessed Digital Health Devices market is estimated to grow annually at a CAGR of around 17% over the forecast period (2026-2034).

- In terms of revenue, the global Reprocessed Digital Health Devices market size was valued at around USD 2.3 billion in 2025 and is projected to reach USD 9.5 billion, by 2034.

- The Reprocessed Digital Health Devices market is primarily driven by the increasing focus on cost reduction and environmental sustainability in healthcare.

- Based on the Product, the Cardiovascular segment dominated with a share of 57% due to the high prevalence of cardiovascular diseases and the significant cost savings from reprocessing cardiac devices.

- Based on the Type, the Third-party Reprocessing segment dominated with a share of 66% because of specialized expertise and stringent quality control provided by external firms.

- Based on the End-use, the Hospitals segment dominated with a share of 43% owing to the large volume of procedures and need for cost-effective device management in hospital settings.

- Based on region, North America dominated with a share of 46% due to advanced regulatory frameworks, high healthcare expenditure, and strong awareness of reprocessing benefits.

Growth Drivers

- Reduction in Medical Waste

The healthcare sector generates substantial waste from disposable devices, contributing to environmental pollution and resource depletion. Reprocessing digital health devices helps mitigate this by extending device lifecycles, reducing the need for new production, and lowering the overall ecological footprint of medical operations.

This approach supports global sustainability initiatives, as institutions aim to achieve carbon-neutral goals and comply with strict waste management regulations, ultimately fostering a greener healthcare ecosystem.

- Cost Benefits and Savings

Reprocessed devices offer significant financial advantages, allowing healthcare providers to cut expenses by up to half compared to purchasing new equipment. This is crucial in an era of rising healthcare costs, enabling better resource allocation toward patient care and infrastructure improvements.

Moreover, in budget-constrained environments, reprocessing ensures access to high-quality digital health tools without compromising on performance, driving widespread adoption across various healthcare facilities.

- Rising Prevalence of Chronic Diseases

The global increase in chronic conditions like diabetes and cardiovascular disorders heightens the demand for continuous monitoring via digital health devices. Reprocessing makes these essential tools more affordable and accessible, supporting long-term disease management strategies.

This trend is amplified by an aging population requiring ongoing health tracking, where reprocessed devices play a key role in scaling up healthcare delivery without escalating costs.

Restraints

- Stringent Regulatory Requirements

Regulatory bodies impose rigorous standards for reprocessing to ensure device safety and efficacy, involving extensive documentation, testing, and compliance processes. This can increase operational complexities and costs for manufacturers and providers, potentially slowing market entry and expansion.

In regions with evolving regulations, such as the EU's MDR, the need for enhanced traceability and risk assessments further challenges smaller players, limiting innovation and market participation.

- Concerns Over Safety and Efficacy

Perceptions of potential risks associated with reprocessed devices, including infection or malfunction, can hinder adoption despite proven safety records. Healthcare professionals may prefer new devices for critical applications, affecting market trust.

Addressing these concerns requires ongoing education and evidence-based demonstrations of equivalence to original devices, but lingering doubts can restrain growth in conservative markets.

Opportunities

- Expansion Through Partnerships and Acquisitions

Strategic collaborations and mergers enable companies to enhance their reprocessing capabilities and expand product portfolios. For instance, acquisitions can integrate supply chains for better efficiency and broader market reach.

Such moves also facilitate entry into new geographies, leveraging combined expertise to meet diverse regulatory needs and capitalize on emerging demand for sustainable solutions.

- Growth in Emerging Markets

Developing regions offer untapped potential due to improving healthcare infrastructure and rising awareness of cost-effective practices. Investments in local reprocessing facilities can address equipment shortages and support economic growth.

With increasing chronic disease burdens, these markets present opportunities for tailored digital health solutions, driven by government initiatives promoting affordable healthcare access.

Challenges

- Fragmented Market Structure

The market features a mix of large players and numerous small providers, leading to inconsistencies in quality and pricing. This fragmentation can complicate standardization and trust-building among end-users.

Navigating this landscape requires robust industry associations to promote best practices, but competition may hinder collaborative efforts for overall market advancement.

- Supply Chain Disruptions

Global events can impact the availability of reprocessing materials and logistics, affecting timely device turnaround. Dependence on international suppliers exacerbates vulnerabilities in the chain.

Mitigating these requires diversified sourcing and resilient strategies, but ongoing disruptions pose risks to market stability and growth projections.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.3 Billion |

Projected Market Size in 2034 |

USD 9.5 Billion |

CAGR Growth Rate |

17% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Stryker, Innovative Health, NEScientific, Inc., Medline Industries, LP, Arjo, Cardinal Health, SureTek Medical, Soma Tech Intl, Johnson & Johnson MedTech, GE Healthcare, and Others. |

Key Segment |

By Product (Cardiovascular, Laparoscopic, Gastroenterology, General Surgery Devices, Orthopedic), By Type (Third-party Reprocessing, In-house Reprocessing), By End-use (Hospitals, Home Healthcare, Others), and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Reprocessed Digital Health Devices market is segmented by product, type, end-use, and region.

Based on Product Segment, the Reprocessed Digital Health Devices market is divided into Cardiovascular, Laparoscopic, Gastroenterology, General Surgery Devices, and Orthopedic.

The most dominant segment is Cardiovascular, followed by Laparoscopic as the second most dominant. The Cardiovascular segment dominates because of the widespread use of digital cardiac monitoring and diagnostic tools amid rising heart disease incidences worldwide, where reprocessing allows for substantial cost reductions while maintaining high accuracy in data transmission and analysis, thereby driving market expansion by enabling broader deployment in resource-limited settings and enhancing overall healthcare efficiency.

Based on Type Segment, the Reprocessed Digital Health Devices market is divided into Third-party Reprocessing, and In-house Reprocessing.

The most dominant segment is Third-party Reprocessing, followed by In-house Reprocessing as the second most dominant. Third-party Reprocessing dominates due to the specialized facilities and regulatory compliance expertise offered by external providers, which ensure superior quality control and scalability for complex digital devices, helping to drive the market by reducing in-house burdens on healthcare facilities and promoting wider adoption through reliable, cost-effective services.

Based on End-use Segment, the Reprocessed Digital Health Devices market is divided into Hospitals, Home Healthcare, and Others.

The most dominant segment is Hospitals, followed by Home Healthcare as the second most dominant. The Hospitals segment dominates because of the high procedural volumes and need for advanced digital health tools in clinical environments, where reprocessing supports budget optimization and sustainability goals, driving market growth by facilitating continuous access to innovative monitoring and diagnostic equipment without prohibitive costs.

Recent Developments

- In December 2024, Prestige AmeriTech acquired S2S Global from Premier Inc., enhancing product offerings in cardiology devices and improving supply chain resilience for reprocessed digital health solutions.

- In October 2023, GE Healthcare partnered with Relink Medical to optimize equipment management, addressing utilization and inventory challenges in reprocessing digital health devices.

- In August 2024, Arjo launched a new reprocessing facility to boost capabilities in handling single-use digital devices, supporting sustainability and cost-efficiency in healthcare.

- In July 2024, Innovative Health collaborated with MC Healthcare to raise awareness of reprocessing practices, promoting sustainable use of digital health devices in hospitals.

- In April 2024, GE Healthcare established a refurbishing unit in Bangladesh for ultrasound systems, improving accessibility to reprocessed digital imaging tools.

- In February 2024, GE Healthcare teamed up with Biofourmis for virtual care solutions, extending patient monitoring with reprocessed devices in home settings.

Regional Analysis

- North America to dominate the global market

North America maintains its leading position in the reprocessed digital health devices market, driven by sophisticated healthcare systems and proactive adoption of sustainable practices. The United States, as the dominating country, excels through established FDA regulations that facilitate safe reprocessing, coupled with a culture of innovation in digital health technologies. This region benefits from strong collaborations between manufacturers and providers, ensuring seamless integration of reprocessed devices into clinical workflows. Furthermore, emphasis on reducing healthcare costs while maintaining quality standards propels demand, with Canada contributing through similar regulatory alignments and focus on accessible care.

Europe demonstrates robust growth in the reprocessed digital health devices market, supported by stringent environmental policies and a commitment to circular economy principles. Germany stands out as the dominating country, leveraging its advanced engineering expertise and stable regulations that encourage reprocessing without compromising safety. The region's aging population drives the need for reliable digital monitoring tools, with countries like the UK and France enhancing market dynamics through national health initiatives. Collaborative efforts across the EU foster standardization, enabling efficient cross-border trade and adoption of reprocessed technologies in diverse healthcare settings.

Asia Pacific emerges as the fastest-growing region for reprocessed digital health devices, fueled by rapid urbanization and expanding healthcare access. China dominates as the key country, with its massive population and government push for affordable medical solutions amid rising chronic diseases. The region sees increasing investments in reprocessing infrastructure, particularly in India and Japan, where cost sensitivities and technological advancements converge. This growth is bolstered by partnerships with global players, aiming to bridge gaps in device availability and promote sustainable health practices across varied economic landscapes.

Latin America presents promising opportunities in the reprocessed digital health devices market, characterized by evolving healthcare reforms and awareness of cost-effective alternatives. Brazil leads as the dominating country, benefiting from a large market size and initiatives to enhance device accessibility in both urban and rural areas. The region's focus on combating chronic conditions through digital tools drives reprocessing adoption, with Mexico and Argentina contributing via trade agreements and local manufacturing efforts. Overall, sustainability trends and regulatory improvements are key to unlocking further potential in this dynamic market.

The Middle East & Africa region is witnessing gradual expansion in the reprocessed digital health devices market, driven by investments in healthcare modernization and addressing disease burdens. South Africa emerges as the dominating country, with its relatively advanced infrastructure and collaborations with international firms facilitating reprocessing adoption. The area grapples with resource limitations but leverages growing awareness of environmental benefits, particularly in the UAE and Saudi Arabia through vision-led health strategies. This progress supports equitable access to digital health innovations, fostering long-term market development amid demographic shifts.

Competitive Analysis

The global Reprocessed Digital Health Devices market is dominated by players:

- Stryker

- Innovative Health

- NEScientific, Inc.

- Medline Industries, LP

- Arjo

- Cardinal Health

- SureTek Medical

- Soma Tech Intl

- Johnson & Johnson MedTech

- GE Healthcare

The global Reprocessed Digital Health Devices market is segmented as follows:

By Product

- Cardiovascular

- Laparoscopic

- Gastroenterology

- General Surgery Devices

- Orthopedic

By Type

- Third-party Reprocessing

- In-house Reprocessing

By End-use

- Hospitals

- Home Healthcare

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Reprocessed Digital Health Devices market is dominated by players:

- Stryker

- Innovative Health

- NEScientific, Inc.

- Medline Industries, LP

- Arjo

- Cardinal Health

- SureTek Medical

- Soma Tech Intl

- Johnson & Johnson MedTech

- GE Healthcare

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors