![]()

Search Market Research Report

Portable Oxygen Concentrators Market Size, Share Global Analysis Report, 2026-2034

Portable Oxygen Concentrators Market Size, Share, Growth Analysis Report By Delivery System (Continuous Flow, Pulse Flow, and Others), By Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Respiratory Distress Syndrome, and Others), By End-User (Homecare, Hospitals and Clinics, Ambulatory Surgical Centers, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

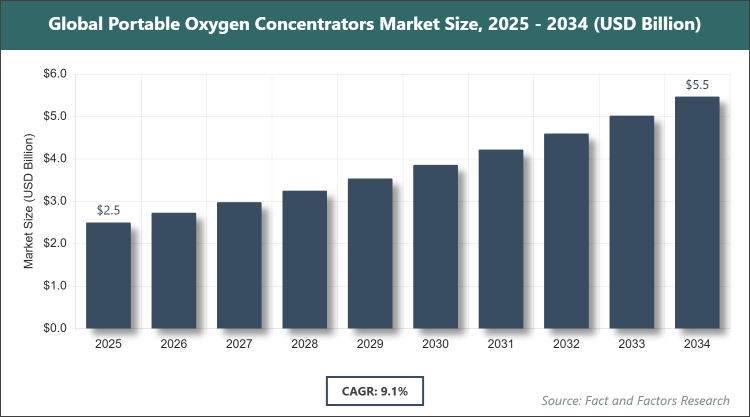

[215+ Pages Report] According to Facts & Factors, the global Portable Oxygen Concentrators market size was estimated at USD 2.5 billion in 2025 and is expected to reach USD 5.5 billion by the end of 2034. The Portable Oxygen Concentrators industry is anticipated to grow by a CAGR of 9.1% between 2026 and 2034. The Portable Oxygen Concentrators Market is driven by the increasing prevalence of respiratory diseases and an aging population.

Market Overview

Market Overview

Portable Oxygen Concentrators are medical devices designed to deliver concentrated oxygen to individuals with respiratory conditions by extracting oxygen from ambient air through a process involving pressure swing adsorption or membrane separation. These compact, battery-operated units provide mobility and independence for users requiring supplemental oxygen therapy, distinguishing them from stationary concentrators or traditional oxygen tanks by enabling active lifestyles without the need for frequent refills. The market encompasses the design, manufacturing, and distribution of these devices, catering to patients with chronic ailments like COPD or asthma, focusing on enhancing quality of life through reliable, on-the-go oxygen supply without quantitative specifics.

Key Insights

- As per the analysis shared by our research analyst, the global Portable Oxygen Concentrators market is estimated to grow annually at a CAGR of around 9.1% over the forecast period (2026-2034).

- In terms of revenue, the global Portable Oxygen Concentrators market size was valued at around USD 2.5 billion in 2025 and is projected to reach USD 5.5 billion by 2034.

- The market is driven by the rising prevalence of chronic respiratory diseases and the growing preference for home-based oxygen therapy.

- Based on the delivery system, the pulse flow segment dominated with a 62% share due to its energy efficiency and ability to deliver oxygen on demand.

- Based on the application, the COPD segment dominated with a 48% share, owing to the high incidence of COPD globally requiring long-term oxygen support.

- Based on the end-user, the homecare segment dominated with a 65% share because of the shift towards patient-centric care and cost-effectiveness.

- Based on the region, North America dominated with a 38% share attributed to advanced healthcare infrastructure and high awareness levels.

Growth Drivers

- Rising Prevalence of Respiratory Diseases

The increasing incidence of conditions such as COPD, asthma, and sleep apnea, driven by factors like air pollution, smoking, and aging populations, has heightened the demand for portable oxygen solutions that allow patients to maintain daily activities. This driver is particularly pronounced in urban areas where environmental factors exacerbate respiratory issues, leading to greater adoption of user-friendly devices.

Additionally, technological advancements in battery life and device miniaturization have made these concentrators more appealing, expanding their use beyond traditional settings and fostering market growth through improved patient compliance and satisfaction.

Restraints

- High Initial Costs and Reimbursement Challenges

The substantial upfront expense of portable oxygen concentrators limits accessibility for many patients, especially in low-income regions, while inconsistent insurance coverage and reimbursement policies further hinder widespread adoption. These financial barriers can delay purchases and affect market penetration.

Moreover, dependency on electricity and the need for regular maintenance add to operational costs, posing challenges in areas with unreliable power supply and potentially restricting growth in emerging markets.

Opportunities

- Technological Innovations and Smart Features

Advancements like integration with mobile apps for monitoring and AI-driven oxygen delivery systems present opportunities to enhance device functionality, attracting tech-savvy users and opening new revenue streams. These innovations can improve treatment outcomes and user experience.

Furthermore, expanding into untapped markets in developing countries through affordable models and partnerships with healthcare providers could significantly broaden the customer base, capitalizing on rising healthcare investments.

Challenges

- Regulatory Hurdles and Competition from Alternatives

Stringent approval processes for medical devices vary across regions, delaying product launches and increasing development costs, while competition from oxygen cylinders and liquid oxygen systems challenges market share. Navigating these regulations requires substantial resources.

In addition, concerns over device reliability during travel or in extreme conditions can undermine consumer confidence, necessitating ongoing R&D to address durability and performance issues.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.5 Billion |

Projected Market Size in 2034 |

USD 5.5 Billion |

CAGR Growth Rate |

9.1% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Inogen Inc., Koninklijke Philips N.V., Invacare Corporation, Chart Industries Inc., ResMed Inc., Drive DeVilbiss Healthcare, Precision Medical Inc., GCE Group, O2 Concepts LLC, Caire Inc., and Others. |

Key Segment |

By Delivery System, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Portable Oxygen Concentrators market is segmented by delivery system, application, end-user, and region.

Based on Delivery System Segment, the Portable Oxygen Concentrators market is divided into continuous flow, pulse flow, and others. The most dominant segment is pulse flow, followed by continuous flow as the second most dominant. Pulse flow dominates due to its efficient oxygen delivery synchronized with breathing patterns, conserving battery life and enabling lighter designs that enhance portability for active users, driving the market by meeting the demand for mobility in daily life; continuous flow, providing a steady oxygen supply ideal for severe cases or sleep therapy, supports growth by catering to patients needing constant support, thus expanding application in homecare and clinical settings.

Based on Application Segment, the Portable Oxygen Concentrators market is divided into chronic obstructive pulmonary disease (COPD), asthma, respiratory distress syndrome, and others. The most dominant segment is COPD, followed by asthma as the second most dominant. COPD leads owing to its high global prevalence among the elderly and smokers, requiring long-term oxygen therapy that portable concentrators effectively provide for improved quality of life, propelling market expansion through sustained demand; asthma, with episodic needs for supplemental oxygen during exacerbations, drives growth by offering quick relief and portability for on-the-go management, enhancing patient independence.

Based on End-User Segment, the Portable Oxygen Concentrators market is divided into homecare, hospitals and clinics, ambulatory surgical centers, and others. The most dominant segment is homecare, followed by hospitals and clinics as the second most dominant. Homecare dominates as it allows cost-effective, long-term management of chronic conditions in familiar environments, reducing hospital visits and boosting market demand through preference for home-based care; hospitals and clinics utilize these devices for acute care and mobility within facilities, contributing to growth by integrating portable solutions into treatment protocols for efficient patient handling.

Recent Developments

- In March 2025, O2Xpress launched a novel portable oxygen concentrator designed to support patients with respiratory conditions, enabling more active lives.

- In June 2025, Inogen Inc. announced the launch of VoxiTM 5, a new stationary oxygen concentrator to improve access to high-quality oxygen therapy for long-term care patients.

- In July 2025, VARON introduced the VP-8G portable oxygen concentrator, the lightest and most advanced model with eight adjustable pulse flow settings.

- In January 2025, Caire launched IntenOxy 5, a stationary oxygen concentrator with efficient power consumption and high oxygen concentration.

Regional Analysis

- North America to Dominate the Global Market

North America dominates the Portable Oxygen Concentrators market, led by the United States, where advanced healthcare systems, high prevalence of respiratory diseases, favorable reimbursement policies, and strong awareness drive extensive adoption, supported by leading manufacturers and robust R&D investments that innovate device features for better patient outcomes.

Europe holds a significant share, with Germany and the UK at the forefront, benefiting from aging populations, stringent health regulations promoting quality devices, and integrated care models that emphasize home therapy to reduce hospital burdens and enhance life quality for chronic patients.

Asia Pacific is experiencing rapid growth, dominated by China and India, fueled by urbanization, rising pollution levels increasing respiratory issues, expanding middle-class access to healthcare, and government initiatives improving medical infrastructure to address burgeoning demand.

Latin America shows promising expansion, led by Brazil, through improving economic conditions, greater healthcare spending, and awareness campaigns on respiratory health that encourage portable device use for managing conditions in diverse geographic settings.

The Middle East & Africa region is emerging, with South Africa leading, driven by increasing chronic disease rates, investments in healthcare facilities, and international aid programs introducing advanced portable technologies to remote areas.

Competitive Analysis

The global Portable Oxygen Concentrators market is dominated by players:

- Inogen Inc.

- Koninklijke Philips N.V.

- Invacare Corporation

- Chart Industries Inc.

- ResMed Inc.

- Drive DeVilbiss Healthcare

- Precision Medical Inc.

- GCE Group

- O2 Concepts LLC

- Caire Inc.

- Others

The global Portable Oxygen Concentrators market is segmented as follows:

By Delivery System

- Continuous Flow

- Pulse Flow

By Application

- Chronic Obstructive Pulmonary Disease (COPD)

- Asthma

- Respiratory Distress Syndrome

By End-User

- Homecare

- Hospitals and Clinics

- Ambulatory Surgical Centers

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Inogen Inc.

- Koninklijke Philips N.V.

- Invacare Corporation

- Chart Industries Inc.

- ResMed Inc.

- Drive DeVilbiss Healthcare

- Precision Medical Inc.

- GCE Group

- O2 Concepts LLC

- Caire Inc.

- Others

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors