![]()

Search Market Research Report

Porcine Epidemic Diarrhea Vaccines Market Size, Share Global Analysis Report, 2026-2034

Porcine Epidemic Diarrhea Vaccines Market Size, Share, Growth Analysis Report By Type (Live Vaccines, Killed Vaccines, and Others), By Application (Piglets, Adult Pigs, and Others), By End-User (Veterinary Hospitals, Hog Production Farms, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

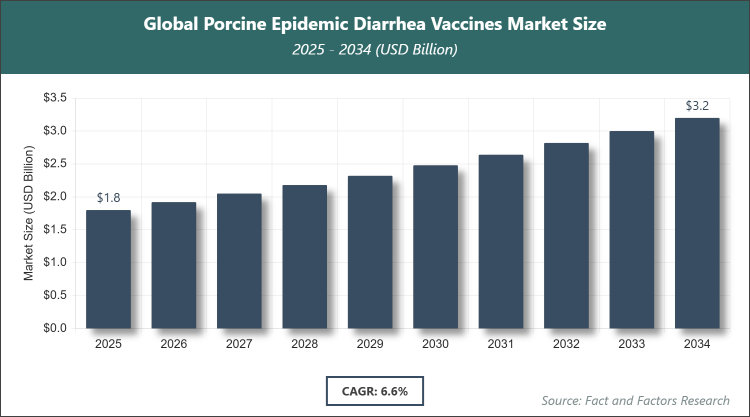

[235+ Pages Report] According to Facts & Factors, the global Porcine Epidemic Diarrhea Vaccines market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 3.2 billion by the end of 2034. The Porcine Epidemic Diarrhea Vaccines industry is anticipated to grow by a CAGR of 6.6% between 2026 and 2034. The Porcine Epidemic Diarrhea Vaccines Market is driven by rising global demand for pork products and increasing prevalence of PEDV outbreaks.

Market Overview

Market Overview

Porcine Epidemic Diarrhea Vaccines encompass biological agents designed to immunize swine against the Porcine Epidemic Diarrhea Virus, a coronavirus that induces acute enteritis, leading to severe dehydration and high fatality rates, particularly in neonatal piglets. These vaccines are pivotal in veterinary medicine for safeguarding herd health and preventing economic devastation in the pork industry through proactive disease management. They are formulated as live attenuated or inactivated variants, targeting the virus's spike protein to elicit protective immune responses, either directly in young pigs or via maternal antibodies transferred from vaccinated sows, thereby enhancing overall swine welfare without quantitative specifics.

Key Insights

- As per the analysis shared by our research analyst, the global Porcine Epidemic Diarrhea Vaccines market is estimated to grow annually at a CAGR of around 6.6% over the forecast period (2026-2034).

- In terms of revenue, the global Porcine Epidemic Diarrhea Vaccines market size was valued at around USD 1.8 billion in 2025 and is projected to reach USD 3.2 billion by 2034.

- The market is driven by the increasing prevalence of PEDV outbreaks and rising global pork consumption.

- Based on the type, the live vaccines segment dominated with a 60% share due to their ability to induce strong, long-lasting immunity.

- Based on the application, the piglets segment dominated with a 70% share owing to high vulnerability and mortality rates in young pigs.

- Based on the end-user, the hog production farms segment dominated with a 75% share because of large-scale operations requiring routine vaccinations.

- Based on the region, Asia Pacific dominated with a 40% share attributed to high pig populations and frequent outbreaks in China.

Growth Drivers

- Increasing Prevalence of PEDV Outbreaks

The surge in PEDV incidences worldwide, especially in densely populated swine farming areas, has amplified the necessity for robust vaccination strategies to curb widespread herd losses and maintain productivity. This driver is compounded by the globalization of trade, which facilitates virus spread, prompting farmers to adopt preventive measures.

Moreover, technological progress in vaccine formulation, including enhanced adjuvants and delivery systems, bolsters efficacy, encouraging broader implementation across commercial operations. These advancements align with industry shifts toward sustainable farming, reducing reliance on antibiotics.

Restraints

- High Development and Distribution Costs

Elevated expenses in research, clinical trials, and maintaining cold chain logistics restrict vaccine accessibility, particularly for small-scale farmers in resource-limited settings. This financial barrier can delay adoption and exacerbate outbreak impacts.

Additionally, stringent regulatory approvals vary by region, prolonging time-to-market for new products and increasing overall costs. Such restraints necessitate collaborative efforts between governments and manufacturers to subsidize or streamline processes.

Opportunities

- Advancements in Novel Vaccine Technologies

The emergence of recombinant, mRNA, and nanoparticle-based vaccines offers superior protection and adaptability to viral mutations, opening avenues for market expansion. These innovations cater to evolving needs for safer, more effective solutions.

Furthermore, untapped markets in developing regions with growing swine industries provide growth potential through localized manufacturing and awareness campaigns. Strategic partnerships can facilitate technology transfer and market penetration.

Challenges

- Viral Mutations Reducing Vaccine Efficacy

PEDV's genetic variability leads to strain mismatches, diminishing vaccine performance and requiring frequent updates. This challenge demands ongoing surveillance and R&D investment to stay ahead of evolutionary changes.

In addition, inadequate biosecurity in some farms undermines vaccination efforts, allowing persistent transmission. Addressing this involves integrated approaches combining education, infrastructure improvements, and policy enforcement.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 1.8 Billion |

Projected Market Size in 2034 |

USD 3.2 Billion |

CAGR Growth Rate |

6.6% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Zoetis Inc., Merck Animal Health, Elanco Animal Health, Boehringer Ingelheim Animal Health, Ceva Santé Animale, Phibro Animal Health Corporation, IDT Biologika GmbH, Vaxxinova, Qilu Animal Health Products Factory Co. Ltd., Green Cross Veterinary Products Co. Ltd., Nisseiken Co. Ltd., Komipharm International Co. Ltd., Harrisvaccines Inc., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Porcine Epidemic Diarrhea Vaccines market is segmented by type, application, end-user, and region.

Based on Type Segment, the Porcine Epidemic Diarrhea Vaccines market is divided into live vaccines, killed vaccines, and others. The most dominant segment is live vaccines, followed by killed vaccines as the second most dominant. Live vaccines dominate because they replicate natural infection to stimulate comprehensive immune responses, including mucosal immunity crucial for gastrointestinal protection, driving the market by effectively controlling outbreaks in endemic areas and reducing economic losses; killed vaccines, offering safety for use in pregnant animals without reversion risk, support growth by enabling maternal antibody transfer to vulnerable piglets, enhancing herd-wide resilience.

Based on Application Segment, the Porcine Epidemic Diarrhea Vaccines market is divided into piglets, adult pigs, and others. The most dominant segment is piglets, followed by adult pigs as the second most dominant. Piglets lead due to their immature immune systems making them highly susceptible to fatal PEDV infections, necessitating targeted vaccination to minimize mortality and sustain farm viability, thus propelling market demand; adult pigs, especially breeding sows, are vaccinated to generate colostral antibodies that protect offspring, contributing to market expansion by ensuring long-term herd health and productivity.

Based on End-User Segment, the Porcine Epidemic Diarrhea Vaccines market is divided into veterinary hospitals, hog production farms, and others. The most dominant segment is hog production farms, followed by veterinary hospitals as the second most dominant. Hog production farms dominate as they manage vast swine populations requiring systematic vaccination protocols to prevent disease spread and maintain export standards, driving the market through high-volume procurement; veterinary hospitals facilitate distribution and expert administration, aiding growth by providing diagnostic support and customized health programs for diverse clients.

Recent Developments

- In August 2024, Zoetis Inc. received a grant for PEDV vaccine research and a conditional license from the U.S. Department of Agriculture for a PEDV vaccine.

- In November 2024, Phibro Animal Health Corporation acquired Zoetis Inc. to broaden its product portfolio in animal health, including PEDV solutions.

- In February 2025, a PED outbreak in Hunan, China, led to the rapid development and deployment of an inactivated autogenous vaccine using infected piglet tissues, effectively controlling the spread.

- In June 2025, a study published on the safety and efficacy of live attenuated PEDV vaccines demonstrated promising results for neonatal piglet protection.

Regional Analysis

- Asia Pacific to Dominate the Global Market

The Asia Pacific region dominates the Porcine Epidemic Diarrhea Vaccines market, led by China, where the world's largest pig population and intensive farming practices amplify PEDV risks, driving extensive vaccine use to protect economic interests in pork production and ensure food security amid frequent viral challenges.

North America maintains a strong position, with the United States at the forefront, benefiting from advanced research facilities, proactive government policies on animal health, and large integrated farms that prioritize vaccination to mitigate losses and comply with stringent export regulations.

Europe exhibits steady growth, dominated by countries like Germany and Spain, supported by robust EU frameworks emphasizing biosecurity and welfare, which encourage vaccine adoption in commercial operations to prevent cross-border disease transmission and sustain competitive pork markets.

Latin America is emerging rapidly, with Brazil leading through expanding agribusiness and increasing investments in swine health to boost exports, addressing PEDV threats that could undermine regional economic gains from livestock.

The Middle East & Africa region shows gradual progress, spearheaded by South Africa, where developing commercial farming sectors are adopting vaccines to enhance productivity and reduce dependency on imports, despite challenges in infrastructure and awareness.

Competitive Analysis

The global Porcine Epidemic Diarrhea Vaccines market is dominated by players:

- Zoetis Inc.

- Merck Animal Health

- Elanco Animal Health

- Boehringer Ingelheim Animal Health

- Ceva Santé Animale

- Phibro Animal Health Corporation

- IDT Biologika GmbH

- Vaxxinova

- Qilu Animal Health Products Factory Co. Ltd.

- Green Cross Veterinary Products Co. Ltd.

- Nisseiken Co. Ltd.

- Komipharm International Co. Ltd.

- Harrisvaccines Inc.

- Others

The global Porcine Epidemic Diarrhea Vaccines market is segmented as follows:

By Type

- Live Vaccines

- Killed Vaccines

By Application

- Piglets

- Adult Pigs

By End-User

- Veterinary Hospitals

- Hog Production Farms

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Zoetis Inc.

- Merck Animal Health

- Elanco Animal Health

- Boehringer Ingelheim Animal Health

- Ceva Santé Animale

- Phibro Animal Health Corporation

- IDT Biologika GmbH

- Vaxxinova

- Qilu Animal Health Products Factory Co. Ltd.

- Green Cross Veterinary Products Co. Ltd.

- Nisseiken Co. Ltd.

- Komipharm International Co. Ltd.

- Harrisvaccines Inc.

- Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors