![]()

Search Market Research Report

Paper and Plastic Straws Market Size, Share Global Analysis Report, 2026-2034

Paper and Plastic Straws Market Size, Share, Growth Analysis Report By Type (Paper Straws and Plastic Straws), By Application (Foodservice and Household), By End-User (Commercial and Residential), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

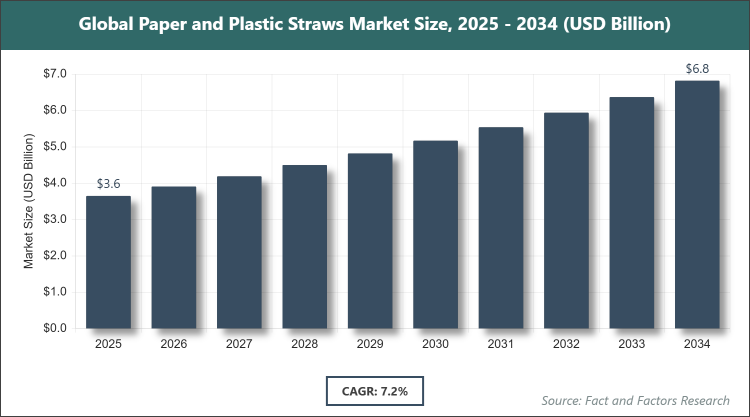

[226 Pages Report] According to Facts & Factors, the global Paper and Plastic Straws market size was estimated at USD 3.65 billion in 2025 and is expected to reach USD 6.85 billion by the end of 2034. The Paper and Plastic Straws industry is anticipated to grow by a CAGR of 7.2% between 2026 and 2034. The Paper and Plastic Straws Market is driven by stringent government regulations banning single-use plastic straws, coupled with rising consumer preference for sustainable and biodegradable alternatives.

Market Overview

Market Overview

The Paper and Plastic Straws market covers the manufacturing, distribution, and consumption of single-use drinking straws produced from either paper-based materials or conventional petroleum-derived plastics. Paper straws are typically made from food-grade paperboard or kraft paper, often coated for improved moisture resistance, while plastic straws are extruded from polypropylene or polystyrene resins, offering flexibility and durability. These products are essential accessories in the foodservice industry for beverages, with additional applications in household and retail settings, where they provide convenience for on-the-go consumption. The market reflects a transitional phase driven by environmental concerns, with innovation focused on enhancing the performance of paper variants to match the functional attributes traditionally associated with plastic while meeting compostability and recyclability standards.

Key Insights

- As per the analysis shared by our research analyst, the Paper and Plastic Straws market is estimated to grow annually at a CAGR of around 7.2% over the forecast period (2026-2034).

- In terms of revenue, the Paper and Plastic Straws market size was valued at around USD 3.65 billion in 2025 and is projected to reach USD 6.85 billion by 2034.

- The Paper and Plastic Straws Market is driven by global bans on single-use plastics and demand for eco-friendly alternatives.

- Based on the Type, the Paper Straws segment dominated the market in 2025 with a share of 58% due to widespread regulatory restrictions on plastics and a strong consumer shift toward biodegradable options.

- Based on the Application, the Foodservice segment dominated the market in 2025 with a share of 69%, owing to massive volume consumption in quick-service restaurants, cafes, and beverage outlets requiring high-volume disposable accessories.

- Based on the End-User, the Commercial segment dominated the market in 2025 with a share of 74% because of extensive adoption by restaurants, hotels, and catering services prioritizing cost-effective and compliant single-use solutions.

- Asia Pacific dominated the global Paper and Plastic Straws market in 2025 with a share of 46%, attributed to the region's enormous foodservice industry, large population base, and rapid urbanization driving beverage consumption across both paper and plastic formats.

Growth Drivers

- Regulatory Bans and Environmental Awareness

Governments worldwide continue to implement outright bans or taxes on single-use plastic straws, compelling foodservice operators and retailers to transition toward paper alternatives and accelerating overall market momentum.

Heightened consumer consciousness regarding ocean plastic pollution and corporate sustainability commitments by major beverage chains have created a strong pull for certified eco-friendly straw options, boosting innovation and adoption rates.

Restraints

- Performance Limitations of Paper Straws

Paper straws often soften or lose structural integrity when exposed to liquids for extended periods, leading to customer dissatisfaction and slower replacement of plastic in certain high-volume applications.

Higher production costs associated with quality paper straws compared to conventional plastic variants create pricing pressure for budget-conscious foodservice operators in price-sensitive markets.

Opportunities

- Innovation in Durable and Functional Paper Straws

Advancements in coating technologies, multi-layer designs, and plant-based reinforcements are improving the durability and user experience of paper straws, opening doors for premium and specialty applications.

Expansion of e-commerce and ready-to-drink beverage delivery services is generating new demand channels for individually wrapped and branded straws in both paper and hybrid formats.

Challenges

- Supply Chain and Raw Material Volatility

Fluctuations in pulp prices and competition for sustainable paper sources can disrupt consistent supply, particularly as demand for food-grade paperboard surges globally.

Fragmented regulatory landscapes across regions create complexity for manufacturers attempting to standardize products for international distribution while complying with varying compostability and labeling requirements.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 3.65 Billion |

Projected Market Size in 2034 |

USD 6.85 Billion |

CAGR Growth Rate |

7.2% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Huhtamaki Oyj, Hoffmaster Group Inc., Transcend Packaging Ltd., BioPak Pty Ltd., Footprint, Dart Container Corporation, Pactiv Evergreen Inc., and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Paper and Plastic Straws market is segmented by type, application, end-user, and region.

Based on Type Segment, the Paper and Plastic Straws market is divided into paper straws and plastic straws. The most dominant segment is Paper Straws, followed by Plastic Straws. Paper Straws dominate because of accelerating global plastic bans, superior environmental credentials, and improving technical performance that meets foodservice durability needs, which together drive higher prescription and procurement volumes while encouraging manufacturers to invest in next-generation coated and reinforced designs that further expand market share and revenue growth.

Based on Application Segment, the Paper and Plastic Straws market is divided into Foodservice and Household. The most dominant segment is Foodservice, followed by Household. Foodservice leads the segment due to the enormous daily volume of beverages served in restaurants, cafes, and quick-service outlets where straws are standard accompaniments, generating consistent high-volume demand that stimulates bulk procurement and innovation in cost-efficient, compliant formats while propelling overall market expansion through large-scale contracts and supply agreements.

Based on End-User Segment, the Paper and Plastic Straws market is divided into Commercial and Residential. The most dominant segment is Commercial, followed by Residential. Commercial dominates because restaurants, hotels, and catering businesses require reliable, high-volume disposable straw supplies that comply with local regulations and brand sustainability goals, creating steady procurement cycles and driving market growth through economies of scale in manufacturing and distribution tailored to B2B requirements.

Recent Developments

- In January 2025, Huhtamaki Oyj launched a new generation of coated paper straws with enhanced liquid resistance and faster biodegradation, targeting major quick-service restaurant chains across Europe and North America.

- In June 2025, BioPak expanded its manufacturing facility in Australia to double production capacity of printed and custom-branded paper straws in response to rising demand from the Asia-Pacific foodservice sector.

- In March 2025, Hoffmaster Group Inc. (Aardvark Straws) introduced fully compostable paper straws certified for marine environments, securing contracts with several large U.S. coastal restaurant groups.

- In October 2025, Transcend Packaging Ltd. partnered with a leading European beverage brand to supply 100% recycled-content paper straws as part of the brand’s net-zero packaging initiative.

- In November 2025, several Southeast Asian countries announced phased plastic straw bans effective 2026, prompting local converters to accelerate conversion lines to paper-based production.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific leads the Paper and Plastic Straws market through its massive foodservice sector, rapid urbanization, and expanding quick-service restaurant chains that generate enormous daily demand for drinking straws across both paper and plastic formats. The region benefits from large-scale manufacturing capabilities, cost-competitive raw material sourcing, and a growing middle class that drives beverage consumption in both on-premise and delivery channels. Government initiatives promoting circular economy principles and selective plastic restrictions in key countries further accelerate the shift toward paper while maintaining overall volume growth. China dominates within Asia Pacific with its unparalleled scale of food and beverage production, dense network of street vendors and restaurants, and position as a global manufacturing hub that supplies both domestic needs and international export markets for affordable straw solutions.

North America holds a strong position in the Paper and Plastic Straws market supported by early and stringent plastic bans in multiple states and provinces, high consumer environmental awareness, and leadership of major restaurant chains in adopting sustainable alternatives. The region features sophisticated distribution networks and strong corporate sustainability reporting that favors certified paper products. The United States dominates within North America owing to its vast quick-service restaurant industry, proactive regulatory environment at city and state levels, and presence of innovative paper straw manufacturers that continuously improve product performance to meet demanding foodservice standards.

Europe exhibits mature and regulation-driven growth in the Paper and Plastic Straws market fueled by comprehensive EU single-use plastics directives, high consumer preference for eco-labeled products, and widespread adoption of paper straws in hospitality and retail settings. The region emphasizes circular economy principles and extended producer responsibility schemes that favor biodegradable materials. Germany dominates within Europe through its advanced packaging technology sector, strict enforcement of plastic reduction targets, and central role in supplying high-quality paper straws to neighboring markets while maintaining leadership in sustainable material innovation.

Latin America is experiencing accelerating uptake in the Paper and Plastic Straws market driven by improving regulatory frameworks in major economies, rising middle-class consumption of packaged beverages, and increasing participation of international foodservice brands that bring sustainability standards. Growing e-commerce food delivery further expands straw requirements. Brazil dominates the region with its large population, vibrant foodservice culture, and expanding organized retail sector that increasingly incorporates paper-based disposables to align with global brand expectations and local environmental goals.

The Middle East & Africa region shows promising early-stage development in the Paper and Plastic Straws market supported by tourism-driven hospitality growth, urban modernization, and selective adoption of sustainability practices in premium foodservice outlets. Rising awareness among younger consumers and international hotel chains operating in the region create demand for compliant straw options. The United Arab Emirates leads within the region through its world-class hospitality infrastructure, government vision for sustainable tourism, and role as a regional hub that introduces advanced paper straw solutions to serve both local and expatriate markets.

Competitive Analysis

The global Paper and Plastic Straws market is dominated by players:

- Huhtamaki Oyj

- Hoffmaster Group Inc. (Aardvark Straws)

- Transcend Packaging Ltd.

- BioPak Pty Ltd.

- Footprint

- Fuling Global Inc.

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Novolex

- Nippon Paper Industries Co., Ltd.

The global Paper and Plastic Straws market is segmented as follows:

By Type

- Paper Straws

- Plastic Straws

By Application

- Foodservice

- Household

- Others

By End-User

- Commercial

- Residential

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Huhtamaki Oyj

- Hoffmaster Group Inc. (Aardvark Straws)

- Transcend Packaging Ltd.

- BioPak Pty Ltd.

- Footprint

- Fuling Global Inc.

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Novolex

- Nippon Paper Industries Co., Ltd.

- Huhtamaki Oyj

- Hoffmaster Group Inc. (Aardvark Straws)

- Transcend Packaging Ltd.

- BioPak Pty Ltd.

- Footprint

- Fuling Global Inc.

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Novolex

- Nippon Paper Industries Co., Ltd.

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors