![]()

Search Market Research Report

Medical Tubing Market Size, Share Global Analysis Report, 2026-2034

Medical Tubing Market Size, Share, Growth Analysis Report By Material (PVC, Silicone, Polyolefins, Thermoplastics, Others), By Application (Bulk Disposable Tubing, Catheters & Cannulas, Drug Delivery Systems, Special Applications), By End-User (Hospitals & Clinics, Ambulatory Surgical Centers, Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

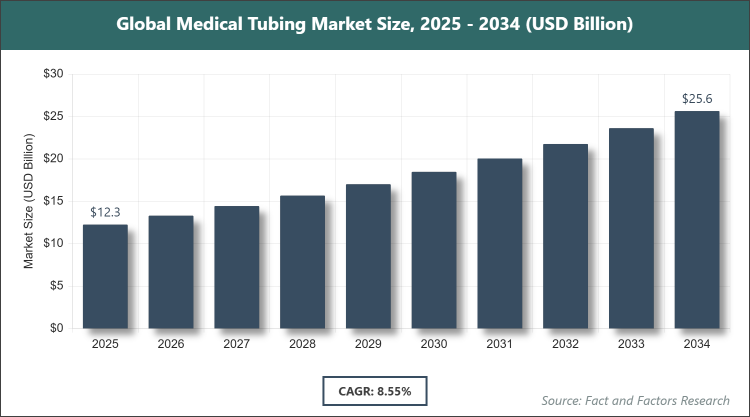

[218+ Pages Report] According to Facts & Factors, the global Medical Tubing market size was estimated at USD 12.26 billion in 2025 and is expected to reach USD 25.56 billion by the end of 2034. The Medical Tubing industry is anticipated to grow by a CAGR of 8.55% between 2026 and 2034. The Medical Tubing Market is driven by increasing demand for minimally invasive procedures and advanced medical devices.

Market Overview

Market Overview

Medical tubing refers to flexible, hollow tubes made from various polymers and materials, designed for use in healthcare applications to transport fluids, gases, or instruments within the body or medical devices. These tubes are engineered to meet stringent biocompatibility, sterility, and durability standards, serving critical roles in procedures such as infusion therapy, catheterization, and respiratory support. They vary in structure, including single-lumen or multi-lumen designs, and are essential for ensuring safe, efficient delivery of treatments while minimizing patient risk in clinical, surgical, and home care environments.

Key Insights

- As per the analysis shared by our research analyst, the global Medical Tubing market is estimated to grow annually at a CAGR of around 8.55% over the forecast period (2026-2034).

- In terms of revenue, the global Medical Tubing market size was valued at around USD 12.26 billion in 2025 and is projected to reach USD 25.56 billion by 2034.

- The market is driven by the rising prevalence of chronic diseases and advancements in biocompatible materials.

- Based on the material, the PVC segment dominated the market with a share of 45%, as it offers cost-effectiveness, flexibility, and ease of sterilization, ideal for disposable applications.

- Based on the application, the catheters & cannulas segment dominated with a share of 35%, due to increasing minimally invasive surgeries requiring precise and durable tubing.

- Based on the end-user, the hospitals & clinics segment dominated with a share of 50%, attributed to high procedural volumes and advanced infrastructure.

- North America dominated the global market with a share of 40%, owing to robust healthcare spending, technological innovations, and high chronic disease incidence.

Growth Drivers

- Increasing Demand for Minimally Invasive Procedures

The surge in preference for minimally invasive surgeries, driven by benefits like reduced recovery time and lower complication risks, has boosted the need for specialized medical tubing in catheters and endoscopes. This trend is supported by aging populations and rising chronic conditions, prompting healthcare providers to adopt advanced tubing materials that enhance procedural precision and patient safety.

Furthermore, innovations in tubing design, such as multi-lumen configurations, allow for multifunctional use in complex interventions, aligning with evolving surgical techniques. As global healthcare systems prioritize cost-effective, efficient treatments, this driver sustains market momentum through expanded applications in ambulatory and home settings.

Restraintsa

- Stringent Regulatory Compliance

The rigorous approval processes and quality standards imposed by agencies like the FDA and EMA increase development timelines and costs for medical tubing manufacturers, potentially delaying market entry for new products. This restraint is amplified by the need for extensive testing to ensure biocompatibility and sterility, limiting innovation in smaller firms.

Additionally, varying international regulations complicate global distribution, requiring customized compliance strategies that strain resources. In emerging markets, these barriers may hinder the adoption of advanced tubing, favoring basic alternatives and capping overall market growth despite demand.

Opportunities

- Advancements in Biocompatible Materials

The development of novel polymers like bioresorbable and antimicrobial tubing opens avenues for enhanced patient outcomes in long-term implants and infection-prone applications. Collaborations between material scientists and device makers are accelerating these innovations, supported by investments in R&D for sustainable, eco-friendly options.

Moreover, the integration of smart technologies, such as sensor-embedded tubing, enables real-time monitoring, appealing to telemedicine and personalized medicine trends. This opportunity diversifies product portfolios, capturing shares in high-growth areas like drug delivery and diagnostics.

Challenges

- Raw Material Price Volatility

Fluctuations in prices of key materials like silicone and PVC, influenced by supply chain disruptions and geopolitical factors, elevate production costs and affect profitability. This challenge is particularly acute during global events, leading to shortages that delay manufacturing.

In addition, the push for sustainable sourcing adds complexity, as eco-friendly alternatives may be costlier. Balancing cost with quality is critical, but persistent volatility could erode competitive edges and slow expansion in price-sensitive regions.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 12.26 Billion |

Projected Market Size in 2034 |

USD 25.56 Billion |

CAGR Growth Rate |

8.55% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Saint-Gobain, Freudenberg Medical, Nordson Corporation, Lubrizol Corporation, Trelleborg AB, Asahi Tec Corp., MDC Industries, ZARYS International Group, Hitachi Cable America Inc., NewAge Industries, Inc., TE Connectivity, Spectrum Plastics Group, ATAG SpA, and Others. |

Key Segment |

By Material, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Medical Tubing market is segmented by material, application, end-user, and region.

Based on Material Segment, the Medical Tubing market is divided into PVC, silicone, polyolefins, thermoplastics, others. The PVC segment emerges as the most dominant, holding approximately 45% market share, primarily due to its low cost, versatility, and compatibility with sterilization processes, making it ideal for single-use disposables, thereby driving the market by enabling affordable, high-volume production for global healthcare needs. The silicone segment follows as the second most dominant, with around 25% share, owing to its biocompatibility, flexibility, and resistance to extreme temperatures, supporting advanced applications like implants and contributing to market growth through enhanced durability and patient safety.

Based on Application Segment, the Medical Tubing market is divided into bulk disposable tubing, catheters & cannulas, drug delivery systems, special applications. The catheters & cannulas segment is the most dominant, capturing about 35% of the market, as it caters to the rising demand for interventional procedures, driven by chronic diseases, helping to propel the market by facilitating precise fluid and device delivery. The bulk disposable tubing segment ranks second, with roughly 30% share, benefiting from its use in routine infusions and diagnostics, aiding market expansion by promoting hygiene and reducing cross-contamination risks.

Based on End-User Segment, the Medical Tubing market is divided into hospitals & clinics, ambulatory surgical centers, others. The hospitals & clinics segment is the most dominant, capturing about 50% of the market, propelled by high patient throughput and complex procedures requiring reliable tubing, thereby driving the market through sustained demand for quality medical devices. The ambulatory surgical centers segment ranks second, with roughly 25% share, utilizing tubing for outpatient care, contributing to market growth by supporting cost-effective, minimally invasive treatments.

Recent Developments

- In May 2025, Freudenberg Medical invested in R&D for advanced catheter and thermoplastic molding capacity in Costa Rica, enhancing production for minimally invasive applications.

- In July 2024, Lubrizol Corporation announced a USD 350 million investment near Chennai, India, to expand extrusion capacity for medical tubing, reducing lead times for local OEMs.

- In November 2023, Nordson Corporation acquired a specialty polymer firm to bolster its portfolio in biocompatible materials for drug delivery tubing.

- In January 2024, Saint-Gobain launched an antimicrobial tubing line, targeting infection control in hospital settings.

- In October 2025, Trelleborg AB partnered with a major device maker to develop sensor-embedded tubing for real-time monitoring.

Regional Analysis

- North America to dominate the global market

North America leads the medical tubing market, underpinned by sophisticated healthcare infrastructure, substantial R&D investments, and a high burden of chronic diseases that necessitate advanced medical devices. The United States dominates this region, with its robust regulatory framework and innovation ecosystem fostering developments in biocompatible materials, enabling widespread adoption in minimally invasive procedures and supporting both domestic and global supply chains for efficient patient care.

Europe maintains significant influence, driven by stringent quality standards and a focus on sustainable healthcare practices amid aging populations. Germany emerges as the key player, leveraging its engineering prowess and EU harmonized regulations to advance precision tubing manufacturing, promoting eco-friendly innovations that align with environmental goals and enhance procedural safety across clinical applications.

Asia Pacific exhibits rapid expansion, fueled by urbanization, increasing healthcare access, and rising procedural volumes in emerging economies. China stands out as dominant, capitalizing on its manufacturing scale and government initiatives to localize production, addressing domestic demand for affordable tubing while exporting to international markets and tackling pollution-related respiratory issues.

Latin America shows promising growth, supported by improving medical facilities and foreign investments in healthcare. Brazil leads, utilizing its expanding economy and public health reforms to integrate advanced tubing in surgical and diagnostic settings, fostering better outcomes for chronic conditions and bridging gaps in rural healthcare delivery.

The Middle East & Africa region advances progressively, aided by infrastructure projects and international collaborations. South Africa dominates, drawing on its developed medical sector and efforts to combat infectious diseases, implementing high-quality tubing in hospitals and clinics to improve treatment efficacy and position the region in global health advancements.

Competitive Analysis

The global Medical Tubing market is dominated by players:

- Saint-Gobain

- Freudenberg Medical

- Nordson Corporation

- Lubrizol Corporation

- Trelleborg AB

- Asahi Tec Corp.

- MDC Industries

- ZARYS International Group

- Hitachi Cable America Inc.

- NewAge Industries, Inc.

- TE Connectivity

- Spectrum Plastics Group

- ATAG SpA

- And Others.

The global Medical Tubing market is segmented as follows:

By Material

- PVC

- Silicone

- Polyolefins

- Thermoplastics

- Others

By Application

- Bulk Disposable Tubing

- Catheters & Cannulas

- Drug Delivery Systems

- Special Applications

By End-User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Saint-Gobain

- Freudenberg Medical

- Nordson Corporation

- Lubrizol Corporation

- Trelleborg AB

- Asahi Tec Corp.

- MDC Industries

- ZARYS International Group

- Hitachi Cable America Inc.

- NewAge Industries, Inc.

- TE Connectivity

- Spectrum Plastics Group

- ATAG SpA

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors