![]()

Search Market Research Report

Mexico Water and Wastewater Treatment Chemicals Market Size, Share Global Analysis Report, 2026-2034

Mexico Water and Wastewater Treatment Chemicals Market Size, Share, Growth Analysis Report By Product Type (Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Softeners, Anti-Foaming Agents, Chelating Agents, and Others), By Application (Raw Water Treatment, Water Desalination, Cooling, Boiler, Effluent Water Treatment, and Others), By End-User (Municipal, Oil & Gas, Power, Mining, Chemical, Food & Beverage, Pulp & Paper, and Others), and By Region - Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

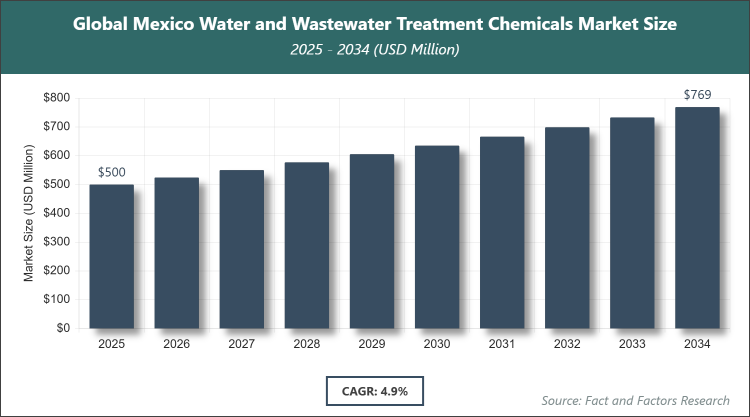

[220+ Pages Report] According to Facts & Factors, the Mexico Water and Wastewater Treatment Chemicals market size was estimated at USD 500 million in 2025 and is expected to reach USD 800 million by the end of 2034. The Water and Wastewater Treatment Chemicals industry is anticipated to grow by a CAGR of 4.9% between 2026 and 2034. The Water and Wastewater Treatment Chemicals Market is driven by increasing industrialization, urbanization, and stringent environmental regulations.

Market Overview

Market Overview

The Mexico Water and Wastewater Treatment Chemicals Market encompasses the production, distribution, and application of various chemical agents used in treating water and wastewater to make it safe for consumption, industrial use, or environmental discharge. These chemicals play a crucial role in processes such as coagulation, flocculation, disinfection, pH adjustment, and corrosion control, ensuring compliance with quality standards and protecting public health and ecosystems.

Key Insights

- As per the analysis shared by our research analyst, the Mexico Water and Wastewater Treatment Chemicals market is estimated to grow annually at a CAGR of around 4.9% over the forecast period (2026-2034).

- In terms of revenue, the Mexico Water and Wastewater Treatment Chemicals market was valued at USD 500 million in 2025 and is expected to reach USD 800 million by 2034.

- The market is driven by rapid industrialization, urbanization, and government regulations promoting sustainable water management.

- Based on the product type, the coagulants & flocculants segment dominated with a 35% share.

- It is dominated due to their essential role in removing suspended solids and impurities from water, which is critical for both municipal and industrial treatment processes, enhancing efficiency and compliance with water quality standards.

- Based on the application, the effluent water treatment segment dominated with a 30% share.

- It is dominated because of the increasing focus on wastewater recycling and stringent discharge regulations, driving demand for chemicals that effectively treat industrial effluents to prevent environmental pollution.

- Based on the end-user, the municipal segment dominated with a 40% share.

- It is dominated owing to the high demand for clean drinking water in growing urban populations and government investments in public water infrastructure.

- The Central Mexico region dominated with a 45% share due to its concentration of major cities, industrial hubs, and higher population density, leading to greater water consumption and treatment needs.

Growth Drivers

- Rapid Industrialization and Urbanization

Rapid industrialization in Mexico has led to increased water usage in sectors like manufacturing, mining, and energy, necessitating advanced treatment chemicals to manage wastewater and ensure sustainable operations. This growth is further amplified by urbanization, which strains existing water infrastructure and drives investments in treatment solutions to address scarcity and pollution issues.

As industries expand, the demand for efficient water recycling and purification rises, promoting the adoption of specialized chemicals that enhance treatment processes and comply with environmental standards, ultimately supporting long-term economic development.

- Stringent Government Regulations

Government policies in Mexico, including water quality standards and wastewater discharge controls, compel industries and municipalities to utilize treatment chemicals for compliance. Initiatives like the draft General Water Law emphasize sustainable management, boosting market growth through enforced environmental protections.

These regulations encourage innovation in chemical formulations, leading to more effective and eco-friendly solutions that reduce pollution and promote water reuse, fostering a robust market environment.

Restraints

- High Costs of Chemicals and Infrastructure

The elevated costs associated with procuring and implementing water treatment chemicals pose a significant barrier, particularly for small-scale industries and municipalities with limited budgets. This financial strain can delay adoption and limit market penetration in less developed areas.

Additionally, the need for substantial infrastructure investments to integrate these chemicals effectively adds to the overall expense, potentially hindering growth in regions with economic constraints.

- Environmental Concerns Over Chemical Usage

Concerns regarding the environmental impact of certain treatment chemicals, such as potential toxicity and residue accumulation, restrain market expansion. Stricter scrutiny on chemical safety may lead to regulatory hurdles and increased R&D costs for greener alternatives.

This restraint encourages a shift towards sustainable options but can slow down the adoption of traditional chemicals, affecting short-term market dynamics.

Opportunities

- Technological Advancements in Eco-Friendly Formulations

Innovations in biodegradable and low-toxicity treatment chemicals present opportunities for market players to cater to environmentally conscious consumers and comply with evolving regulations. These advancements can open new segments focused on sustainable water management.

By investing in R&D, companies can differentiate their products, gaining a competitive edge and expanding into emerging applications like advanced desalination and recycling.

- Investments in Water Infrastructure

Government and private sector investments in upgrading water treatment facilities create opportunities for increased chemical demand. Projects aimed at addressing water scarcity in arid regions can drive long-term market growth.

These investments facilitate the integration of modern treatment technologies, enhancing efficiency and creating avenues for chemical suppliers to partner on large-scale initiatives.

Challenges

- Water Scarcity and Resource Management

Mexico's ongoing water scarcity issues challenge the effective deployment of treatment chemicals, as limited resources may prioritize conservation over extensive treatment processes. This can impact the scalability of chemical applications.

Addressing this requires integrated strategies that combine chemical treatments with conservation efforts, but regional disparities in water availability complicate uniform market growth.

- Supply Chain Disruptions

Supply chain vulnerabilities, including raw material shortages and logistical issues, pose challenges to the consistent availability of treatment chemicals. This can lead to price fluctuations and delays in project implementations.

Mitigating these requires diversified sourcing and local production enhancements, but persistent disruptions may affect market stability in the short term.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 500 Million |

Projected Market Size in 2034 |

USD 800 Million |

CAGR Growth Rate |

4.9% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Ecolab, BASF SE, Kemira Oyj, Solenis, SNF Group, Buckman, Baker Hughes, IDE Water Technologies, Cortec Corporation, and Others. |

Key Segment |

By Product Type, By Application, By End-User, and By Region |

Major Regions Covered |

Northern Mexico, Central Mexico, Southern Mexico, and Others |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Mexico Water and Wastewater Treatment Chemicals market is segmented by product type, application, end-user, and region.

Based on Product Type Segment, the Mexico Water and Wastewater Treatment Chemicals market is divided into coagulants & flocculants, corrosion & scale inhibitors, biocides & disinfectants, pH adjusters & softeners, anti-foaming agents, chelating agents, and others. The most dominant segment is coagulants & flocculants, holding a significant share due to their critical function in aggregating particles for easy removal, which is fundamental in initial treatment stages across various applications. The second most dominant is corrosion & scale inhibitors, which prevent equipment degradation and maintain system efficiency, driving the market by reducing maintenance costs and extending infrastructure lifespan in industrial settings.

Based on Application Segment, the Mexico Water and Wastewater Treatment Chemicals market is divided into raw water treatment, water desalination, cooling, boiler, effluent water treatment, and others. The most dominant segment is effluent water treatment, as it addresses the growing need to treat industrial and municipal wastewater before discharge, ensuring environmental compliance and resource recovery. The second most dominant is cooling, which supports industrial processes by preventing scaling and corrosion in cooling systems, thereby enhancing operational efficiency and contributing to overall market expansion through sustained demand from manufacturing sectors.

Based on End-User Segment, the Mexico Water and Wastewater Treatment Chemicals market is divided into municipal, oil & gas, power, mining, chemical, food & beverage, pulp & paper, and others. The most dominant segment is municipal, driven by the essential need for safe drinking water and sanitation in populous urban areas, supported by government funding. The second most dominant is oil & gas, where chemicals are vital for managing produced water and maintaining equipment integrity, fueling market growth amid Mexico's energy sector activities.

Recent Developments

- In 2024, Crown Electrokinetics Corp. announced plans to build and co-own a reverse osmosis water treatment plant in Cabo San Lucas, Mexico, in partnership with 529 Capital. This initiative aims to desalinate water and address local scarcity issues, with construction set to begin in summer 2025 and operations commencing in 2026, highlighting a focus on sustainable water solutions.

- In 2024, Tetradom presented its innovative chemical-free and electricity-free water treatment technology at Aquatech Mexico. Utilizing ultra-fine oscillation waves, this system prevents scale formation, microbial growth, and rust in industrial applications, offering an eco-friendly alternative that aligns with growing demands for sustainable treatment methods.

Regional Analysis

- Central Mexico to dominate the market

Central Mexico, encompassing major urban centers like Mexico City, dominates the market due to its high population density and extensive industrial activities, which generate substantial demand for water treatment chemicals to manage supply and wastewater. The region's advanced infrastructure and government focus on pollution control further bolster its leading position, with key industries relying on efficient treatment to sustain operations.

Northern Mexico experiences robust growth driven by its manufacturing and mining sectors, particularly in border states like Baja California and Nuevo Leon, where cross-border trade amplifies water usage. Proximity to the U.S. market encourages investments in treatment technologies to meet international standards, supporting regional expansion through enhanced industrial water recycling.

Southern Mexico, including areas like Chiapas and Oaxaca, shows potential amid agricultural and tourism-driven needs, though challenged by infrastructural limitations. Increasing awareness of water quality in rural communities and eco-tourism sites drives demand for chemicals, with opportunities arising from federal programs aimed at improving access to clean water.

Competitive Analysis

The Mexico Water and Wastewater Treatment Chemicals market is dominated by players:

- Ecolab

- BASF SE

- Kemira Oyj

- Solenis

- SNF Group

- Buckman

- Baker Hughes

- IDE Water Technologies

- Cortec Corporation

- and Others

The Mexico Water and Wastewater Treatment Chemicals market is segmented as follows:

By Product Type

- Coagulants & Flocculants

- Corrosion & Scale Inhibitors

- Biocides & Disinfectants

- pH Adjusters & Softeners

- Anti-Foaming Agents

- Chelating Agents

- Others

By Application

- Raw Water Treatment

- Water Desalination

- Cooling

- Boiler

- Effluent Water Treatment

- Others

By End-User

- Municipal

- Oil & Gas

- Power

- Mining

- Chemical

- Food & Beverage

- Pulp & Paper

- Others

By Region

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

Industry Major Market Players

The Mexico Water and Wastewater Treatment Chemicals market is dominated by players:

- Ecolab

- BASF SE

- Kemira Oyj

- Solenis

- SNF Group

- Buckman

- Baker Hughes

- IDE Water Technologies

- Cortec Corporation

- and Others

Frequently Asked Questions

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors