![]()

Search Market Research Report

Plastic Films and Sheets Market Size, Share Global Analysis Report, 2026-2034

Plastic Films and Sheets Market Size, Share, Growth Analysis Report By Product (LDPE/LLDPE, HDPE, PVC, BOPP, CPP, PA, and Others), By Application (Packaging, Non-Packaging), By End-User (Food, Consumer Goods, Medical & Pharmaceutical, Industrial, Agriculture, Construction, Healthcare, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

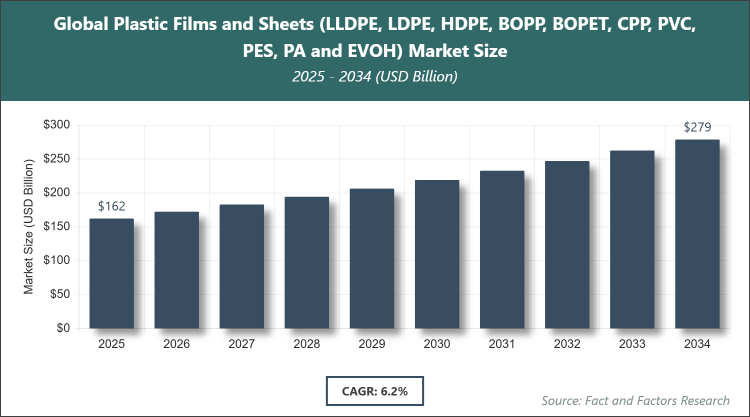

[235+ Pages Report] According to Facts & Factors, the global plastic films and sheets market size was estimated at USD 162.2 billion in 2025 and is expected to reach USD 279.5 billion by the end of 2034. The plastic films and sheets industry is anticipated to grow by a CAGR of 6.2% between 2026 and 2034. The plastic films and sheets Market is driven by increasing demand for sustainable packaging solutions across various industries.

Market Overview

Market Overview

The plastic films and sheets market encompasses a wide range of thin, flexible materials made from polymers, used primarily for packaging, protection, and insulation purposes. These materials are produced through processes like extrusion and are essential in applications where lightweight, durable, and versatile barriers are required, without incorporating specific quantitative data.

Key Insights

- As per the analysis shared by our research analyst, the global plastic films and sheets market is estimated to grow annually at a CAGR of around 6.2% over the forecast period (2026-2034).

- In terms of revenue, the global plastic films and sheets market size was valued at around USD 162.2 billion in 2025 and is projected to reach USD 279.5 billion by 2034.

- The market is driven by rising demand in the packaging and agriculture sectors.

- Based on the product, the LDPE/LLDPE segment dominated the market with a share of over 30% due to its versatility and cost-effectiveness in packaging applications.

- Based on the application, the packaging segment dominated with a share of over 80%, owing to its extensive use in food preservation and consumer goods protection.

- Based on the end-user, the food segment dominated with a share of around 40% because of the need for hygienic and flexible packaging solutions.

- Based on region, Asia Pacific dominated with a share of over 40% attributed to rapid industrialization and high manufacturing output in countries like China and India.

Growth Drivers

- Increasing Demand in Packaging Industry

The surge in e-commerce and processed food consumption has heightened the need for efficient packaging materials. Plastic films and sheets offer superior barrier properties against moisture and contaminants, making them ideal for extending shelf life and ensuring product safety.

This demand is further amplified by urbanization and changing consumer lifestyles, which favor convenient, ready-to-eat products. Innovations in multi-layer films enhance functionality, supporting market expansion across global supply chains.

Restraints

- Environmental Regulations and Sustainability Concerns

Strict policies on single-use plastics and bans in various regions pose significant hurdles. Governments are pushing for reduced plastic waste, impacting traditional film production.

This leads to higher compliance costs and shifts towards alternatives, potentially slowing growth in mature markets. Consumer awareness of plastic pollution adds pressure on manufacturers to reformulate products.

Opportunities

- Advancements in Biodegradable and Recyclable Films

Development of eco-friendly alternatives using bio-based polymers opens new avenues. These materials meet sustainability goals while maintaining performance, attracting environmentally conscious brands.

Investments in R&D for compostable films could capture premium segments in packaging and agriculture, fostering long-term growth amid global green initiatives.

Challenges

- Volatility in Raw Material Prices

Fluctuations in petroleum-based feedstock costs affect profitability. Supply chain disruptions from geopolitical events exacerbate this issue.

Manufacturers face challenges in maintaining stable pricing, which can deter investments and impact competitiveness in price-sensitive markets.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 162.2 Billion |

Projected Market Size in 2034 |

USD 279.5 Billion |

CAGR Growth Rate |

6.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Amcor PLC, Berry Global Group, Inc., SABIC, Toray Industries, Inc., Sealed Air Corporation, Uflex Limited, Toyobo Co., Ltd., Jindal Poly Films Limited, DuPont Teijin Films, British Polythene Industries PLC, and Others. |

Key Segment |

By Product, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The plastic films and sheets market is segmented by product, application, end-user, and region.

Based on Product Segment, the plastic films and sheets market is divided into LDPE/LLDPE, HDPE, PVC, BOPP, CPP, PA, and others. The LDPE/LLDPE segment is the most dominant, holding over 30% share, due to its excellent flexibility, low cost, and widespread use in flexible packaging, which drives market growth by enabling efficient production and distribution of goods. The BOPP segment is the second most dominant, with around 20% share, valued for its high clarity and strength in labels and wrappers, contributing to market expansion through enhanced aesthetic appeal and durability in consumer products.

Based on Application Segment, the plastic films and sheets market is divided into packaging and non-packaging. The packaging segment is the most dominant, capturing over 80% share, as it provides essential protection and preservation for various products, fueling market growth by supporting global trade and reducing spoilage. The non-packaging segment is the second most dominant, with about 20% share, utilized in agriculture for mulching and greenhouse covers, aiding market development by improving crop yields and resource efficiency.

Based on End-User Segment, the plastic films and sheets market is divided into food, consumer goods, medical & pharmaceutical, industrial, agriculture, construction, healthcare, and others. The food segment is the most dominant, with around 40% share, owing to its role in hygienic packaging that extends shelf life, driving the market by meeting rising demand for processed foods. The agriculture segment is the second most dominant, holding about 15% share, through applications like soil covers that enhance productivity, contributing to overall market growth via sustainable farming practices.

Recent Developments

- In August 2023, Amcor acquired Phoenix Flexibles to expand its capabilities in the Indian market, enhancing production capacity to meet growing demand for flexible packaging solutions.

- In May 2023, Berry Global Group partnered with ExxonMobil to incorporate certified-circular plastics into pet food packaging, advancing sustainability through advanced recycling technology.

- In December 2022, Amcor opened a new manufacturing plant in Huizhou, China, featuring advanced technology for high-performance films, boosting efficiency and market presence in Asia.

Regional Analysis

- Asia Pacific to Dominate the Global Market

The Asia Pacific region leads the global plastic films and sheets market, driven by robust manufacturing sectors and high consumption in packaging and agriculture. China stands out as the dominating country, with its massive production capabilities and export-oriented industries fueling demand. Rapid urbanization and economic growth further amplify the need for versatile plastic materials in daily applications.

North America follows as a key market, supported by advanced technological innovations and strong end-user industries like food and healthcare. The United States is the dominating country here, benefiting from a mature packaging sector and investments in sustainable films that align with regulatory standards.

Europe emphasizes sustainability, with growth in recyclable and bio-based films amid stringent environmental policies. Germany dominates in this region, leveraging its engineering expertise to develop high-quality films for automotive and medical uses, promoting eco-friendly practices.

Latin America shows potential through expanding agriculture and consumer goods sectors. Brazil is the dominating country, utilizing films for crop protection and packaging, driven by increasing exports and domestic consumption needs.

The Middle East & Africa region is emerging, with growth in construction and industrial applications. Saudi Arabia dominates, supported by its petrochemical industry that supplies raw materials, enabling cost-effective production and regional supply.

Competitive Analysis

The global plastic films and sheets market is dominated by players:

- Amcor PLC

- Berry Global Group, Inc.

- SABIC

- Toray Industries, Inc.

- Sealed Air Corporation

- Uflex Limited

- Toyobo Co., Ltd.

- Jindal Poly Films Limited

- DuPont Teijin Films

- British Polythene Industries PLC

The global plastic films and sheets market is segmented as follows:

By Product

- LDPE/LLDPE

- HDPE

- PVC

- BOPP

- CPP

- PA

- Others

By Application

- Packaging

- Non-Packaging

By End-User

- Food

- Consumer Goods

- Medical & Pharmaceutical

- Industrial

- Agriculture

- Construction

- Healthcare

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global plastic films and sheets market is dominated by players:

- Amcor PLC

- Berry Global Group, Inc.

- SABIC

- Toray Industries, Inc.

- Sealed Air Corporation

- Uflex Limited

- Toyobo Co., Ltd.

- Jindal Poly Films Limited

- DuPont Teijin Films

- British Polythene Industries PLC

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors