![]()

Search Market Research Report

Snow Melting System Market Size, Share Global Analysis Report, 2026-2034

Snow Melting System Market Size, Share, Growth Analysis Report By Type (Hydronic Snow Melting System, Electric Snow Melting System, Self-Regulating Cable Systems, Constant Wattage Systems, and Others), By Application (Driveways & Parking Areas, Walkways & Sidewalks, Rooftops & Gutters, Airport Runways & Aprons, Bridge Decks & Ramps, and Others), By End-User (Residential, Commercial, Municipal & Government, Industrial, Airports & Transportation, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

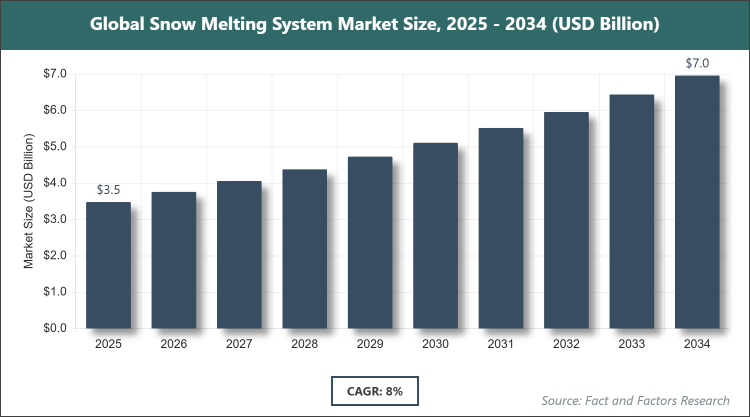

[238 + Pages Report] According to Facts & Factors, the global Snow Melting System market size was estimated at USD 3.48 billion in 2025 and is expected to reach USD 6.95 billion by the end of 2034. The Snow Melting System industry is anticipated to grow by a CAGR of 8.0% between 2026 and 2034. The Snow Melting System Market is driven by increasing emphasis on public safety, infrastructure resilience in cold-climate regions, and growing adoption of automated, energy-efficient de-icing technologies.

Market Overview

Market Overview

The Snow Melting System market encompasses engineered heating solutions installed beneath paved surfaces, rooftops, and other outdoor areas to automatically prevent snow accumulation and ice formation. These systems utilize either hydronic (fluid-filled tubing connected to boilers or heat pumps) or electric (resistance heating cables/mats) technologies, combined with moisture and temperature sensors, automated controls, and weather-responsive activation logic. They eliminate the need for manual shoveling, reduce reliance on chemical de-icers, minimize slip-and-fall liabilities, protect pavement integrity from freeze-thaw cycles, and ensure continuous accessibility for vehicles and pedestrians in commercial, residential, municipal, airport, and industrial settings during winter months.

Key Insights

- As per the analysis shared by our research analyst, the Snow Melting System market is estimated to grow annually at a CAGR of around 8.0% over the forecast period (2026-2034).

- In terms of revenue, the Snow Melting System market size was valued at around USD 3.48 billion in 2025 and is projected to reach USD 6.95 billion by 2034.

- The Snow Melting System Market is driven by rising safety regulations and demand for automated winter maintenance solutions.

- Based on the Type, the Hydronic Snow Melting System segment dominated the market in 2025 with a share of 66% due to superior energy efficiency for large areas, lower long-term operating costs, and compatibility with renewable heat sources.

- Based on the Application, the Driveways & Parking Areas segment dominated the market in 2025 with a share of 49%, owing to massive demand from residential homeowners and commercial property managers for safe, accessible vehicle movement.

- Based on the End-User, the Commercial segment dominated the market in 2025 with a share of 53% because retail centers, hotels, office campuses, and hospitals prioritize zero-downtime access and reduced liability during winter.

- North America dominated the global Snow Melting System market in 2025 with a share of 42%, attributed to severe and prolonged winters, stringent safety codes, advanced infrastructure, and high willingness to invest in premium automated solutions.

Growth Drivers

- Stringent Safety & Liability Regulations

A growing number of slip-and-fall lawsuits and municipal mandates for clear public walkways and emergency access routes have forced property owners and facility managers to adopt permanent, automated snow-melting systems as a proactive risk-mitigation measure.

Insurance companies in cold-climate regions increasingly offer premium discounts for buildings equipped with certified snow-melting infrastructure, creating a strong financial incentive for adoption across commercial and institutional properties.

Restraints

- High Upfront Capital and Installation Disruption

Significant excavation, concrete removal, tubing/cable laying, and surface reinstatement required during installation make retrofitting existing surfaces expensive and disruptive, deterring many property owners — especially in regions with shorter winter seasons.

Energy costs for electric systems and boiler/fuel expenses for hydronic setups remain a concern in areas with high electricity or natural gas prices, lengthening payback periods and limiting appeal in cost-sensitive markets.

Opportunities

- Renewable Energy Integration & Smart Controls

Pairing snow-melting systems with ground-source heat pumps, solar thermal, or district heating networks allows near-zero operational carbon emissions, aligning with net-zero building goals and qualifying for green-building incentives and subsidies.

Advancements in IoT sensors, AI weather prediction, and mobile-app controls enable demand-based activation (only when snow is actually falling), dramatically improving energy efficiency and creating attractive retrofit opportunities for existing buildings.

Challenges

- Climate Change & Variable Winter Patterns

Increasingly unpredictable and shorter winter seasons in some traditional cold regions reduce system utilization rates, lengthening ROI timelines and causing hesitation among prospective buyers.

Skilled labor shortages for specialized hydronic and electric installation work, combined with supply-chain volatility for high-quality tubing and cables, slow project execution, and raise costs in peak winter-preparation periods.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 3.48 Billion |

Projected Market Size in 2034 |

USD 6.95 Billion |

CAGR Growth Rate |

8.0% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Uponor Corporation, Watts Water Technologies, Inc., nVent Electric plc, Rehau Group, Warmup plc, HeatTrak LLC, and Others. |

Key Segment |

By Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Snow Melting System market is segmented by type, application, end-user, and region.

Based on Type Segment, the Snow Melting System market is divided into hydronic snow melting systems, electric snow melting systems, self-regulating cable systems, constant wattage systems, and others. The most dominant segment isthe Hydronic Snow Melting System, followed by the Electric Snow Melting System. Hydronic Snow Melting System dominates because it offers the best long-term energy efficiency for medium-to-large surfaces when integrated with condensing boilers or heat pumps, delivers even heat distribution, and achieves the lowest operating cost per square meter, making it the preferred solution for commercial parking lots, municipal sidewalks, and airport aprons that require reliable, high-capacity performance and drive the majority of large-scale project revenue.

Based on Application Segment, the Snow Melting System market is divided into driveways & parking areas, walkways & sidewalks, rooftops & gutters, airport runways & aprons, bridge decks & ramps, and others. The most dominant segment is Driveways & Parking Areas, followed by Walkways & Sidewalks. Driveways & Parking Areas lead the segment because they represent the largest cumulative surface area across residential, commercial, and institutional properties where safe vehicle access is non-negotiable during winter, generating the highest installation volume and stimulating continuous product innovation in durable, high-output heating solutions that accelerate market expansion.

Based on End-User Segment, the Snow Melting System market is divided into residential, commercial, municipal & government, industrial, airports & transportation, and others. The most dominant segment is Commercial, followed by Municipal & Government. Commercial dominates because hotels, shopping malls, office complexes, hospitals, and universities face the highest liability exposure and operational disruption from snow accumulation, leading them to invest heavily in automated systems that ensure 24/7 accessibility, guest/tenant safety, and brand reputation — creating the largest contract values and fastest adoption rate across the industry.

Recent Developments

- In January 2025, Uponor expanded its Ecoflex pre-insulated hydronic tubing offering with a new low-temperature snow-melt series optimized for air-to-water heat pumps, targeting net-zero commercial projects in Canada and the northern United States.

- In April 2025, nVent Electric launched the Raychem SENTRI intelligent snow-melt control system with cloud-based predictive activation using local weather API data, reducing energy use by up to 35% in pilot installations across Scandinavian municipalities.

- In July 2025, Watts Water Technologies introduced a modular retrofit electric mat system designed for existing concrete driveways, gaining rapid traction among U.S. residential contractors.

- In October 2025, Rehau secured a major contract to supply hydronic snow-melting systems for the new terminal expansion at Oslo Gardermoen Airport, highlighting growth in transportation infrastructure.

- In February 2026, Warmup plc released a Wi-Fi-enabled residential snow-melt controller compatible with major smart-home platforms (Alexa, Google Home, Apple HomeKit), expanding its footprint in premium suburban markets.

Regional Analysis

- North America to dominate the global market

North America leads the Snow Melting System market due to long, harsh winters across Canada and the northern United States, strict municipal safety codes requiring clear pedestrian and vehicular access, high liability awareness among property owners, and widespread acceptance of automated de-icing as a standard feature in new commercial and high-end residential construction. The region benefits from mature distribution networks, experienced installers, and strong R&D investment in energy-efficient and smart-controlled systems. Canada and the northern U.S. states drive consistent retrofit demand while new airport, hospital, and distribution-center projects accelerate large-scale hydronic installations. The United States dominates within North America through its enormous commercial real estate stock, advanced smart-building ecosystem, leadership in integrating snow-melt with building-management systems, and position as the largest single-country market for both residential driveway and municipal sidewalk applications.

Europe holds a strong second position in the Snow Melting System market, supported by severe winters in Scandinavia, the Alps, and parts of Central and Eastern Europe, rigorous workplace and public-access safety regulations, and increasing focus on sustainable heating solutions that utilize district heating or heat pumps. The region leads in retrofitting historic city centers and ski-resort infrastructure with minimal visual impact systems. Germany dominates within Europe owing to its engineering excellence, strict energy-efficiency standards, leadership in exporting high-quality hydronic components, and central role in supplying advanced snow-melting solutions to neighboring cold-climate countries.

Asia Pacific exhibits the fastest growth rate in the Snow Melting System market, driven by rising winter tourism in northern China, Japan, and South Korea, rapid airport and high-speed rail expansion in snowy regions, and increasing safety standards for commercial and public infrastructure. Government-backed smart-city projects and luxury residential developments in cold areas are accelerating adoption. China dominates within Asia Pacific with its massive infrastructure investment program, dominant domestic manufacturing capacity for electric systems, and growing number of northern cities requiring reliable snow-clearing solutions for transportation and commercial hubs.

Latin America shows niche but growing demand in the Snow Melting System market, primarily in high-altitude Andean countries and southern Patagonia, where tourism and mining operations face winter challenges. Improving safety awareness in commercial real estate is creating early opportunities. Chile dominates the region through its world-class ski resorts, mining infrastructure in snowy regions, and increasing investment in modern heating technologies for pedestrian safety and operational continuity.

The Middle East & Africa region has limited but emerging applications in the Snow Melting System market, concentrated in high-elevation areas of Turkey, Iran, and parts of the Atlas Mountains, as well as premium hospitality projects in northern Africa. Strategic tourism investments are introducing systems in select locations. Turkey dominates within the region with its mountainous terrain, established winter tourism industry, and modern commercial developments that increasingly incorporate snow-melting for guest safety and year-round accessibility.

Competitive Analysis

The global Snow Melting System market is dominated by players:

- Uponor Corporation

- Watts Water Technologies, Inc.

- nVent Electric plc (Raychem)

- Rehau Group

- Warmup plc

- HeatTrak LLC

- Thermon Group Holdings, Inc.

- Emerson Electric Co. (EasyHeat)

- Viega LLC

- Britech Corporation

The global Snow Melting System market is segmented as follows:

By Type

- Hydronic Snow Melting System

- Electric Snow Melting System

- Self-Regulating Cable Systems

- Constant Wattage Systems

- Others

By Application

- Driveways & Parking Areas

- Walkways & Sidewalks

- Rooftops & Gutters

- Airport Runways & Aprons

- Bridge Decks & Ramps

- Others

By End-User

- Residential

- Commercial

- Municipal & Government

- Industrial

- Airports & Transportation

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Uponor Corporation

- Watts Water Technologies, Inc.

- nVent Electric plc (Raychem)

- Rehau Group

- Warmup plc

- HeatTrak LLC

- Thermon Group Holdings, Inc.

- Emerson Electric Co. (EasyHeat)

- Viega LLC

- Britech Corporation

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors