![]()

Search Market Research Report

Phosgene Market Size, Share Global Analysis Report, 2026-2034

Phosgene Market Size, Share, Growth Analysis Report By Derivative (Isocyanates, Chloroformates, Carbamoyl Chlorides, and Others), By Application (Agrochemicals, Pharmaceuticals, Polycarbonates, Fine Chemicals, Dyes, Specialty Chemicals, and Others), By End-User (Chemicals, Pharmaceuticals, Agriculture, Plastics, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

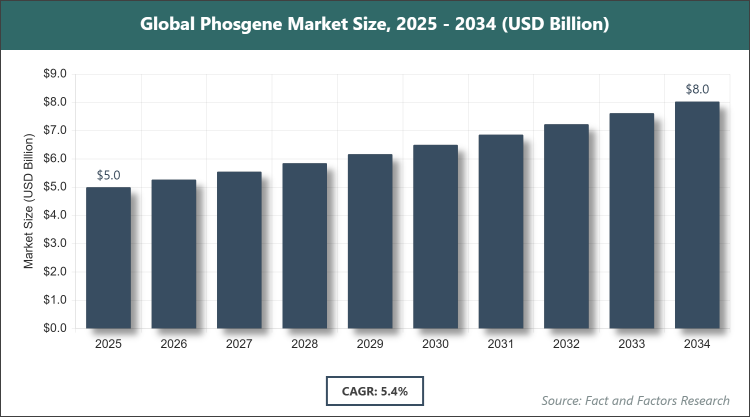

[228 Pages Report] According to Facts & Factors, the global phosgene market size was estimated at USD 5 billion in 2025 and is expected to reach USD 8 billion by the end of 2034. The Phosgene industry is anticipated to grow by a CAGR of 5.4% between 2026 and 2034. The Phosgene Market is driven by increasing demand for polyurethanes and agrochemicals.

Market Overview

Market Overview

The phosgene market involves the production, distribution, and utilization of phosgene, a colorless gas with the chemical formula COCl2, primarily used as an intermediate in the synthesis of various chemicals including isocyanates for polyurethane production, chloroformates for pharmaceuticals, and other derivatives essential in agrochemicals and specialty chemicals, serving industries that require high-performance materials for manufacturing processes while adhering to stringent safety and environmental regulations. This market engages key players in the chemical sector, focusing on efficient production methods to meet global demand for downstream products in construction, automotive, and agriculture, without direct end-consumer applications due to its toxic nature.

Key Insights

- As per the analysis shared by our research analyst, the Phosgene market is expected to grow at a CAGR of 5.4% during the forecast period of 2026-2034.

- In terms of revenue, the Phosgene market size was valued at about USD 5 billion in 2025 and is expected to reach USD 8 billion by 2034.

- The Phosgene market is driven by increasing demand for polyurethanes and agrochemicals.

- Based on the derivative, the isocyanates segment dominated the market with a share of 70% in 2025 due to its critical role in polyurethane production for foams, coatings, and adhesives in construction and automotive industries.

- Based on the application, the polycarbonates segment dominated the market with a share of 40% in 2025, owing to rising demand for durable plastics in electronics and automotive components.

- Based on the end-user, the chemicals segment dominated the market with a share of 50% in 2025, as it encompasses broad industrial applications requiring phosgene as a key intermediate.

- Asia Pacific dominated the market with a share of 40% in 2025 due to rapid industrialization and high demand from the polyurethane and agrochemical sectors in emerging economies.

Market Dynamics

Growth Drivers

- Rising Demand for Polyurethanes

The expanding construction and automotive industries are fueling the need for polyurethane foams and coatings derived from phosgene-based isocyanates, as these materials offer superior insulation and durability, driving market growth through increased production volumes in developing regions. This demand is further supported by urbanization trends that require advanced building materials for energy efficiency.

Additionally, innovations in polyurethane applications, such as flexible foams for furniture and rigid foams for refrigeration, are enhancing product performance, leading to broader adoption and sustained market expansion via technological advancements and supply chain optimizations.

- Growth in Agrochemical Sector

Increasing global food demand and the need for effective crop protection are boosting phosgene use in herbicide and pesticide synthesis, particularly in Asia where agricultural commercialization is rising, contributing to market growth through enhanced yield requirements. This is complemented by government initiatives promoting sustainable farming practices.

Moreover, the development of new agrochemical formulations with phosgene derivatives improves efficacy against pests, supporting long-term market growth by addressing challenges like climate change impacts on agriculture and fostering R&D investments.

- Expansion in Pharmaceuticals

Phosgene's role in synthesizing active pharmaceutical ingredients and intermediates is growing with rising healthcare needs, especially for drugs treating chronic diseases, propelling market demand through pharmaceutical industry expansions globally. This driver is amplified by aging populations in developed regions.

Furthermore, advancements in drug delivery systems utilizing phosgene-derived compounds are opening new avenues, driving market growth by enabling more efficient production processes and meeting regulatory standards for safety and efficacy.

Restraints

- Stringent Environmental Regulations

Strict regulations on phosgene handling and emissions due to its toxicity are increasing compliance costs for manufacturers, limiting market expansion in regions with rigorous environmental policies. This restraint poses challenges in operational scalability.

Ongoing monitoring and investment in safer alternatives further strain resources, potentially slowing growth as companies navigate complex legal frameworks to minimize environmental impact.

- Health and Safety Concerns

The hazardous nature of phosgene requires advanced safety measures, raising operational expenses and deterring new entrants, which constrains market growth in safety-sensitive industries. This issue is exacerbated by past incidents highlighting risks.

Efforts to implement robust safety protocols and training programs add to costs, impacting profitability and requiring continuous improvements to maintain market viability.

Opportunities

- Technological Advancements in Production

Innovations in safer phosgene synthesis methods, like on-site generation, offer opportunities to reduce risks and costs, attracting investments and expanding market reach in regulated environments. This can lead to more efficient processes.

Such developments enable integration with green chemistry principles, opening doors for sustainable products and partnerships that enhance competitive positioning.

- Emerging Markets in Asia Pacific

Rapid industrialization in countries like China and India presents opportunities for phosgene demand in manufacturing, supported by favorable policies and infrastructure growth, fostering market penetration. This region holds potential for high-volume applications.

Leveraging local resources and collaborations can accelerate adoption, driving revenue through tailored solutions for regional needs.

Challenges

- Supply Chain Disruptions

Volatility in raw material supplies, such as carbon monoxide and chlorine, poses challenges to consistent phosgene production, affecting market stability amid global trade fluctuations. This requires diversified sourcing strategies.

Geopolitical tensions and logistic issues further complicate supply chains, demanding adaptive measures to ensure uninterrupted operations.

- Competition from Alternatives

The development of phosgene-free processes in chemical synthesis challenges traditional market reliance, pushing companies to innovate or risk share loss in eco-conscious sectors. This necessitates R&D focus.

Balancing cost-effectiveness with environmental benefits remains key to overcoming this challenge and retaining market position.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 5 Billion |

Projected Market Size in 2034 |

USD 8 Billion |

CAGR Growth Rate |

5.4% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Wanhua Chemical Group Co. Ltd., VanDeMark Chemical Inc., Vertellus Holdings LLC, Atul Ltd., Paushak Ltd., Gujarat Narmada Valley Fertilizers & Chemicals Limited, Synthesia a.s., Shandong Tianan Chemicals Co. Ltd., Altivia, Tokyo Chemical Industry Co. Ltd., Lanxess, and Others. |

Key Segment |

By Derivative, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Phosgene market is segmented by derivative, application, end-user, and region.

Based on Derivative Segment, the phosgene market is divided into isocyanates, chloroformates, carbamoyl chlorides, and others. The most dominant segment is isocyanates, commanding the largest share because of its extensive use in producing methylene diphenyl diisocyanate (MDI) and toluene diisocyanate (TDI) for polyurethane foams essential in construction and automotive sectors, driving the market by supporting growth in insulation and lightweight materials that enhance energy efficiency and vehicle performance; the second most dominant is chloroformates, which gains prominence in pharmaceutical intermediates and agrochemicals, contributing to market expansion through applications in drug synthesis and crop protection that address global health and food security needs.

Based on Application Segment, the phosgene market is divided into agrochemicals, pharmaceuticals, polycarbonates, fine chemicals, dyes, specialty chemicals, and others. The most dominant segment is polycarbonates, leading due to high demand for transparent and impact-resistant plastics in electronics, automotive, and construction, propelling market growth via innovations in lightweight components that improve fuel efficiency and durability; the second most dominant is agrochemicals, sustaining demand through its role in herbicide production amid rising agricultural needs, aiding market drive by enhancing crop yields and supporting food production in densely populated regions.

Based on End-User Segment, the phosgene market is divided into chemicals, pharmaceuticals, agriculture, plastics, and others. The most dominant segment is chemicals, dominating owing to broad utilization as an intermediate in diverse synthesis processes, boosting market growth in industrial applications requiring versatile building blocks; the second most dominant is plastics, which supports expansion by facilitating polycarbonate and polyurethane production for consumer goods and packaging, helping to meet evolving material demands in modern manufacturing.

Recent Developments

- In May 2022, BASF SE launched Phosgene (COCl2) A1, aiming to enhance production efficiency and safety in chemical synthesis applications.

- In November 2022, Huntsman Corporation announced the sale of its Textile Effects division to Archroma, focusing resources on core phosgene-related polyurethane businesses.

- In October 2022, the Department of Chemical Technology Industry and Bioengineering Technologies launched production of polyurethanes as part of the Ural Interregional Research and Education Centre, introducing green polyurethane without harmful substances.

- In April 2021, Merck invested USD 22.9 million to expand R&D and manufacturing capabilities in Shizuoka, Japan, advancing electronic materials potentially linked to phosgene derivatives.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific commands the phosgene market with China as the dominating country, where rapid industrialization and a booming polyurethane industry for construction and automotive sectors drive demand, bolstered by extensive manufacturing infrastructure that supports large-scale production and export, while government policies promoting chemical sector growth further enhance its position through investments in technology and capacity expansion to meet both domestic and international needs.

North America holds a significant share with the United States dominating, fueled by advanced pharmaceutical and specialty chemical industries utilizing phosgene for drug intermediates and high-performance materials, supported by robust R&D ecosystems and stringent safety standards that ensure reliable supply chains, alongside growing demand in agrochemicals for sustainable farming practices in vast agricultural lands.

Europe follows closely, led by Germany, where a strong focus on automotive and construction applications for polycarbonates and polyurethanes propels the market, integrated with environmental regulations driving innovation in safer production methods, creating a competitive edge through high-quality exports and collaborations in chemical engineering.

Latin America is emerging, with Brazil as the key country, driven by expanding agrochemical needs to support its large agricultural sector, combined with increasing investments in chemical manufacturing that leverage natural resources, fostering growth in phosgene derivatives for pesticides and plastics amid economic development.

The Middle East & Africa region is growing, dominated by South Africa, where mining and industrial applications require specialty chemicals derived from phosgene, aided by regional trade agreements and infrastructure projects that boost demand for construction materials, while efforts to diversify economies include chemical production enhancements.

Competitive Analysis

The global Phosgene market is dominated by players:

- BASF SE

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- Wanhua Chemical Group Co. Ltd.

- VanDeMark Chemical Inc.

- Vertellus Holdings LLC

- Atul Ltd.

- Paushak Ltd.

- Gujarat Narmada Valley Fertilizers & Chemicals Limited

- Synthesia a.s.

- Shandong Tianan Chemicals Co. Ltd.

- Altivia

- Tokyo Chemical Industry Co. Ltd.

- Lanxess

The global Phosgene market is segmented as follows:

By Derivative

- Isocyanates

- Chloroformates

- Carbamoyl Chlorides

- Others

By Application

- Agrochemicals

- Pharmaceuticals

- Polycarbonates

- Fine Chemicals

- Dyes

- Specialty Chemicals

- Others

By End-User

- Chemicals

- Pharmaceuticals

- Agriculture

- Plastics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Phosgene market is dominated by players:

BASF SE

Covestro AG

Dow Inc.

Huntsman Corporation

Wanhua Chemical Group Co. Ltd.

VanDeMark Chemical Inc.

Vertellus Holdings LLC

Atul Ltd.

Paushak Ltd.

Gujarat Narmada Valley Fertilizers & Chemicals Limited

Synthesia a.s.

Shandong Tianan Chemicals Co. Ltd.

Altivia

Tokyo Chemical Industry Co. Ltd.

Lanxess

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors