![]()

Search Market Research Report

Set-Top Box Market Size, Share Global Analysis Report, 2026-2034

Set-Top Box Market Size, Share, Growth Analysis Report By Type (Cable Set-Top Box, IP Set-Top Box, Satellite Receiver Box, and Others), By Content Quality (SD, HD, UHD, 4K & Above), By Sales Channel (Direct Selling, Retail Outlets, Third-Party Distributors, Online), By End-User (Residential, Commercial), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

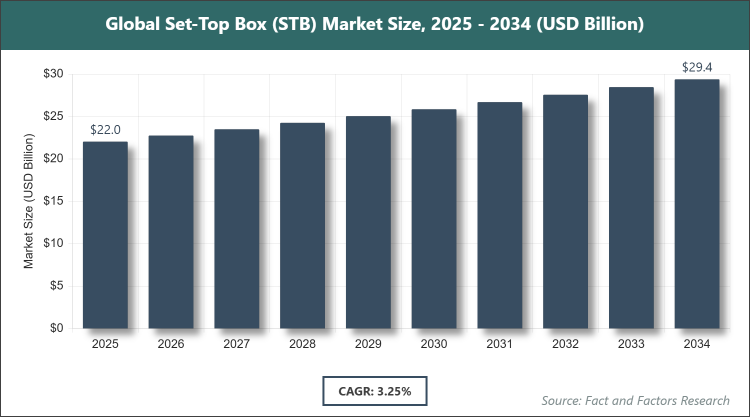

[220+ Pages Report] According to Facts & Factors, the global Set-Top Box market size was estimated at USD 22.04 billion in 2025 and is expected to reach USD 29.38 billion by the end of 2034. The Set-Top Box industry is anticipated to grow by a CAGR of 3.25% between 2026 and 2034. The Set-Top Box Market is driven by ongoing demand for managed digital TV and hybrid content delivery.

Market Overview

Market Overview

A set-top box (STB) is an electronic device that connects to a television set and an external signal source, converting the signal into content that can be displayed on the TV screen. It serves as an intermediary between broadcast signals from cable, satellite, or internet providers and the viewer's television, enabling access to a wide range of channels, on-demand content, and interactive features. Set-top boxes have evolved from basic signal decoders to advanced multimedia gateways that support high-definition video, streaming services, and smart home integration, playing a crucial role in the modern entertainment ecosystem by enhancing viewing experiences and providing content management capabilities.

Key Insights

- As per the analysis shared by our research analyst, the global Set-Top Box market is estimated to grow annually at a CAGR of around 3.25% over the forecast period (2026-2034).

- In terms of revenue, the global Set-Top Box market size was valued at around USD 22.04 Billion in 2025 and is projected to reach USD 29.38 Billion, by 2034.

- The Set-Top Box market is driven by ongoing demand for managed digital TV and hybrid content delivery.

- Based on the Type, IP Set-Top Box dominated the market in 2025 with a market share of 38% due to its flexible content delivery over broadband, integration with cloud middleware, and suitability for hybrid/digital networks.

- Based on the Content Quality, HD dominated the market in 2025 with a market share of 42% due to widespread consumer demand for improved picture quality, balance of cost and performance, and standard offering across cable, IP, and satellite platforms.

- Based on the Sales Channel, Direct Selling dominated the market in 2025 with a market share of 37% due to preferred channel for large-volume procurement by pay-TV operators, ensuring compatibility, bulk deployment, and long-term service agreements.

- Based on the End-User, Residential dominated the market in 2025 with a market share of 72% due to household demand for live TV, on-demand content, and high-resolution formats supported by increasing screen sizes and bundled services.

- Based on the region, Asia-Pacific dominated the market in 2025 with a market share of 39% due to high population density, rapid urbanization, expanding pay-TV/broadband penetration, and government-led digital TV transitions.

Growth Drivers

- Ongoing Demand for Managed Digital TV and Hybrid Content Delivery

The persistent need for reliable and managed digital television services continues to propel the set-top box market forward, as consumers seek seamless access to a blend of traditional broadcast and modern streaming content. This driver is particularly evident in regions where hybrid solutions bridge the gap between legacy systems and emerging technologies, allowing operators to deliver personalized viewing experiences without overhauling existing infrastructure. As content consumption patterns evolve, set-top boxes equipped with hybrid capabilities enable efficient signal processing and content aggregation, fostering user loyalty and reducing churn rates for service providers.

Furthermore, the integration of hybrid content delivery systems supports advanced features like time-shifting and multi-device streaming, which enhance overall user satisfaction and drive market expansion. This trend is supported by investments in network upgrades that facilitate smoother transitions to digital formats, ensuring that set-top boxes remain indispensable in the entertainment value chain.

- Expansion of Digital TV Infrastructure in Emerging Economies

Rapid development of digital television networks in developing countries is a key catalyst, as governments and operators invest in infrastructure to replace analog systems and expand coverage. This expansion creates substantial demand for set-top boxes that can decode digital signals and provide access to a broader array of channels and services, particularly in rural and underserved areas. By enabling affordable entry points to digital entertainment, these devices help bridge the digital divide and stimulate economic growth through increased media consumption.

In addition, partnerships between local governments and international tech firms accelerate this infrastructure buildup, leading to widespread adoption of standardized set-top box technologies. This not only boosts market volumes but also encourages innovation in cost-effective designs tailored to regional needs, further solidifying the role of set-top boxes in global digital transformation efforts.

- Migration Toward High-Definition Formats (HD, UHD, 4K)

The shift to superior video resolutions is driving upgrades in set-top box hardware, as consumers demand crisper images and immersive viewing experiences that align with advancements in display technologies. This migration is fueled by the proliferation of high-definition content from broadcasters and streaming platforms, necessitating devices capable of handling increased data throughput and processing demands. As a result, manufacturers are focusing on developing set-top boxes with enhanced chipsets and software to support these formats without compromising performance.

Moreover, this trend opens avenues for premium pricing strategies and bundled offerings that include high-definition subscriptions, contributing to revenue growth across the ecosystem. The ongoing evolution in content production standards ensures sustained demand for compatible set-top boxes, positioning them as essential components in the high-definition entertainment landscape.

- Integration with Smart Home Platforms and Broadband Networks

Increasing connectivity between set-top boxes and smart home ecosystems is enhancing their functionality, allowing seamless interaction with other devices like voice assistants and IoT systems. This integration leverages broadband networks to deliver not just entertainment but also home automation features, appealing to tech-savvy consumers seeking unified control interfaces. By embedding smart capabilities, set-top boxes evolve into central hubs for digital lifestyles, driving adoption in connected households.

Additionally, broadband expansions enable faster data transfers and lower latency, supporting advanced applications such as interactive gaming and virtual reality content through set-top boxes. This synergy between entertainment and smart home technologies fosters innovation and market differentiation, ensuring long-term relevance for set-top boxes in an increasingly interconnected world.

Restraints

- Growing Adoption of App-Based and Device-Less Viewing Through Smart TVs and Streaming Platforms

The rise of smart televisions and direct streaming apps is diminishing the necessity for traditional set-top boxes, as consumers opt for built-in functionalities that eliminate the need for additional hardware. This shift is accelerated by the convenience of app ecosystems on smart TVs, which offer direct access to content libraries without intermediary devices, leading to reduced demand in mature markets. Consequently, set-top box manufacturers face pressure to innovate or risk obsolescence in segments where integrated solutions dominate.

Furthermore, the proliferation of affordable smart TVs with robust operating systems challenges the value proposition of standalone set-top boxes, prompting a reevaluation of business models toward software-centric approaches. This restraint highlights the need for hybrid strategies that combine hardware with cloud-based services to maintain market share.

- Price Sensitivity and Extended Device Lifecycles in Mature Markets

In developed regions, consumers exhibit high price sensitivity and tend to prolong the use of existing set-top boxes due to their durability and sufficient performance for basic needs. This behavior slows replacement cycles and hampers market growth, as new features may not justify upgrades for cost-conscious users. Manufacturers must address this by offering value-added services or incentives to encourage renewals.

Moreover, extended lifecycles contribute to market saturation, where incremental innovations struggle to penetrate established user bases. This dynamic necessitates targeted marketing and partnerships with operators to bundle upgrades with service plans, mitigating the impact on overall sales volumes.

Opportunities

- Expansion of IP-Based and Hybrid Set-Top Box Deployments

The growth of internet protocol-based systems presents opportunities for deploying versatile set-top boxes that support both traditional and online content delivery. This expansion allows operators to offer scalable solutions that adapt to varying network conditions, attracting new subscribers in broadband-rich areas. By capitalizing on IP technologies, the market can tap into untapped segments like cord-cutters seeking flexible viewing options.

In addition, hybrid deployments enable seamless transitions between broadcast and streaming, enhancing user experiences and opening doors for premium content partnerships. This opportunity underscores the potential for set-top boxes to evolve into multifaceted platforms driving future growth.

- Upgrades in Fiber and Broadband Networks for IPTV Services

Investments in high-speed fiber optics and broadband infrastructure create fertile ground for advanced IPTV set-top boxes that deliver ultra-high-definition content with minimal buffering. These upgrades facilitate richer interactive features and personalized recommendations, appealing to demanding consumers. As networks mature, set-top boxes can leverage this bandwidth for innovative services like multi-room viewing.

Furthermore, this trend supports global expansion efforts, particularly in regions undergoing digital infrastructure overhauls, positioning set-top boxes as key enablers of next-generation television services.

- Transition from Analog to Digital Broadcasting in Emerging Markets

Ongoing shifts from analog to digital signals in developing nations offer significant opportunities for mass deployment of compatible set-top boxes. This transition, often mandated by governments, requires affordable devices to ensure widespread access, boosting market volumes. Manufacturers can collaborate with local entities to customize solutions for regional standards.

Additionally, this opportunity extends to educational and informational content delivery, enhancing social impact while expanding market reach in high-growth areas.

- Demand for Customizable User Interfaces and Operator-Branded Experiences

Rising expectations for personalized interfaces drive opportunities for set-top boxes with customizable software that aligns with operator branding and user preferences. This demand allows for differentiated offerings that improve engagement and retention. By focusing on user-centric designs, the market can foster loyalty in competitive landscapes.

Moreover, operator-branded experiences enable monetization through targeted advertising and add-on services, creating new revenue streams beyond hardware sales.

Challenges

- Rapid Technology Evolution Requiring Feature Upgrades and Cost Optimization

The fast pace of technological advancements necessitates continuous updates to set-top box features, straining resources for cost-effective development. This challenge involves balancing innovation with affordability to remain competitive. Manufacturers must invest in R&D while managing production costs to avoid pricing out potential buyers.

Furthermore, adapting to evolving standards like new compression algorithms adds complexity to supply chains and product lifecycles, requiring agile strategies to sustain market positions.

- Supply Chain Volatility and Component Cost Fluctuations

Global supply chain disruptions lead to inconsistent availability and pricing of key components, impacting set-top box production timelines and profitability. This volatility challenges manufacturers to secure stable sourcing and hedge against price swings. Diversifying suppliers becomes essential to mitigate risks.

In addition, component fluctuations can delay launches and affect quality control, necessitating robust contingency planning to maintain operational resilience.

- Maintaining Backward Compatibility with New Video Standards and Security Protocols

Ensuring new set-top boxes remain compatible with legacy systems while incorporating advanced security measures poses significant engineering challenges. This balance is crucial to avoid alienating existing users during upgrades. Compliance with evolving regulations adds layers of complexity.

Moreover, security protocols must evolve to counter threats like piracy, requiring ongoing software updates that can strain device performance in older models.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 22.04 Billion |

Projected Market Size in 2034 |

USD 29.38 Billion |

CAGR Growth Rate |

3.25% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Samsung Electronics Ltd., ARRIS International, Ecostar Corporation, Huawei Technologies Ltd., DISH Network, HUMAX, CISCO Systems Inc., Skyworth Group, ADB Global, Technicolor, and Others. |

Key Segment |

By Type, By Content Quality, By Sales Channel, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Set-Top Box market is segmented by type, content quality, sales channel, end-user, and region.

Based on Type Segment, the Set-Top Box market is divided into Cable Set-Top Box, IP Set-Top Box, Satellite Receiver Box, and others. The most dominant segment is IP Set-Top Box with a 38% share, as it offers flexible content delivery over broadband networks, seamless integration with cloud-based middleware, and adaptability to hybrid and fully digital broadcasting environments, which drives market growth by enabling operators to provide on-demand services and reduce dependency on traditional infrastructure; the second most dominant is Cable Set-Top Box at 34%, valued for its reliability in delivering high-bandwidth content through established cable networks, supporting consistent performance in densely populated urban areas and contributing to market expansion through compatibility with existing subscriber bases.

Based on Content Quality Segment, the Set-Top Box market is divided into SD, HD, UHD, 4K & Above. The most dominant segment is HD with a 42% share, owing to its optimal balance of enhanced picture quality and affordability, making it a standard across various platforms like cable, IP, and satellite, which propels market growth by meeting widespread consumer expectations for improved visuals without the premium costs of higher resolutions; the second most dominant is UHD at 25%, driven by increasing availability of ultra-high-definition content and compatible displays, fostering market development through immersive viewing experiences that attract tech-enthusiast households.

Based on Sales Channel Segment, the Set-Top Box market is divided into Direct Selling, Retail Outlets, Third-Party Distributors, Online. The most dominant segment is Direct Selling with a 37% share, as it facilitates bulk purchases by pay-TV operators ensuring device compatibility and customized service agreements, which accelerates market growth by streamlining deployment and supporting long-term operator-subscriber relationships; the second most dominant is Retail Outlets at 28%, popular for providing hands-on consumer access and immediate availability, aiding market penetration through targeted promotions and in-store demonstrations.

Based on End-User Segment, the Set-Top Box market is divided into Residential, Commercial. The most dominant segment is Residential with a 72% share, fueled by household demands for diverse entertainment options including live TV and streaming, which boosts market growth via bundled home services and larger screen integrations; the second most dominant is Commercial at 28%, utilized in hospitality and enterprise settings for managed content delivery, contributing to market expansion through specialized applications like digital signage and guest entertainment systems.

Recent Developments

- Launch of IP-based hybrid set-top boxes integrating streaming services has revolutionized content access by combining traditional broadcast with popular OTT platforms, allowing users to switch seamlessly between live channels and on-demand libraries, thereby enhancing viewer engagement and supporting operator efforts to retain subscribers in a competitive landscape.

- Introduction of energy-efficient and compact device designs addresses environmental concerns and space constraints in modern homes, incorporating low-power chipsets and smaller form factors that reduce electricity consumption while maintaining high performance, appealing to eco-conscious consumers and complying with global sustainability regulations.

- Expansion of UHD and 4K-capable set-top box portfolios caters to the growing demand for superior resolution content, featuring advanced processors and HDR support that deliver vivid colors and sharper images, driving upgrades among users with compatible televisions and boosting market revenues through premium product lines.

- Development of advanced content security and conditional access systems protects against piracy and unauthorized access, utilizing encryption technologies and secure boot mechanisms to safeguard intellectual property, which builds trust among content providers and enables the distribution of high-value programming.

- Strategic collaborations between operators and hardware manufacturers foster innovation in customized solutions, such as branded interfaces and integrated ecosystems, leading to tailored devices that align with specific service offerings and improve overall user satisfaction.

Regional Analysis

- Asia Pacific to dominate the global market

The Asia Pacific region stands out due to its vast population and accelerating urbanization, which fuel the adoption of digital entertainment solutions. Countries like China and India lead with extensive investments in broadband infrastructure, enabling widespread access to diverse content. This region's dynamic media landscape, characterized by a mix of traditional broadcasting and emerging streaming services, supports innovative device integrations. Furthermore, government initiatives promoting digital literacy and television upgrades enhance market penetration, creating a vibrant ecosystem for content creators and distributors. The cultural emphasis on family-oriented viewing also drives demand for multi-feature devices that cater to varied preferences.

North America benefits from advanced technological adoption and a mature pay-TV market, with the United States dominating through its robust ecosystem of content providers and high-speed internet availability. Innovation in user interfaces and smart integrations keeps the region competitive, while consumer preferences for premium content push continuous hardware evolution. Regulatory frameworks ensuring content diversity further strengthen the market, fostering partnerships that enhance service quality.

Europe's market is shaped by stringent regulations on digital broadcasting and a focus on high-quality content, with Germany and the United Kingdom leading through strong infrastructure and consumer spending on entertainment. The region's emphasis on energy efficiency and data privacy influences device designs, promoting sustainable practices. Collaborative efforts among EU nations facilitate cross-border content sharing, enriching viewer options.

Latin America's growth is driven by improving economic conditions and expanding middle-class populations, with Brazil and Mexico as key players due to their large urban centers and increasing internet penetration. Local content production thrives, supported by affordable devices that bridge access gaps. Regional alliances aim to standardize technologies, aiding seamless market expansion.

The Middle East & Africa region experiences progress through infrastructure developments and rising disposable incomes, with the United Arab Emirates and South Africa dominating via investments in smart cities and digital transitions. Efforts to combat content piracy enhance security features in devices, while cultural adaptations ensure relevance. International collaborations bring advanced technologies, accelerating adoption rates.

Competitive Analysis

The global Set-Top Box market is dominated by players:

- Samsung Electronics Ltd.

- ARRIS International

- Ecostar Corporation

- Huawei Technologies Ltd.

- DISH Network

- HUMAX

- CISCO Systems Inc.

- Skyworth Group

- ADB Global

- Technicolor

The global Set-Top Box market is segmented as follows:

By Type

- Cable Set-Top Box

- IP Set-Top Box

- Satellite Receiver Box

- Others

By Content Quality

- SD

- HD

- UHD

- 4K & Above

By Sales Channel

- Direct Selling

- Retail Outlets

- Third-Party Distributors

- Online

By End-User

- Residential

- Commercial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Set-Top Box market is dominated by players:

- Samsung Electronics Ltd.

- ARRIS International

- Ecostar Corporation

- Huawei Technologies Ltd.

- DISH Network

- HUMAX

- CISCO Systems Inc.

- Skyworth Group

- ADB Global

- Technicolor

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors