![]()

Search Market Research Report

Compression Garments and Stockings Market Size, Share Global Analysis Report, 2026-2034

Compression Garments and Stockings Market Size, Share, Growth Analysis Report By Type (Compression Stockings, Compression Sleeves, Compression Bandages, Compression Socks, and Others), By Application (Varicose Veins, Lymphedema, Deep Vein Thrombosis Prevention, Sports & Athletics, Pregnancy, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Sales, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

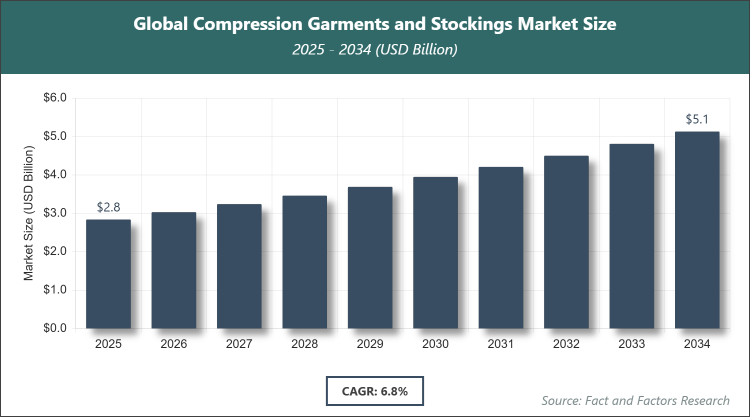

[232+ Pages Report] According to Facts & Factors, the global Compression Garments and Stockings market size was estimated at USD 2.84 billion in 2025 and is expected to reach USD 5.12 billion by the end of 2034. The Compression Garments and Stockings industry is anticipated to grow by a CAGR of 6.8% between 2026 and 2034. The Compression Garments and Stockings Market is driven by the rising prevalence of venous disorders and the growing adoption in sports recovery and preventive healthcare.

Market Overview

Market Overview

The compression garments and stockings market encompasses specialized textile-based medical and performance products engineered to apply graduated pressure to specific body parts, primarily the legs, to improve blood circulation, reduce swelling, alleviate pain, and prevent or manage various vascular and lymphatic conditions. These garments are constructed from elastic fibers such as nylon and spandex, often with silicone bands for secure fit, and are available in different compression levels measured in mmHg to suit therapeutic or athletic needs. The market serves clinical, preventive, and lifestyle applications, emphasizing innovations in breathable fabrics, seamless knitting, and stylish designs to enhance patient compliance while adhering to medical standards for efficacy and safety.

Key Insights

- As per the analysis shared by our research analyst, the global Compression Garments and Stockings market is estimated to grow annually at a CAGR of around 6.8% over the forecast period (2026-2034).

- In terms of revenue, the global Compression Garments and Stockings market size was valued at around USD 2.84 billion in 2025 and is projected to reach USD 5.12 billion, by 2034.

- The Compression Garments and Stockings market is projected to witness significant growth due to increasing awareness of venous health and expanding use in sports and occupational wellness.

- Based on the Type, the Compression Stockings segment accounted for the largest market share of 58% due to its widespread therapeutic use in managing chronic venous insufficiency and lymphedema.

- Based on the Application, the Varicose Veins segment dominated the market with the highest share, owing to high global prevalence and strong clinical evidence supporting compression therapy.

- Based on the Distribution Channel, the Retail Pharmacies segment held the leading position with a substantial share because of easy accessibility and professional guidance for patients.

- Based on the region, the North America region captured around 38% market share, driven by advanced healthcare infrastructure, high awareness, and favorable reimbursement policies.

Growth Drivers

- Increasing Prevalence of Venous Disorders

The global rise in varicose veins, chronic venous insufficiency, and deep vein thrombosis, largely due to sedentary lifestyles, obesity, and aging populations, is significantly boosting demand for compression garments and stockings as a first-line non-invasive treatment. Clinical guidelines from vascular societies increasingly recommend graduated compression as standard care, driving prescription volumes in hospitals and clinics. Improved diagnostic tools and awareness campaigns further accelerate early intervention.

Moreover, the integration of compression therapy into post-surgical recovery protocols enhances outcomes and reduces complications, encouraging healthcare providers to adopt these products routinely. This driver creates sustained demand across both therapeutic and preventive segments, supporting long-term market expansion.

Restraints

- Limited Patient Compliance and Discomfort

Many users discontinue compression therapy due to discomfort, difficulty in donning/doffing, heat retention, and aesthetic concerns, especially with higher compression classes, leading to suboptimal treatment adherence. This issue is particularly pronounced among elderly patients and those with dexterity limitations. Lack of proper fitting and education exacerbates non-compliance.

Additionally, reimbursement restrictions in certain regions limit access to premium or custom-fit products. These factors hinder market penetration, requiring manufacturers to invest in user-friendly designs and awareness programs to improve acceptance rates.

Opportunities

- Growing Demand in Sports and Fitness Recovery

The expanding sports and fitness industry presents significant opportunities as athletes and active individuals increasingly use compression garments for muscle recovery, reduced fatigue, and injury prevention. Endorsements by professional teams and influencers drive consumer adoption. Innovations in moisture-wicking, lightweight fabrics tailored for athletic use broaden appeal.

Furthermore, e-commerce platforms enable direct-to-consumer sales with size guides and educational content. This opportunity allows market players to tap into a younger, health-conscious demographic and diversify beyond traditional medical indications.

Challenges

- Intense Competition and Price Pressure

The presence of numerous local and global manufacturers leads to price competition, particularly in commoditized segments like basic stockings, eroding profit margins. Counterfeit and low-quality products in online channels damage brand trust. Rapid product commoditization limits differentiation opportunities.

In addition, fluctuating raw material costs (elastane, nylon) impact pricing stability. These challenges necessitate strong branding, quality certifications, and innovation in performance features to maintain a competitive advantage.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.84 Billion |

Projected Market Size in 2034 |

USD 5.12 Billion |

CAGR Growth Rate |

6.8% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

SIGVARIS GROUP, medi GmbH & Co. KG, BSN medical (Essity), 3M, medi USA, JOBST, Bauerfeind AG, Thuasne Group, Gloria Med, Salzmann-Group, Cizeta Medicali, Juzo, and Others. |

Key Segment |

By Type, By Application, By Distribution Channel, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Compression Garments and Stockings market is segmented by type, application, distribution channel, and region.

Based on Type Segment, the Compression Garments and Stockings market is divided into Compression Stockings, Compression Sleeves, Compression Bandages, Compression Socks, and others. The most dominant segment is Compression Stockings, which holds the largest share due to their proven efficacy in treating lower limb venous disorders and widespread physician recommendation, driving the market by forming the backbone of clinical compression therapy; the second most dominant is Compression Socks, increasingly popular for everyday wear and sports recovery, contributing to market growth through lifestyle and preventive applications.

Based on Application Segment, the Compression Garments and Stockings market is divided into Varicose Veins, Lymphedema, Deep Vein Thrombosis Prevention, Sports & Athletics, Pregnancy, and others. The most dominant segment is Varicose Veins, commanding the highest share because of its high global prevalence and strong clinical endorsement as primary treatment, which drives the market by ensuring consistent demand from vascular specialists; the second most dominant is Sports & Athletics, gaining rapid traction due to performance and recovery benefits, propelling market expansion in the wellness sector.

Based on Distribution Channel Segment, the Compression Garments and Stockings market is divided into Hospital Pharmacies, Retail Pharmacies, Online Sales, and others. The most dominant segment is Retail Pharmacies, holding the biggest share due to immediate availability, professional fitting advice, and insurance facilitation, driving the market by serving as the primary access point for prescribed products; the second most dominant is Online Sales, growing fastest due to convenience, variety, and home delivery, contributing to market growth through digital transformation.

Recent Developments

- In January 2025, SIGVARIS GROUP launched a new line of fashionable medical compression stockings with improved breathability and silicone grip technology for better patient compliance.

- In October 2024, medi GmbH & Co. KG introduced the mediven® elegance 2.0, featuring enhanced microfiber technology and a wider size range for greater inclusivity.

- In March 2025, BSN medical (Essity) expanded its JOBST® compression portfolio with new flat-knit options specifically designed for advanced lymphedema management.

Regional Analysis

- North America to dominate the global market

North America leads the compression garments and stockings market, with the United States as the dominant country owing to its high prevalence of venous disorders, advanced vascular care infrastructure, and favorable reimbursement policies under Medicare and private insurance for prescribed compression therapy. The region's strong focus on preventive healthcare and sports medicine drives adoption in both clinical and athletic segments. Extensive physician education programs and patient awareness initiatives further support market penetration. The U.S. benefits from a mature distribution network and rapid incorporation of stylish, high-compliance designs.

Europe maintains a very strong position with emphasis on medical-grade quality, led by Germany as the dominant country through its engineering excellence in textile compression products and strict medical device regulations ensuring superior efficacy. The region's aging population and high incidence of chronic venous disease fuel consistent demand. Collaborative research between manufacturers and universities advances material science. Germany's leadership arises from its export-oriented industry and reputation for precision medical textiles.

Asia Pacific is experiencing the fastest growth driven by improving healthcare access and rising lifestyle-related venous issues, with China as the dominant country through its massive population and increasing investment in vascular health awareness programs. Rapid urbanization and sedentary work patterns contribute to higher incidence rates. Domestic manufacturing capabilities support affordable options. China's dominance stems from scale, government healthcare initiatives, and growing middle-class demand for preventive products.

Latin America shows steady progress with increasing diagnosis rates, led by Brazil as the dominant country via expanding private healthcare and growing awareness of compression benefits in obesity-related conditions. Public health campaigns target chronic disease management. Brazil's position strengthens from regional manufacturing presence and rising medical tourism.

The Middle East & Africa region is gradually developing through healthcare modernization, with Saudi Arabia dominating due to Vision 2030 investments in advanced medical care and increasing focus on preventive vascular health among affluent populations. Growing medical infrastructure supports higher adoption. Saudi Arabia's lead comes from economic diversification and import of premium European and American brands.

Competitive Analysis

The global Compression Garments and Stockings market is dominated by players:

- SIGVARIS GROUP

- medi GmbH & Co. KG

- BSN medical (Essity)

- 3M

- medi USA

- JOBST (part of Essity)

- Bauerfeind AG

- Thuasne Group

- Gloria Med

- Salzmann-Group

- Cizeta Medicali

- Juzo

The global Compression Garments and Stockings market is segmented as follows:

By Type

- Compression Stockings

- Compression Sleeves

- Compression Bandages

- Compression Socks

- Others

By Application

- Varicose Veins

- Lymphedema

- Deep Vein Thrombosis Prevention

- Sports & Athletics

- Pregnancy

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Sales

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

- SIGVARIS GROUP

- medi GmbH & Co. KG

- BSN medical (Essity)

- 3M

- medi USA

- JOBST (part of Essity)

- Bauerfeind AG

- Thuasne Group

- Gloria Med

- Salzmann-Group

- Cizeta Medicali

- Juzo

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors