![]()

Search Market Research Report

Cold Chain Market Size, Share Global Analysis Report, 2026-2034

Cold Chain Market Size, Share, Growth Analysis Report By Type (Storage, Transportation, Monitoring Components, and Others), By Temperature Range (Chilled, Frozen), By Application (Fruits & Vegetables, Meat & Seafood, Dairy & Frozen Desserts, Bakery & Confectionery, Pharmaceuticals, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

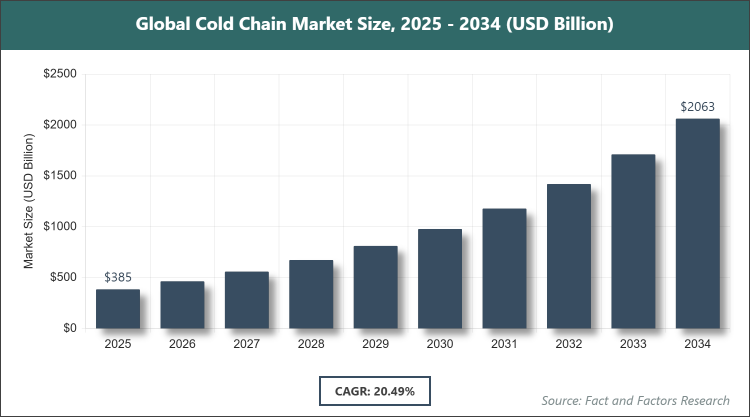

[220 Pages Report] According to Facts & Factors, the global Cold Chain market size was estimated at USD 385.36 billion in 2025 and is expected to reach USD 2063.28 billion by the end of 2034. The Cold Chain industry is anticipated to grow by a CAGR of 20.49% between 2026 and 2034. The Cold Chain Market is driven by increasing demand for perishable goods and advancements in refrigeration technologies.

Market Overview

Market Overview

The cold chain market encompasses the temperature-controlled supply chain infrastructure essential for preserving the quality and safety of perishable products from production to consumption. It involves a seamless network of refrigerated storage, transportation, and monitoring systems designed to maintain specific temperature ranges, preventing spoilage and ensuring product integrity. This market serves critical industries by facilitating the global distribution of temperature-sensitive items without compromising their efficacy or freshness.

Key Insights

- As per the analysis shared by our research analyst, the Cold Chain market is estimated to grow annually at a CAGR of around 20.49% over the forecast period (2026-2034).

- In terms of revenue, the Cold Chain market size was valued at around USD 385.36 billion in 2025 and is projected to reach USD 2063.28 billion by 2034.

- The Cold Chain market is driven by rising global demand for fresh food products, pharmaceuticals, and biologics requiring stringent temperature control.

- Based on the Type, the Storage segment held the largest market share of 55% in 2025.

- This dominance is attributed to substantial investments in refrigerated warehouses and facilities that provide scalable capacity for long-term preservation of perishable goods.

- Based on the Temperature Range, the Frozen segment held the largest market share of 60% in 2025.

- This dominance is attributed to the need for extended shelf life in products like meat, seafood, and frozen foods, which require sub-zero temperatures to prevent bacterial growth.

- Based on the Application, the Meat & Seafood segment held the largest market share of 28% in 2025.

- This dominance is attributed to the high perishability and global trade volume of these protein-rich products, necessitating robust cold chain infrastructure to maintain freshness and safety.

- North America dominated the market with the largest market share of 34% in 2025.

- This regional dominance is attributed to advanced logistics networks, stringent regulatory standards, and high consumption of perishable goods in the food and pharmaceutical sectors.

Market Dynamics

Growth Drivers

- Increasing Demand for Perishable Food Products

The surge in consumer preference for fresh and frozen foods, driven by urbanization and changing lifestyles, has amplified the need for efficient cold chain systems. This demand is particularly evident in emerging economies where rising disposable incomes enable greater access to diverse food options, pushing companies to expand their refrigerated supply chains.

Furthermore, global trade in perishable commodities like fruits, vegetables, and dairy has intensified, requiring reliable temperature-controlled logistics to minimize waste and ensure quality during long-distance transportation. Technological integrations, such as IoT-enabled monitoring, further enhance efficiency, reducing spoilage rates and supporting sustainable practices in food distribution.

- Rising Pharmaceutical and Vaccine Distribution Needs

The pharmaceutical industry's growth, especially for biologics and vaccines that require precise temperature control, has propelled the cold chain market forward. Events like global health crises have highlighted the criticality of maintaining cold chains for vaccine efficacy, leading to increased investments in specialized storage and transport solutions.

Advancements in healthcare, including the development of temperature-sensitive therapies, demand end-to-end visibility and compliance with regulatory standards, fostering innovation in cold chain technologies. This driver not only boosts market revenue but also encourages collaborations between logistics providers and pharma companies to optimize supply chain resilience.

- Technological Advancements in Refrigeration and Monitoring

Innovations such as AI-driven predictive analytics and real-time tracking systems have revolutionized cold chain operations by improving accuracy and reducing energy consumption. These technologies enable proactive issue resolution, minimizing disruptions and enhancing overall supply chain efficiency.

The adoption of sustainable refrigerants and energy-efficient equipment aligns with environmental regulations, attracting investments from eco-conscious stakeholders. As a result, these advancements lower operational costs and expand market accessibility, particularly for small-scale operators in developing regions.

Restraints

- High Initial and Operational Costs

The substantial capital required for establishing refrigerated infrastructure, including warehouses and vehicles, poses a significant barrier, especially for small and medium enterprises. Maintenance and energy expenses further escalate costs, limiting market entry and expansion in price-sensitive regions.

Additionally, fluctuating energy prices and the need for specialized training add to the financial burden, potentially slowing adoption rates. This restraint impacts profitability and may lead to consolidation among larger players who can afford economies of scale.

- Stringent Regulatory Compliance Requirements

Complex global regulations governing temperature control and product safety demand continuous monitoring and documentation, increasing administrative overheads. Non-compliance can result in severe penalties and product recalls, deterring investment in certain markets.

Variations in standards across countries complicate international trade, requiring adaptable systems that raise implementation challenges. This restraint underscores the need for standardized protocols to facilitate smoother market growth.

Opportunities

- Expansion in Emerging Markets

Rapid economic growth in Asia-Pacific and Latin America presents untapped potential for cold chain infrastructure development, driven by increasing urbanization and food demand. Investments in these regions can capitalize on government initiatives for food security and healthcare improvements.

Partnerships with local players can accelerate market penetration, leveraging regional expertise to build resilient supply chains. This opportunity promises high returns as consumer bases expand and e-commerce grows.

- Adoption of Sustainable and Green Technologies

The shift toward eco-friendly practices opens avenues for innovation in low-emission refrigeration and recyclable packaging. Companies investing in green technologies can differentiate themselves, appealing to environmentally aware consumers and regulators.

Government incentives for sustainable initiatives further encourage adoption, potentially reducing long-term costs through energy savings. This opportunity aligns market growth with global sustainability goals, fostering long-term viability.

- Growth in E-Commerce and Online Grocery Delivery

The boom in online shopping for perishable goods necessitates advanced last-mile cold chain solutions, creating demand for compact, efficient delivery systems. Integrating digital platforms with logistics enhances customer satisfaction and operational agility.

This trend supports market expansion by diversifying applications beyond traditional sectors, tapping into consumer convenience preferences.

Challenges

- Infrastructure Gaps in Developing Regions

Inadequate road networks and power supply in emerging markets hinder efficient cold chain operations, leading to higher spoilage rates and inefficiencies. Addressing these requires significant public-private investments, which may be slow to materialize.

Cultural and logistical barriers further complicate implementation, necessitating tailored strategies for regional adaptation. This challenge threatens equitable market growth and requires innovative, off-grid solutions.

- Supply Chain Disruptions and Geopolitical Risks

Global events like pandemics or trade conflicts can interrupt cold chain flows, affecting product availability and costs. Volatility in fuel prices and labor shortages exacerbate these issues, demanding robust contingency planning.

Building resilient systems through diversification and technology is essential, but implementation varies by region. This challenge highlights the need for agile strategies to maintain market stability.

- Climate Change and Environmental Impacts

Rising temperatures and extreme weather events pose risks to cold chain integrity, increasing energy demands for cooling. Environmental concerns over refrigerant emissions push for transitions to greener alternatives, which may involve high retrofit costs.

Adapting to these changes requires ongoing research and policy alignment, balancing ecological and economic considerations. This challenge underscores the industry's role in broader climate mitigation efforts.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 385.36 Billion |

Projected Market Size in 2034 |

USD 2063.28 Billion |

CAGR Growth Rate |

20.49% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Americold Logistics, Lineage Logistics Holding LLC, Nichirei Corporation, Burris Logistics, Agro Merchants Group, Kloosterboer, United States Cold Storage, Tippmann Group, VersaCold Logistics Services, Congebec Inc, and Others. |

Key Segment |

By Type (Storage, Transportation, Monitoring Components, and Others), By Temperature Range (Chilled, Frozen), By Application (Fruits & Vegetables, Meat & Seafood, Dairy & Frozen Desserts, Bakery & Confectionery, Pharmaceuticals, and Others), and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Cold Chain market is segmented by type, temperature range, application, and region.

Based on Type Segment,the Cold Chain market is divided into Storage, Transportation, Monitoring Components, and others.

The most dominant segment is Storage, which commands the largest share due to its foundational role in preserving large volumes of perishable goods over extended periods, enabling efficient inventory management and reducing waste; the second most dominant is Transportation, which supports global distribution by ensuring temperature integrity during transit, driving market growth through expanded trade capabilities and just-in-time delivery models.

Based on Temperature Range Segment, the Cold Chain market is divided into Chilled, Frozen.

The most dominant segment is Frozen, leading because it caters to products requiring long-term preservation like meat and seafood, minimizing spoilage and extending shelf life to meet global demand; the second most dominant is Chilled, which facilitates the handling of fresh produce and dairy, contributing to market expansion by supporting shorter supply chains and consumer preferences for minimally processed foods.

Based on Application Segment, the Cold Chain market is divided into Fruits & Vegetables, Meat & Seafood, Dairy & Frozen Desserts, Bakery & Confectionery, Pharmaceuticals, and others.

The most dominant segment is Meat & Seafood, prevailing owing to its high susceptibility to contamination and the necessity for stringent temperature control to ensure safety and quality in international exports; the second most dominant is Pharmaceuticals, which bolsters market growth by addressing the critical need for maintaining drug efficacy, especially for vaccines and biologics in healthcare distribution.

Recent Developments

- In August 2025, Americold announced the opening of a 335,000-square-foot import-export hub in Kansas City, Missouri, in partnership with Canadian Pacific Kansas City railroad, enhancing connectivity for temperature-controlled goods across North America.

- In November 2024, Lineage acquired Coldpoint's assets, a Kansas City-based provider of cold storage and transportation solutions, expanding its network and capabilities in the Midwest region.

- In October 2025, Carrier Transicold showcased new container-refrigeration technologies at Intermodal Europe, focusing on efficiency, sustainability, and reliability for global shipping.

- In July 2025, Geotab upgraded its Cold Chain solution with new hardware and software, providing greater visibility, control, and compliance for temperature-sensitive shipments.

Regional Analysis

- North America to dominate the global market

North America leads the cold chain market due to its sophisticated infrastructure and high-tech logistics systems that support seamless distribution of perishable goods. The region's dominance stems from robust investments in automated warehouses and advanced monitoring technologies, ensuring compliance with strict food safety regulations. The United States, as the dominating country, drives this through its vast consumer market and extensive pharmaceutical industry, where temperature-controlled supply chains are critical for vaccine and biologic distribution. Innovations in sustainable refrigeration further strengthen the area's position, fostering efficiency and reducing environmental impact. Overall, North America's integrated network of highways, ports, and air cargo facilities enables rapid and reliable delivery, catering to diverse industries from agriculture to healthcare.

Europe maintains a strong presence in the cold chain market, characterized by stringent environmental and quality standards that promote innovative solutions. The region's focus on sustainability has led to widespread adoption of eco-friendly refrigerants and energy-efficient systems. Germany, the dominating country, excels through its engineering prowess and central location, facilitating efficient cross-border trade within the EU. Emphasis on traceability and real-time data analytics enhances supply chain transparency, crucial for perishable exports like dairy and confectionery. Europe's collaborative approach, involving public-private partnerships, supports continuous improvement in logistics, addressing challenges like urban congestion and climate variability.

Asia Pacific emerges as a high-growth area in the cold chain market, fueled by rapid urbanization and expanding middle-class populations demanding fresh imports. Investments in infrastructure, such as new refrigerated facilities and transportation hubs, are accelerating to meet rising needs. China, the dominating country, propels this through massive scale operations and government initiatives for food security, integrating advanced IoT for monitoring. The region's diverse climates necessitate adaptable technologies, driving innovation in portable cooling solutions. E-commerce growth further amplifies demand, creating opportunities for last-mile delivery enhancements across densely populated areas.

Latin America shows promising development in the cold chain market, supported by abundant agricultural resources and increasing exports of fruits and seafood. Efforts to modernize logistics are underway, with improvements in road and port infrastructure to reduce transit times. Brazil, the dominating country, leads with its agribusiness strength, implementing cold storage expansions to preserve harvest quality for global markets. Regional collaborations aim to standardize practices, overcoming hurdles like energy instability. The focus on sustainable practices aligns with international demands, positioning the area for expanded trade partnerships.

The Middle East & Africa region is gradually advancing in the cold chain market, driven by import dependencies and emerging healthcare needs. Investments in solar-powered refrigeration address power challenges, enhancing reliability in arid environments. South Africa, the dominating country, stands out with its developed ports and focus on fruit exports, utilizing cold chains to maintain competitiveness. Initiatives for skill development and technology transfer are key to building capacity. The area's strategic location supports transit roles in global supply chains, with potential for growth in pharmaceutical distribution amid health initiatives.

Competitive Analysis

The global Cold Chain market is dominated by players:

- Americold Logistics

- Lineage Logistics Holding LLC

- Nichirei Corporation

- Burris Logistics

- Agro Merchants Group

- Kloosterboer

- United States Cold Storage

- Tippmann Group

- VersaCold Logistics Services

- Congebec Inc

- And Others

The global Cold Chain market is segmented as follows:

By Type

- Storage

- Transportation

- Monitoring Components

- Others

By Temperature Range

- Chilled

- Frozen

By Application

- Fruits & Vegetables

- Meat & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Pharmaceuticals

- Others

By Regional Segment Analysis

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Cold Chain market is dominated by players:

- Americold Logistics

- Lineage Logistics Holding LLC

- Nichirei Corporation

- Burris Logistics

- Agro Merchants Group

- Kloosterboer

- United States Cold Storage

- Tippmann Group

- VersaCold Logistics Services

- Congebec Inc

- And Others

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors