![]()

Search Market Research Report

Stainless Steel Pipes and Tubes Market Size, Share Global Analysis Report, 2026-2034

Stainless Steel Pipes and Tubes Market Size, Share, Growth Analysis Report By Product Type (Seamless Pipes and Tubes, Welded Pipes and Tubes, and Others), By Application (Oil and Gas, Chemical Industry, Automotive, Construction, Food Industry, Power Industry, Water Treatment, Pharmaceutical, and Others), By End-Use Industry (Energy & Power, Construction & Infrastructure, Automotive & Transportation, Chemical & Petrochemical, Healthcare & Pharmaceuticals, Food & Beverage, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

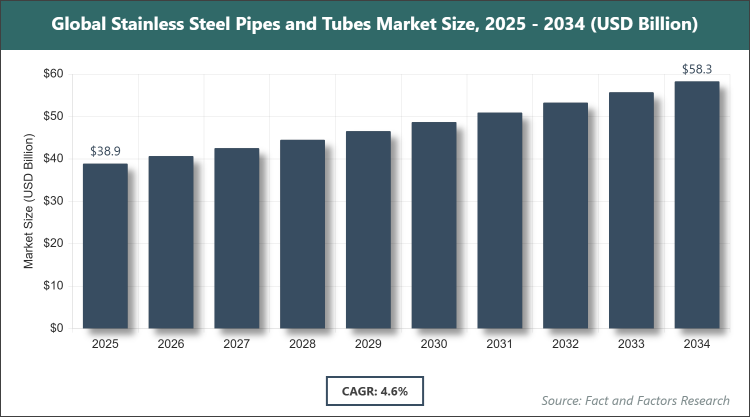

[245+ Pages Report] According to Facts & Factors, the global stainless steel pipes and tubes market size was estimated at USD 38.9 billion in 2025 and is expected to reach USD 60.1 billion by the end of 2034. The stainless steel pipes and tubes industry is anticipated to grow by a CAGR of 4.6% between 2026 and 2034. The stainless steel pipes and tubes Market is driven by increasing demand from oil & gas and construction sectors.

Market Overview

Market Overview

Stainless steel pipes and tubes are essential components in various industries, crafted from stainless steel alloys that offer exceptional corrosion resistance, durability, and strength. These products are used for transporting fluids and gases in harsh environments where reliability is paramount.

Key Insights

- As per the analysis shared by our research analyst, the global stainless steel pipes and tubes market is estimated to grow annually at a CAGR of around 4.6% over the forecast period (2026-2034).

- In terms of revenue, the global stainless steel pipes and tubes market size was valued at around USD 38.9 Billion in 2025 and is projected to reach USD 60.1 Billion, by 2034.

- The market is driven by rising industrialization and infrastructure development.

- Based on the product type, the seamless segment dominated with 60% share, due to its superior strength and suitability for high-pressure applications.

- Based on the application, oil and gas dominated with 30% share, due to the need for corrosion-resistant materials in exploration and transportation.

- Based on the end-use industry, energy & power dominated with 35% share, due to extensive use in power plants and renewable energy infrastructure.

- Asia Pacific dominated with 60% share, due to rapid economic growth and industrialization in the region.

Growth Drivers

- Increasing Demand from Oil & Gas Sector

The oil and gas industry is a major consumer of stainless steel pipes and tubes, driven by the need for materials that can withstand extreme conditions such as high pressure, corrosive environments, and temperature variations. As global energy demands rise, exploration activities in offshore and deep-water regions are expanding, necessitating reliable piping solutions that minimize leaks and ensure safety.

This trend is further amplified by investments in pipeline infrastructure and refinery expansions in emerging economies, where stainless steel's longevity reduces maintenance costs and downtime. Technological advancements in extraction methods, like hydraulic fracturing, also boost the requirement for high-performance tubes, supporting overall market growth.

Restraints

- Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials, such as nickel and chromium, pose a significant challenge to the stainless steel pipes and tubes market. These price swings are influenced by geopolitical tensions, supply chain disruptions, and varying demand from other industries, leading to increased production costs for manufacturers.

As a result, profit margins can be squeezed, and end-users may seek cheaper alternatives like carbon steel or plastic pipes for non-critical applications. This restraint is particularly acute in price-sensitive markets, where cost predictability is crucial for long-term projects, potentially slowing adoption in certain sectors.

Opportunities

- Expansion in Renewable Energy Applications

The shift towards renewable energy sources, such as solar, wind, and geothermal, presents new opportunities for stainless steel pipes and tubes due to their resistance to environmental degradation and ability to handle thermal stresses. In solar thermal plants and geothermal systems, these products are ideal for fluid transport and heat exchange, aligning with global sustainability goals.

Government incentives and investments in green infrastructure are accelerating this trend, opening avenues for innovation in specialized alloys and designs. This opportunity allows manufacturers to diversify beyond traditional sectors, tapping into the growing eco-friendly market and enhancing long-term revenue streams.

Challenges

- Competition from Alternative Materials

The market faces stiff competition from substitute materials like PVC, HDPE, and composite pipes, which offer lower initial costs and easier installation in certain applications. These alternatives are gaining traction in water treatment and construction sectors where corrosion is less severe, challenging the dominance of stainless steel.

Additionally, advancements in coating technologies for carbon steel pipes provide similar corrosion resistance at reduced prices, further intensifying competition. Overcoming this requires continuous innovation in stainless steel formulations to emphasize superior lifecycle value and performance in demanding environments.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 38.9 Billion |

Projected Market Size in 2034 |

USD 60.1 Billion |

CAGR Growth Rate |

4.6% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

ArcelorMittal, ThyssenKrupp, Tenaris, Pohang Iron & Steel (POSCO), Baosteel, CENTRAVIS, Tubacex, Nippon Steel Corporation, Outokumpu, Sandvik, Tata Steel, JFE Steel Corporation, AK Steel, Jiuli Group, Mannesmann Stainless Tubes, and Others. |

Key Segment |

By Product Type, By Application, By End-Use Industry, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The stainless steel pipes and tubes market is segmented by type, application, end-user, and region.

Based on Product Type Segment, the stainless steel pipes and tubes market is divided into seamless pipes and tubes, welded pipes and tubes, and others. The seamless segment is the most dominant, holding approximately 60% market share, primarily because of its enhanced mechanical properties and reliability in high-pressure and high-temperature scenarios, which are critical in industries like oil and gas and power generation. This dominance drives the market by enabling safer and more efficient operations in demanding applications, reducing failure risks and operational costs. The welded segment is the second most dominant, with around 35% share, owing to its cost-effectiveness and versatility for low to medium-pressure uses in construction and automotive, contributing to market growth through broader accessibility and customization options.

Based on Application Segment, the stainless steel pipes and tubes market is divided into oil and gas, chemical industry, automotive, construction, food industry, power industry, water treatment, pharmaceutical, and others. The oil and gas segment is the most dominant, capturing about 30% market share, due to the material's exceptional corrosion resistance and durability in harsh extraction and transportation environments, which helps prevent leaks and extends asset life, thereby driving market expansion through increased adoption in offshore projects. The chemical industry is the second most dominant, with roughly 20% share, as stainless steel's chemical inertness ensures safe handling of aggressive substances, supporting market growth by facilitating efficient processes and compliance with safety standards.

Based on End-Use Industry Segment, the stainless steel pipes and tubes market is divided into energy & power, construction & infrastructure, automotive & transportation, chemical & petrochemical, healthcare & pharmaceuticals, food & beverage, and others. The energy & power segment is the most dominant, accounting for around 35% market share, driven by the need for robust materials in power plants and renewable energy setups that withstand extreme conditions, propelling market growth via enhanced efficiency and reliability in energy production. The construction & infrastructure segment is the second most dominant, with approximately 25% share, because of stainless steel's aesthetic appeal and structural integrity in building projects, aiding market advancement through sustainable and long-lasting infrastructure developments.

Recent Developments

- In November 2025, Metinvest Group acquired ArcelorMittal Tubular Products Iași, a Romanian pipe manufacturing plant, to expand its production capacity and strengthen its presence in the European market.

- In October 2025, Nippon Steel merged its three pipe subsidiaries into Nippon Steel Finetube Co., Ltd., aiming to streamline operations and improve efficiency amid shifting automotive demands.

- In October 2024, Tubacex S.A. secured a USD 69 million contract from Petrobras for CRA OCTG pipes for offshore gas projects in Brazil, boosting its order backlog and global footprint.

- In August 2024, ISMT Limited and Kirloskar Ferrous Industries Limited completed their merger, enhancing strategic growth in the Indian steel sector.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region dominates the stainless steel pipes and tubes market, driven by rapid industrialization, urbanization, and massive infrastructure investments in countries like China and India. China, as the dominating country, leads due to its vast manufacturing base, extensive construction projects, and growing energy demands, which fuel the adoption of these products in pipelines and buildings. This regional leadership is supported by abundant raw materials, low production costs, and government policies promoting industrial expansion, ensuring sustained demand across diverse applications.

North America holds a significant share in the market, with the United States as the dominating country, owing to advanced technological infrastructure and a strong focus on oil and gas exploration. The region's emphasis on upgrading aging pipelines and investing in renewable energy projects drives growth, complemented by stringent quality standards that favor high-performance stainless steel solutions. Innovation in manufacturing processes further enhances competitiveness, positioning North America as a key player in premium applications.

Europe's market is characterized by a mature industrial landscape, with Germany dominating due to its engineering prowess and automotive sector. The region benefits from strict environmental regulations that promote corrosion-resistant materials in chemical and power industries, alongside a push towards sustainable construction. Collaborative R&D efforts and a focus on high-value exports contribute to steady growth, maintaining Europe's role in specialized segments.

Latin America is emerging as a promising market, led by Brazil, where oil and gas discoveries and infrastructure developments are key drivers. The region's natural resources and increasing foreign investments in energy projects support demand, though economic volatility poses challenges. Focus on modernizing water and sewage systems also aids expansion, fostering gradual market penetration.

The Middle East & Africa region is growing, with Saudi Arabia dominating through its oil-dependent economy and diversification efforts into petrochemicals. Massive investments in desalination and construction projects leverage stainless steel's durability in arid conditions, while Africa's mining boom adds momentum. Regional stability and infrastructure initiatives are crucial for unlocking further potential.

Competitive Analysis

The global stainless steel pipes and tubes market is dominated by players:

- ArcelorMittal

- ThyssenKrupp

- Tenaris

- Pohang Iron & Steel (POSCO)

- Baosteel

- CENTRAVIS

- Tubacex

- Nippon Steel Corporation

- Outokumpu

- Sandvik

- Tata Steel

- JFE Steel Corporation

- AK Steel

- Jiuli Group

- Mannesmann Stainless Tubes

The global stainless steel pipes and tubes market is segmented as follows:

By Product Type

- Seamless Pipes and Tubes

- Welded Pipes and Tubes

- Others

By Application

- Oil and Gas

- Chemical Industry

- Automotive

- Construction

- Food Industry

- Power Industry

- Water Treatment

- Pharmaceutical

- Others

By End-Use Industry

- Energy & Power

- Construction & Infrastructure

- Automotive & Transportation

- Chemical & Petrochemical

- Healthcare & Pharmaceuticals

- Food & Beverage

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global stainless steel pipes and tubes market is dominated by players:

- ArcelorMittal

- ThyssenKrupp

- Tenaris

- Pohang Iron & Steel (POSCO)

- Baosteel

- CENTRAVIS

- Tubacex

- Nippon Steel Corporation

- Outokumpu

- Sandvik

- Tata Steel

- JFE Steel Corporation

- AK Steel

- Jiuli Group

- Mannesmann Stainless Tubes

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors