![]()

Search Market Research Report

Geosynthetics Market Size, Share Global Analysis Report, 2026-2034

Geosynthetics Market Size, Share, Growth Analysis Report By Product Type (Geotextiles, Geomembranes, Geogrids, Geonets, Geocomposites, and Others), By Application (Waste Management, Water Management, Transportation Infrastructure, Civil Construction, and Others), By End-User (Construction Industry, Water Management, Transportation, Agriculture, Mining, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

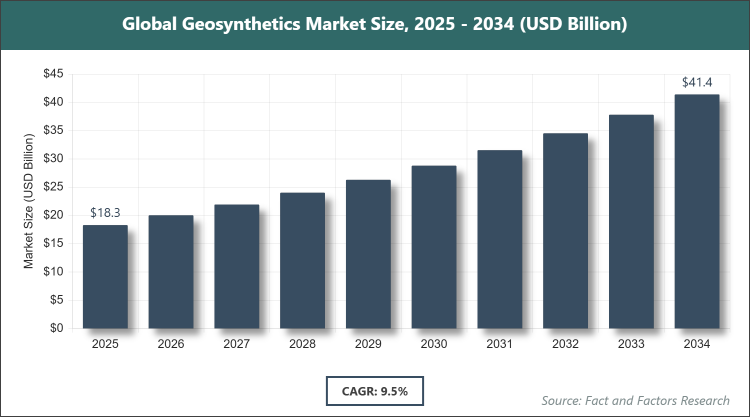

[220+ Pages Report] According to Facts & Factors, the global Geosynthetics market size was estimated at USD 18.3 billion in 2025 and is expected to reach USD 41.4 billion by the end of 2034. The Geosynthetics industry is anticipated to grow by a CAGR of 9.5% between 2026 and 2034. The Geosynthetics Market is driven by increasing demand for sustainable construction materials and infrastructure development.

Market Overview

Market Overview

Geosynthetics refer to synthetic materials used in civil engineering and construction projects to enhance soil stability, provide reinforcement, and facilitate functions such as filtration, drainage, separation, and containment. These materials, typically made from polymers like polyethylene and polypropylene, are engineered to withstand environmental stresses and improve the performance of structures in applications ranging from roadways to landfills.

Key Insights

- As per the analysis shared by our research analyst, the Geosynthetics market is estimated to grow annually at a CAGR of around 9.5% over the forecast period (2026-2034).

- In terms of revenue, the Geosynthetics market size was valued at around USD 18.3 billion in 2025 and is projected to reach USD 41.4 billion by 2034.

- The market is driven by rising infrastructure investments and stringent environmental regulations promoting sustainable construction practices.

- Based on the product type, the Geotextiles segment dominated the market with a share of 49% due to its versatility in filtration, drainage, and soil separation applications across various construction projects.

- Based on the application, the Waste Management segment dominated the market with a share of 25% owing to mandatory landfill liner requirements and increasing focus on environmental protection.

- Based on the end-user, the Construction Industry segment dominated the market with a share of 40% because of extensive use in soil stabilization and reinforcement for buildings and infrastructure.

- Based on the region, Asia Pacific dominated the market with a share of 44% attributed to rapid urbanization and massive government investments in transportation and water management projects.

Growth Drivers

- Increasing Infrastructure Development Worldwide

The surge in global infrastructure projects, including roads, railways, and airports, is a primary driver for the geosynthetics market. These materials offer cost-effective solutions for soil reinforcement and stabilization, reducing construction time and material usage while enhancing durability. Governments in emerging economies are prioritizing large-scale developments to support urbanization, further boosting demand for geosynthetics in civil engineering applications.

Innovations in material technology have led to advanced geosynthetics with improved strength and environmental resistance, making them ideal for challenging terrains. This factor not only expands their application scope but also aligns with sustainable building practices, encouraging adoption across sectors like transportation and water management.

Restraints

- Fluctuating Raw Material Prices

Volatility in the prices of petrochemical-based raw materials, such as polyethylene and polypropylene, poses a significant restraint to market growth. These fluctuations, often influenced by global oil prices and supply chain disruptions, increase production costs and affect pricing stability for end-users. Manufacturers face challenges in maintaining profit margins, which can deter investments in new product development.

Additionally, dependency on fossil fuel-derived polymers raises concerns about long-term sustainability, prompting regulatory scrutiny and potential shifts toward alternative materials. This uncertainty can slow down market expansion, particularly in price-sensitive regions where cost competitiveness is crucial.

Opportunities

- Rising Demand from Mining and Oil & Gas Industries

The mining sector's need for erosion control, tailings management, and heap leach pads presents substantial opportunities for geosynthetics. These materials provide effective containment solutions that minimize environmental impact and comply with stringent regulations. As mining activities expand in regions like Latin America and Africa, the demand for durable geomembranes and geogrids is expected to rise.

In the oil & gas industry, geosynthetics are increasingly used for pipeline protection and secondary containment systems. Technological advancements enabling customization for harsh environments further open avenues for market penetration, fostering partnerships between manufacturers and energy companies.

Challenges

- Lack of Skilled Labor for Installation

Proper installation of geosynthetics requires specialized knowledge and equipment, but a shortage of trained professionals hinders effective deployment. Incorrect installation can lead to project failures, increasing costs and eroding trust in these materials. This challenge is particularly acute in developing regions with limited access to training programs.

Moreover, varying international standards for quality and testing complicate global trade and adoption. Addressing these issues demands investment in education and certification, which could strain resources for smaller market players.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 18.3 Billion |

Projected Market Size in 2034 |

USD 41.4 Billion |

CAGR Growth Rate |

9.5% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Solmax, NAUE GmbH & Co. KG, Officine Maccaferri Spa, Berry Global Inc, AGRU America Inc, Tensar International Corporation, Propex Operating Company LLC, HUESKER Group, GSE Environmental, Koninklijke Ten Cate B.V., and Others. |

Key Segment |

By Product Type, By Application, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Geosynthetics market is segmented by product type, application, end-user, and region.

Based on Product Type Segment, the Geosynthetics market is divided into Geotextiles, Geomembranes, Geogrids, Geonets, Geocomposites, and others.

Geotextiles is the most dominant segment, followed by Geomembranes as the second most dominant. Geotextiles dominate due to their multifunctional properties in separation, filtration, and reinforcement, which drive market growth by enabling efficient soil management in infrastructure projects, reducing erosion, and extending the lifespan of constructions.

Based on Application Segment, the Geosynthetics market is divided into Waste Management, Water Management, Transportation Infrastructure, Civil Construction, and others.

Waste Management is the most dominant segment, followed by Transportation Infrastructure as the second most dominant. Waste Management leads because geosynthetics provide essential barrier systems for landfills, preventing leachate migration and ensuring regulatory compliance, thereby driving the market through enhanced environmental protection and waste containment efficiency.

Based on End-User Segment, the Geosynthetics market is divided into Construction Industry, Water Management, Transportation, Agriculture, Mining, and others.

Construction Industry is the most dominant segment, followed by Transportation as the second most dominant. The Construction Industry dominates as geosynthetics offer cost-effective solutions for foundation stabilization and drainage, propelling market expansion by improving project durability and reducing maintenance needs in building and civil engineering applications.

Recent Developments

- In April 2025, HUESKER acquired Sineco International, expanding its product portfolio with high-quality drainage and dewatering solutions, strengthening its position in the geosynthetics market.

- In January 2025, Officine Maccaferri S.p.A. acquired Synteen Technical Fabrics Inc., enhancing its North American footprint in high-performance geosynthetics.

- In December 2024, Solmax announced plans to centralize nonwoven geotextile production at an advanced facility in the EMEA region, aiming to boost efficiency and innovation.

- In May 2024, Solmax Americas completed a capacity upgrade at its Houston facility, adding new extrusion capabilities to increase geomembrane production.

Regional Analysis

- Asia Pacific to dominate the global market

Asia Pacific stands out as the leading region in the geosynthetics market, driven by extensive infrastructure initiatives and urban expansion. Countries like China and India are investing heavily in transportation networks and water conservation projects, where geosynthetics play a vital role in soil reinforcement and erosion control. The region's focus on sustainable development further amplifies adoption, with governments promoting eco-friendly materials to address environmental concerns. Rapid industrialization enhances demand across sectors, positioning Asia Pacific as a hub for innovation and manufacturing in geosynthetics.

North America maintains a strong presence in the geosynthetics market, supported by advanced regulatory frameworks and mature infrastructure systems. The United States leads with significant investments in waste management and mining, utilizing geosynthetics for containment and stabilization. Emphasis on environmental compliance drives innovation, with companies developing high-performance materials tailored to regional needs. Collaborative efforts between industry and government ensure steady growth, making North America a key player in technological advancements.

Europe's geosynthetics market thrives on stringent environmental regulations and a commitment to sustainable construction. Germany and the United Kingdom dominate, leveraging geosynthetics in coastal protection and landfill applications to mitigate climate impacts. The region's focus on circular economy principles encourages the use of recycled materials, fostering innovation. Ongoing infrastructure upgrades and EU-funded projects bolster demand, solidifying Europe's role in promoting high-quality, eco-conscious solutions.

Latin America is emerging as a promising market for geosynthetics, fueled by mining and agricultural expansions. Brazil leads with applications in soil stabilization for resource extraction and irrigation systems. Increasing awareness of environmental benefits drives adoption, supported by international investments. Challenges like regulatory inconsistencies are being addressed, paving the way for sustained growth in infrastructure and waste management sectors.

The Middle East & Africa region is witnessing gradual adoption of geosynthetics, primarily in water management and oil & gas projects. Saudi Arabia dominates with initiatives for desert reclamation and infrastructure resilience. Growing urbanization and climate adaptation needs propel demand, with international partnerships enhancing technology transfer. The focus on sustainable resource use positions the region for future expansion in geosynthetics applications.

Competitive Analysis

The global Geosynthetics market is dominated by players:

- Solmax

- NAUE GmbH & Co. KG

- Officine Maccaferri Spa

- Berry Global Inc

- AGRU America Inc

- Tensar International Corporation

- Propex Operating Company LLC

- HUESKER Group

- GSE Environmental

- Koninklijke Ten Cate B.V.

The global Geosynthetics market is segmented as follows:

By Product Type

- Geotextiles

- Geomembranes

- Geogrids

- Geonets

- Geocomposites

- Others

By Application

- Waste Management

- Water Management

- Transportation Infrastructure

- Civil Construction

- Others

By End-User

- Construction Industry

- Water Management

- Transportation

- Agriculture

- Mining

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Geosynthetics market is dominated by players:

- Solmax

- NAUE GmbH & Co. KG

- Officine Maccaferri Spa

- Berry Global Inc

- AGRU America Inc

- Tensar International Corporation

- Propex Operating Company LLC

- HUESKER Group

- GSE Environmental

- Koninklijke Ten Cate B.V.

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors