![]()

Search Market Research Report

Hydrotreated Vegetable Oil (HVO) Market Size, Share Global Analysis Report, 2026-2034

Hydrotreated Vegetable Oil (HVO) Market Size, Share, Growth Analysis Report By Feedstock (Vegetable Oils, Waste and Residue Oils, Animal Fats, and Others), By Application (Transportation, Power Generation, Industrial, and Others), By End-User (Automotive, Aviation, Marine, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

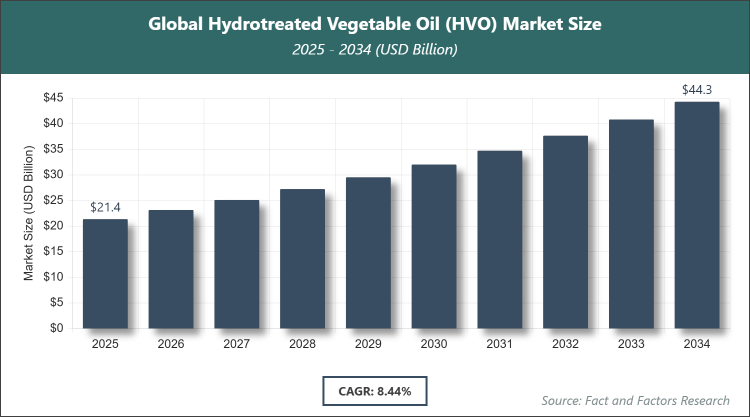

According to Facts & Factors, the global Hydrotreated Vegetable Oil (HVO) market size was estimated at USD 21.36 billion in 2025 and is expected to reach USD 45.00 billion by the end of 2034. The Hydrotreated Vegetable Oil (HVO) industry is anticipated to grow by a CAGR of 8.44% between 2026 and 2034. The Hydrotreated Vegetable Oil (HVO) Market is driven by increasing demand for renewable diesel and supportive government policies promoting low-carbon fuels.

Market Overview

Market Overview

Hydrotreated Vegetable Oil (HVO), also known as renewable diesel, is a sustainable biofuel produced through the hydrotreatment of vegetable oils, animal fats, or other lipid-based feedstocks. This process involves hydrogenation, which removes oxygen and impurities, resulting in a high-quality diesel substitute that is chemically similar to fossil diesel. HVO can be used as a drop-in fuel in existing diesel engines without modifications, offering superior performance characteristics such as a high cetane number, excellent cold-weather properties, and significantly reduced emissions compared to traditional diesel. It serves as an eco-friendly alternative in various sectors, contributing to decarbonization efforts while maintaining compatibility with current infrastructure.

Key Insights

- As per the analysis shared by our research analyst, the global Hydrotreated Vegetable Oil (HVO) market is estimated to grow annually at a CAGR of around 8.44% over the forecast period (2026-2034).

- In terms of revenue, the global Hydrotreated Vegetable Oil (HVO) market size was valued at around USD 21.36 billion in 2025 and is projected to reach USD 45.00 billion by 2034.

- Hydrotreated Vegetable Oil (HVO) market is projected to grow at a significant rate due to increasing demand for renewable diesel as a sustainable alternative to fossil fuels.

- Based on Type segmentation, Pure HVO was predicted to hold maximum market share.

- Based on Application segmentation, Transportation was the leading revenue-generating category in 2025.

- Based on region, Europe was the leading revenue generator in 2025.

Market Dynamics

Growth Drivers

- Increasing Demand for Renewable Diesel

The rising global emphasis on reducing carbon emissions and transitioning to sustainable energy sources has significantly boosted the demand for renewable diesel, including HVO. This fuel offers substantial environmental benefits, such as over 50% reduction in greenhouse gas emissions compared to fossil diesel, making it an attractive option for industries aiming to meet stringent regulatory standards and corporate sustainability goals.

Governments worldwide are implementing policies like biofuel blending mandates and carbon pricing mechanisms, further accelerating HVO adoption. Additionally, its compatibility with existing diesel infrastructure without requiring engine modifications enhances its appeal in transportation and power generation sectors, driving market expansion amid growing awareness of climate change impacts.

Restraints

- High Production Costs

The capital-intensive nature of HVO production, which requires specialized hydrotreating equipment and high-pressure hydrogen, poses a significant barrier to market growth. These costs are notably higher than those for producing biodiesel or ethanol, limiting scalability for smaller producers and potentially hindering widespread adoption in price-sensitive markets.

Feedstock availability and price volatility, particularly for sustainable sources like used cooking oil or animal fats, add to the economic challenges. Competition from cheaper alternatives like fatty acid methyl ester (FAME) biodiesel further restrains HVO's market penetration, especially in regions without strong policy incentives to offset these higher production expenses.

Opportunities

- Expansion in Aviation and Marine Sectors

The aviation industry's push for sustainable aviation fuel (SAF) presents a major opportunity for HVO, as it can be blended up to 50% in jet fuel under international standards. Initiatives like the FAA's Destination 2025 aim to increase renewable jet fuel production, creating new avenues for HVO suppliers to enter this high-value market.

Similarly, the marine sector's adoption of low-sulfur fuels to comply with IMO regulations opens doors for HVO as a cleaner alternative. Technological advancements in co-processing, which allows integration of renewable feedstocks into existing refineries with minimal investment, further enhance opportunities for cost-effective expansion and broader market accessibility.

Challenges

- Feedstock Sustainability Concerns

Environmental issues associated with certain HVO feedstocks, such as palm oil, which can lead to deforestation and biodiversity loss, present ongoing challenges. Regulatory scrutiny and certification requirements for sustainable sourcing increase complexity and costs for producers, potentially limiting supply chains.

Balancing the demand for low-carbon fuels with ethical sourcing practices requires robust traceability systems, which not all market players can implement effectively. Additionally, competition for limited sustainable feedstocks from other biofuel industries could create supply shortages, impacting production volumes and market stability in the long term.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 21.36 Billion |

Projected Market Size in 2034 |

USD 45.00 Billion |

CAGR Growth Rate |

8.44% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Neste (Finland), Valero Energy (U.S.), World Energy (U.S.), Eni (Italy), Cepsa (Spain), Total (France), REG (U.K.), Preem (Sweden), UPM Biofuels (Finland), Repsol (Spain), and Others. |

Key Segment |

By Type, By Application, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Hydrotreated Vegetable Oil (HVO) market is segmented by type, application, and region.

Based on Type Segment, the Hydrotreated Vegetable Oil (HVO) market is divided into Pure HVO, Co-processing, and others. The most dominant segment is Pure HVO, which holds the largest market share due to its superior environmental performance and production from 100% renewable raw materials, resulting in no new CO2 emissions and high compatibility with diesel engines. This dominance drives the market by enabling full substitution of fossil diesel in various applications, supporting global decarbonization efforts. The second most dominant is Co-processing, which allows for efficient integration of up to 10% renewable feedstock in existing refinery units with low capital costs, helping to expand production capacity and meet blending mandates cost-effectively.

Based on Application Segment, the Hydrotreated Vegetable Oil (HVO) market is divided into Transportation, Industrial Power Generators, and others. The most dominant segment is Transportation, accounting for approximately 77.93% share, as HVO serves as a drop-in fuel for diesel vehicles, reducing emissions like CO2, particulate matter, and NOx without engine modifications, thus accelerating adoption in road transport and supporting emission-free mobility goals. This drives the overall market by addressing the largest fuel-consuming sector's sustainability needs. The second most dominant is Industrial Power Generators, with about 18.57% share, due to HVO's high oxygen stability and cleaner combustion, providing a reliable, low-emission alternative for backup power systems in industries, enhancing operational efficiency and compliance with environmental regulations.

Recent Developments

- In December 2022, Cepsa announced an investment of USD 3.15 billion in European green hydrogen projects, aiming to produce 300,000 tons of hydrogen annually for use in refineries, heavy shipping, and haulage, supporting the transition to sustainable fuels including HVO.

- In November 2022, Neste acquired the aggregation business, assets, and used cooking oil collection operations from Crimson Renewable Energy Holdings, LLC in the U.S., strengthening its feedstock supply chain for HVO production.

- In November 2022, Eni revealed plans to construct a third biorefinery at its Livorno site in Italy, featuring a pre-treatment unit, an eco-fining plant with 500,000 tons per year capacity, and a hydrogen production facility from methane gas, expanding HVO output.

- In August 2022, World Energy launched engineering plans to convert its assets into a Sustainable Aviation Fuel (SAF) hub, targeting production of 250 million gallons of SAF annually by 2025, leveraging HVO technology.

- In June 2022, Chevron Corporation completed the acquisition of Renewable Energy Group, Inc., enhancing its renewable fuels capabilities in the U.S. and bolstering HVO production and distribution.

Regional Analysis

- Europe to dominate the global market

Europe holds the dominant position in the global Hydrotreated Vegetable Oil (HVO) market, driven by stringent environmental regulations and ambitious decarbonization targets under the Renewable Energy Directive (RED II). The region's advanced biofuel infrastructure, coupled with increasing blending quotas, fosters rapid adoption across transportation and industrial sectors. Key countries like Finland, with major producers such as Neste, lead in innovation and production capacity, supported by government incentives and a strong focus on sustainable feedstocks. This dominance is further reinforced by collaborative efforts among EU member states to expand biorefineries and reduce reliance on fossil fuels, positioning Europe as a model for global renewable energy transitions.

North America exhibits strong growth in the HVO market, propelled by supportive policies such as the Renewable Fuel Standard and Low Carbon Fuel Standard credits in the U.S. The region's emphasis on reducing greenhouse gas emissions in transportation has led to increased investments in biorefineries and feedstock collection. The United States, as the primary contributor, benefits from abundant waste-based feedstocks and technological advancements in co-processing, enabling seamless integration into existing refinery operations. This strategic approach not only enhances energy security but also aligns with corporate sustainability commitments, driving consistent market expansion.

Asia Pacific is emerging as a significant player in the HVO market, fueled by rapid industrialization and growing awareness of environmental sustainability. Countries like China and India are investing in biofuel technologies to address air quality concerns and reduce import dependence on fossil fuels. Indonesia, a key palm oil producer, dominates regional production by leveraging local resources for HVO manufacturing, supported by national biodiesel mandates. The region's diverse feedstock availability and government initiatives for clean energy transition create opportunities for market growth, though challenges in sustainable sourcing remain crucial for long-term development.

Latin America shows promising potential in the HVO market, driven by abundant agricultural resources and biofuel-friendly policies. Brazil leads the region with its established bioeconomy, utilizing soybean and other oils as feedstocks for HVO production. Government programs promoting renewable fuels in transportation contribute to market expansion, aligning with global sustainability trends. The focus on rural development through biofuel industries further strengthens the sector, positioning Latin America as an exporter of green fuels while addressing domestic energy needs.

The Middle East & Africa region is gradually adopting HVO, primarily in response to global pressure for cleaner energy alternatives. South Africa emerges as a frontrunner, with initiatives to blend biofuels in diesel to reduce emissions. The region's oil-rich economies are diversifying into renewables, leveraging technology transfers for HVO production. Challenges like limited infrastructure are offset by opportunities in aviation fuel, supporting economic diversification and environmental goals.

Competitive Analysis

The global Hydrotreated Vegetable Oil (HVO) market is dominated by players:

- Neste (Finland)

- Valero Energy (U.S.)

- World Energy (U.S.)

- Eni (Italy)

- Cepsa (Spain)

- Total (France)

- REG (U.K.)

- Preem (Sweden)

- UPM Biofuels (Finland)

- Repsol (Spain)

The global Hydrotreated Vegetable Oil (HVO) market is segmented as follows:

By Type

- Pure HVO

- Co-processing

- Others

By Application

- Transportation

- Industrial Power Generators

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Hydrotreated Vegetable Oil (HVO) market is dominated by players:

- Neste (Finland)

- Valero Energy (U.S.)

- World Energy (U.S.)

- Eni (Italy)

- Cepsa (Spain)

- Total (France)

- REG (U.K.)

- Preem (Sweden)

- UPM Biofuels (Finland)

- Repsol (Spain)

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors