![]()

Search Market Research Report

Rodenticides Market Size, Share Global Analysis Report, 2026-2034

Rodenticides Market Size, Share, Growth Analysis Report By Type (Anticoagulant, Non-Anticoagulant), By Form (Pellets, Blocks, Powder, Sprays, Others), By Application (Agricultural Fields, Warehouses, Urban Centers, Residential, Others), By End-User (Agriculture, Pest Control Companies, Households, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

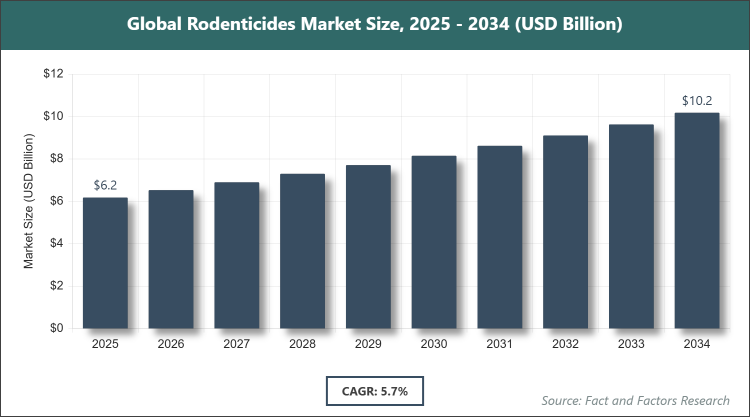

[220+ Pages Report] According to Facts & Factors, the global Rodenticides market size was estimated at USD 6.18 billion in 2025 and is expected to reach USD 10.20 billion by the end of 2034. The Rodenticides industry is anticipated to grow by a CAGR of 5.7% between 2026 and 2034. The Rodenticides Market is driven by increasing rodent infestations in urban and agricultural settings.

Market Overview

Market Overview

The rodenticides market encompasses products designed to control and eliminate rodent populations, including rats and mice, which pose significant threats to public health, agriculture, and infrastructure. These chemicals work by disrupting vital biological processes in rodents, leading to their demise, and are available in various formulations to suit different applications. The market serves a broad range of sectors, from farming to urban pest management, addressing issues like disease transmission and crop damage caused by rodents.

Key Insights

- As per the analysis shared by our research analyst, the Rodenticides market is estimated to grow annually at a CAGR of around 5.7% over the forecast period (2026-2034).

- In terms of revenue, the Rodenticides market size was valued at around USD 6.18 Billion in 2025 and is projected to reach USD 10.20 Billion by 2034.

- Due to a variety of driving factors, the market is predicted to rise at a significant rate.

- Based on the Type, Anticoagulant segment accounted for the largest market share of 70% in 2025 and is expected to maintain its dominance due to its high efficacy in causing internal bleeding in rodents with a single dose, making it preferred for large-scale infestations.

- Based on the Form, Blocks segment accounted for the largest market share of 45% in 2025 and is expected to maintain its dominance due to their durability, weather resistance, and ease of placement in bait stations, which enhances safety and effectiveness in various environments.

- Based on the Application, Pest Control Companies segment accounted for the largest market share of 39% in 2025 and is expected to maintain its dominance due to the professional expertise required for safe and efficient rodent management in commercial and residential settings.

- Based on the End-User, Pest Control Companies segment accounted for the largest market share of 49% in 2025 and is expected to maintain its dominance due to the growing demand for specialized services that comply with regulatory standards and minimize environmental impact.

- North America region was leading the market in 2025 with over 35% market share and is expected to maintain its dominance due to stringent food safety regulations, high urbanization rates, and extensive agricultural activities that necessitate robust rodent control measures.

Growth Drivers

- Increasing Urbanization and Rodent Infestations

Urban expansion has led to higher population densities, creating ideal conditions for rodent proliferation through increased waste generation and habitat disruption. This surge in rodent populations heightens the risk of disease transmission and property damage, prompting greater demand for effective rodenticides.

Rodenticides play a crucial role in mitigating these risks by providing targeted control solutions that are essential for maintaining public health and sanitation in densely populated areas. As cities continue to grow, the need for innovative and efficient rodent management strategies will further propel market expansion.

Restraints

- Stringent Regulatory Restrictions on Toxic Chemicals

Governments worldwide are imposing stricter regulations on the use of highly toxic rodenticides to protect non-target wildlife and ecosystems, limiting product availability and increasing compliance costs for manufacturers. These restrictions often require extensive testing and approval processes, delaying new product launches.

The shift toward safer alternatives can also reduce the market for traditional rodenticides, as consumers and regulators prioritize environmental sustainability. This regulatory landscape challenges industry players to innovate while navigating complex approval hurdles.

Opportunities

- Development of Eco-Friendly and Biodegradable Rodenticides

The rising demand for sustainable pest control solutions opens avenues for the creation of biodegradable rodenticides that minimize environmental harm while effectively controlling rodent populations. Innovations in natural ingredients and low-toxicity formulations can attract environmentally conscious consumers and comply with green regulations.

This trend allows companies to differentiate their products in a competitive market, potentially capturing new segments like organic farming and eco-sensitive urban areas. Investment in research for these alternatives can lead to long-term growth and brand loyalty.

Challenges

- Rising Rodent Resistance to Existing Formulations

Rodents are developing genetic resistance to common anticoagulants, reducing the effectiveness of standard rodenticides and requiring higher doses or frequent applications. This resistance complicates pest management efforts and increases costs for end-users.

Addressing this issue demands ongoing research into new active ingredients and rotation strategies, which can strain resources for smaller manufacturers. Failure to adapt may result in market share loss to more innovative competitors.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 6.18 Billion |

Projected Market Size in 2034 |

USD 10.20 Billion |

CAGR Growth Rate |

5.7% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

BASF SE, Bayer AG, Syngenta AG, Rentokil Initial Plc, Neogen Corporation, Bell Laboratories, Liphatech Inc., UPL Limited, PelGar International, Senestech Inc., JT Eaton & Co. Inc., and Others. |

Key Segment |

By Type, By Form, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Rodenticides market is segmented by type, form, application, end-user, and region.

Based on Type Segment, the Rodenticides market is divided into Anticoagulant, Non-Anticoagulant, and Others. The Anticoagulant segment is the most dominant, holding approximately 70% market share, due to its proven effectiveness in disrupting blood clotting in rodents, leading to a humane and efficient control method that requires minimal bait consumption. This dominance drives the market by enabling large-scale applications in agriculture and urban settings, reducing overall infestation rates and supporting food security. The Non-Anticoagulant segment is the second most dominant, with around 30% share, as it offers rapid action for immediate control in resistance-prone areas, helping to maintain market growth by providing alternatives where anticoagulants fail.

Based on Form Segment, the Rodenticides market is divided into Pellets, Blocks, Powder, Sprays, and Others. The Blocks segment is the most dominant, holding approximately 45% market share, owing to their long-lasting nature and resistance to environmental degradation, making them ideal for outdoor and warehouse use where consistent bait availability is crucial. This helps drive the market by ensuring reliable rodent control over extended periods, minimizing reapplication needs. The Pellets segment is the second most dominant, with around 38% share, due to their ease of dispersion and high palatability, which enhances uptake by rodents and supports efficient pest management in agricultural fields.

Based on Application Segment, the Rodenticides market is divided into Agricultural Fields, Warehouses, Urban Centers, Residential, and Others. The Pest Control Companies segment is the most dominant, holding approximately 39% market share, as professionals require specialized products for compliant and effective services in diverse environments. This drives the market by promoting standardized, safe applications that reduce risks to humans and pets. The Agricultural Fields segment is the second most dominant, with around 30% share, due to the need to protect crops from rodent damage, thereby sustaining food production and economic stability in farming regions.

Based on End-User Segment, the Rodenticides market is divided into Agriculture, Pest Control Companies, Households, and Others. The Pest Control Companies segment is the most dominant, holding approximately 49% market share, driven by the expertise and scale of operations that demand high-volume, reliable rodenticides. This contributes to market growth by facilitating widespread adoption of best practices in pest management. The Agriculture segment is the second most dominant, with around 30% share, as farmers rely on these products to safeguard yields, directly impacting global food supply chains.

Recent Developments

- In November 2024, the United States Environmental Protection Agency (EPA) released its final biological evaluation of 11 rodenticides, concluding that 88% of endangered species face no adverse impact under proposed mitigations, which supports continued market access while emphasizing wildlife protection.

- In October 2024, BASF Group reported higher contributions from its Agricultural Solutions division, including rodenticides, and highlighted investments in flocoumafen and cholecalciferol formulations, boosting innovation in eco-friendly options.

- In August 2024, the EPA issued cancellation orders for multiple pesticide registrations, mandating stewardship for existing inventory, which influences supply chains and encourages shifts to compliant products.

- In March 2024, Bayer AG announced plans to launch ten blockbuster crop-protection products, including next-generation rodenticide technologies, aiming to address resistance and enhance efficacy.

Regional Analysis

- North America to dominate the global market

North America leads the rodenticides market, driven by advanced pest control infrastructure and high awareness of health risks from rodents. The United States, as the dominating country, benefits from extensive urban development and agricultural lands that require robust rodent management to prevent economic losses and disease outbreaks. Strict regulations ensure safe product use, fostering innovation in sustainable solutions.

Europe maintains a strong position with emphasis on environmental regulations and integrated pest management. Germany dominates, leveraging its industrial and farming sectors to implement effective rodent control, balancing efficacy with ecological concerns to protect biodiversity.

Asia Pacific experiences rapid growth due to urbanization and agricultural expansion. China, the dominating country, addresses widespread rodent issues in rural and urban areas through large-scale applications, supporting food security amid population growth.

Latin America shows steady demand, influenced by agricultural needs and tropical climates favoring rodent proliferation. Brazil dominates, focusing on protecting vast farmlands and urban centers from infestations that threaten crops and public health.

The Middle East & Africa region grows with increasing infrastructure development. South Africa dominates, utilizing rodenticides to manage rodents in emerging urban and agricultural landscapes, aiding in disease prevention and economic stability.

Competitive Analysis

The global Rodenticides market is dominated by players:

- BASF SE

- Bayer AG

- Syngenta AG

- Rentokil Initial Plc

- Neogen Corporation

- Bell Laboratories

- Liphatech Inc.

- UPL Limited

- PelGar International

- Senestech Inc.

- JT Eaton & Co. Inc.

- And Others.

The global Rodenticides market is segmented as follows:

By Type

- Anticoagulant

- Non-Anticoagulant

- Others

By Form

- Pellets

- Blocks

- Powder

- Sprays

- Others

By Application

- Agricultural Fields

- Warehouses

- Urban Centers

- Residential

- Others

By End-User

- Agriculture

- Pest Control Companies

- Households

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Rodenticides market is dominated by players:

- BASF SE

- Bayer AG

- Syngenta AG

- Rentokil Initial Plc

- Neogen Corporation

- Bell Laboratories

- Liphatech Inc.

- UPL Limited

- PelGar International

- Senestech Inc.

- JT Eaton & Co. Inc.

- And Others.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors