![]()

Search Market Research Report

Fundus Cameras Market Size, Share Global Analysis Report, 2026-2034

Fundus Cameras Market Size, Share, Growth Analysis Report By Product Type (Mydriatic Fundus Cameras, Non-Mydriatic Fundus Cameras, and Others), By Indication (Diabetic Retinopathy, Glaucoma, Age-Related Macular Degeneration, and Others), By End-User (Hospitals, Ophthalmic Clinics, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

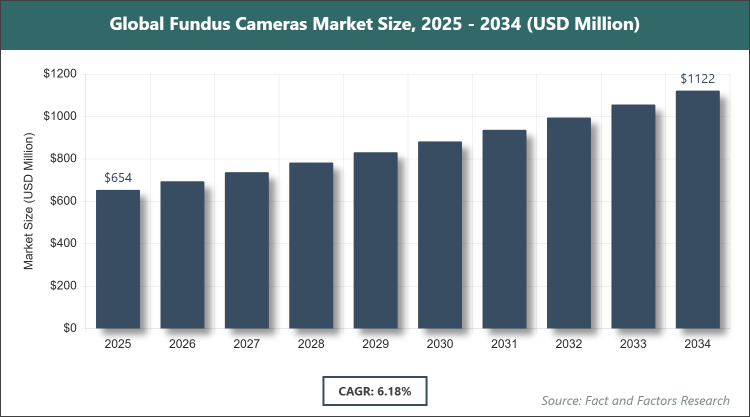

[220+ Pages Report] According to Facts & Factors, the global Fundus Cameras market size was estimated at USD 654.08 million in 2025 and is expected to reach USD 1,116.81 million by the end of 2034. The Fundus Cameras industry is anticipated to grow by a CAGR of 6.18% between 2026 and 2034. The Fundus Cameras Market is driven by the increasing prevalence of ophthalmic disorders and advancements in retinal imaging technologies.

Market Overview

Market Overview

Fundus cameras are specialized medical imaging devices designed to capture high-resolution photographs of the interior surface of the eye, including the retina, optic disc, macula, and posterior pole. These instruments play a crucial role in ophthalmology by enabling non-invasive visualization and documentation of ocular structures, facilitating the early detection, diagnosis, and monitoring of various eye conditions and systemic diseases that manifest in the eye.

Key Insights

- As per the analysis shared by our research analyst, the Fundus Cameras is estimated to grow annually at a CAGR of around 6.18% over the forecast period (2026-2034).

- In terms of revenue, the Fundus Cameras market size was valued at around USD 654.08 million in 2025 and is expected to reach USD 1,116.81 million by 2034.

- The market is driven by the rising incidence of eye diseases linked to aging and chronic conditions like diabetes.

- Based on the Product Type, the Non-Mydriatic segment accounted for the leading share in the market in 2025 (55%) and is anticipated to maintain its dominance over the forecast period. This dominance is attributable to its patient-friendly features, such as no need for pupil dilation, which enhances comfort and efficiency in clinical settings.

- Based on the Indication, the Diabetic Retinopathy segment accounted for the leading share in the market in 2025 (40%) and is anticipated to maintain its dominance over the forecast period. This dominance is attributable to the high global burden of diabetes, which significantly increases the risk of retinal complications requiring regular screening.

- Based on the End-User, the Hospitals segment accounted for the leading share in the market in 2025 (45%) and is anticipated to maintain its dominance over the forecast period. This dominance is attributable to the high volume of patients and the availability of advanced diagnostic infrastructure in hospital environments.

- Based on Region, North America dominated the global Fundus Cameras market in 2025 (36.4%) and is anticipated to maintain its dominance over the forecast period. This dominance is attributable to the region's advanced healthcare systems, high prevalence of diabetic retinopathy, and early adoption of innovative imaging technologies.

Growth Drivers

- Rising Prevalence of Ophthalmic Disorders

The escalating global incidence of eye-related conditions, particularly those associated with an aging population and lifestyle factors, is a primary catalyst for market expansion. Conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration necessitate regular retinal examinations, boosting the demand for reliable imaging solutions in clinical practices worldwide.

Technological advancements in fundus cameras, including integration with artificial intelligence for automated analysis, further enhance diagnostic accuracy and efficiency, encouraging widespread adoption among healthcare providers. This trend is supported by increasing awareness and screening programs aimed at early intervention, ultimately driving sustained market growth.

Restraints

- High Cost of Devices

The substantial initial investment required for acquiring advanced fundus cameras poses a significant barrier, particularly for smaller healthcare facilities and regions with limited budgets. Prices ranging from mid to high figures can deter adoption, leading to uneven market penetration across different economic landscapes.

Additionally, maintenance and operational costs add to the financial burden, potentially slowing down upgrades to newer models even as technology evolves. This restraint is compounded by reimbursement challenges in certain healthcare systems, further limiting accessibility for end-users in resource-constrained settings.

Opportunities

- Expansion in Telemedicine Applications

The growing integration of fundus cameras with remote diagnostic platforms presents a lucrative avenue for market growth, especially in underserved rural and remote areas where access to specialists is limited. Portable and smartphone-compatible models enable real-time image sharing and consultations, expanding the reach of ophthalmic care.

Collaborations between technology firms and healthcare providers to develop affordable, AI-enhanced solutions could further capitalize on this opportunity, fostering innovation and market entry into emerging economies with rising healthcare digitization initiatives.

Challenges

- Shortage of Skilled Professionals

A notable deficit in trained ophthalmologists and technicians capable of operating sophisticated fundus cameras hampers effective utilization, potentially leading to suboptimal diagnostic outcomes. This issue is particularly acute in developing regions where educational and training resources are scarce.

Efforts to address this through comprehensive training programs are essential, yet the projected global shortfall in eye care specialists could exacerbate delays in the adoption and integration of advanced imaging technologies into routine practice.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 654.08 Million |

Projected Market Size in 2034 |

USD 1,116.81 Million |

CAGR Growth Rate |

6.18% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Carl Zeiss Meditech AG, Topcon Corporation, NIDEK Co., Ltd., Haag-Streit Group, CANON MEDICAL SYSTEMS CORPORATION, Kowa Company, Ltd., Optomed, Mediworks, Visionix, and Others. |

Key Segment |

By Product Type, By Indication, By End-User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Fundus Cameras market is segmented by Product Type, Indication, End-User, and region.

Based on Product Type Segment, the Fundus Cameras market is divided into Mydriatic Fundus Cameras, Non-Mydriatic Fundus Cameras, and Others. The most dominant segment is Non-Mydriatic Fundus Cameras, which leads due to its non-invasive nature that eliminates the need for pupil dilation, making it more comfortable for patients and faster for clinicians, thereby increasing its adoption in routine screenings. The second most dominant is Mydriatic Fundus Cameras, valued for providing detailed images in complex cases where dilation allows for comprehensive retinal views, helping to drive the market by catering to specialized diagnostic needs in advanced ophthalmic care.

Based on Indication Segment, the Fundus Cameras market is divided into Diabetic Retinopathy, Glaucoma, Age-Related Macular Degeneration, and Others. The most dominant segment is Diabetic Retinopathy, which dominates owing to the surging global diabetes epidemic that heightens the need for early detection of retinal damage, propelling market growth through increased demand for screening tools. The second most dominant is Glaucoma, essential for monitoring optic nerve health and intraocular pressure effects, contributing to market expansion by supporting preventive care in aging populations prone to this condition.

Based on End-User Segment, the Fundus Cameras market is divided into Hospitals, Ophthalmic Clinics, and Others. The most dominant segment is Hospitals, leading because of their capacity to handle high patient volumes and integrate advanced equipment into multidisciplinary care, driving the market by facilitating large-scale diagnostics. The second most dominant is Ophthalmic Clinics, which grows rapidly due to specialized focus on eye care and the establishment of new facilities, aiding market progression through targeted, efficient service delivery.

Recent Developments

- In December 2024, AVANT Technology partnered with Ainnova Tech to develop an AI-powered fundus camera aimed at early detection of various diseases, enhancing diagnostic capabilities through innovative technology integration.

- In September 2024, Topcon Corporation received FDA 510(k) clearance for its OCTA feature on the robotic Maestro2, marking the first robotic OCT color fundus camera with OCTA in the U.S., improving retinal vascular imaging.

- In March 2023, Remidio Innovative Solutions obtained CE mark approval for its Medios AI, enabling detection of referable diabetic retinopathy using both desktop and smartphone-based fundus cameras, expanding accessibility in screening programs.

- In October 2021, NIDEK launched the Retina Scan Duo2, an advanced OCT/fundus camera system designed for detailed retinal and glaucoma diagnostics, offering enhanced imaging resolution for clinical precision.

- In April 2019, EssilorLuxottica introduced the RETINA800, a non-mydriatic fundus camera focused on screening for retinal pathologies, supporting broader adoption in optometry practices.

Regional Analysis

- North America to dominate the global market

North America leads the market, primarily driven by the United States as the dominating country, where robust healthcare infrastructure and high awareness of eye health facilitate widespread adoption of advanced diagnostic tools. The region's emphasis on research and development, coupled with strong reimbursement policies, supports continuous innovation in ophthalmic devices. Additionally, collaborations between academic institutions and industry players enhance training and technology dissemination, ensuring sustained market leadership through comprehensive eye care networks.

Europe holds a significant position, with Germany and the United Kingdom as key dominating countries, benefiting from a well-established manufacturing base and a large pool of skilled ophthalmologists. The focus on integrating AI in diagnostics across the region promotes efficiency in patient management. Government initiatives for preventive healthcare further bolster demand, creating a stable environment for market growth amid an aging demographic.

Asia Pacific exhibits the fastest growth, led by China and Japan as dominating countries, where rapid urbanization and increasing diabetes awareness drive the need for accessible eye screening solutions. Investments in healthcare infrastructure and portable technologies address rural-urban disparities effectively. Rising disposable incomes and expanding private clinics contribute to broader market penetration in this diverse region.

Latin America shows promising expansion, with Brazil as the dominating country, fueled by rising prevalence of conditions like glaucoma and efforts to improve public health systems. Partnerships with international organizations aid in technology transfer and training programs. The region's focus on affordable diagnostics helps overcome economic barriers, gradually integrating advanced tools into routine care.

The Middle East & Africa region experiences gradual progress, dominated by Saudi Arabia, supported by substantial healthcare investments under national visions for modernization. Efforts to combat eye diseases through awareness campaigns and infrastructure development are key. Collaborations with global firms introduce cutting-edge solutions, though challenges in accessibility persist in remote areas.

Competitive Analysis

The global Fundus Cameras market is dominated by players:

- Carl Zeiss Meditech AG

- Topcon Corporation

- NIDEK Co., Ltd.

- Haag-Streit Group

- CANON MEDICAL SYSTEMS CORPORATION

- Kowa Company, Ltd.

- Optomed

- Mediworks

- Visionix

The global Fundus Cameras market is segmented as follows:

By Product Type

- Mydriatic Fundus Cameras

- Non-Mydriatic Fundus Cameras

- Others

By Indication

- Diabetic Retinopathy

- Glaucoma

- Age-Related Macular Degeneration

- Others

By End-User

- Hospitals

- Ophthalmic Clinics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- Carl Zeiss Meditech AG

- Topcon Corporation

- NIDEK Co., Ltd.

- Haag-Streit Group

- CANON MEDICAL SYSTEMS CORPORATION

- Kowa Company, Ltd.

- Optomed

- Mediworks

- Visionix

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors