![]()

Search Market Research Report

Breast Implants Market Size, Share Global Analysis Report, 2026-2034

Breast Implants Market Size, Share, Growth Analysis Report By Type (Silicone Implants, Saline Implants, and Others), By Shape (Round, Anatomical, and Others), By Application (Cosmetic Surgery, Reconstructive Surgery, and Others), By End User (Hospitals, Cosmetology Clinics, and Others), and By Region - Global Industry Insights, Overview, Comprehensive Analysis, Trends, Statistical Research, Market Intelligence, Historical Data and Forecast 2026-2034

Industry Insights

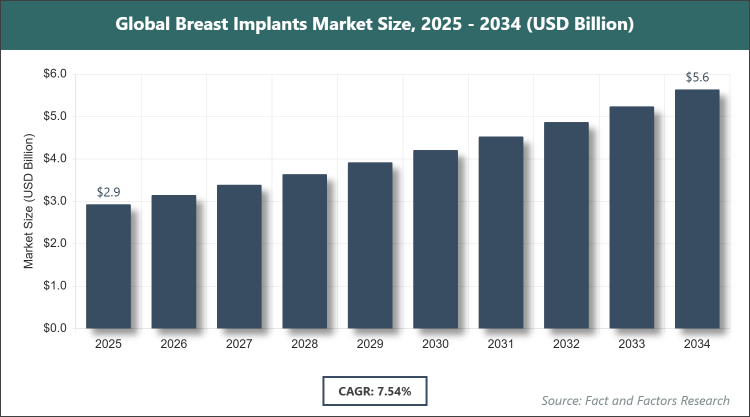

[225 Pages Report] According to Facts & Factors, the global breast implants market size was estimated at USD 2.93 billion in 2025 and is expected to reach USD 5.62 billion by the end of 2034. The Breast Implants industry is anticipated to grow by a CAGR of 7.54% between 2026 and 2034. The Breast Implants Market is driven by rising demand for cosmetic surgeries and increasing breast cancer incidences.

Market Overview

Market Overview

The breast implants market involves the production, distribution, and utilization of medical devices designed to enhance or reconstruct breast shape and size, typically using silicone or saline-filled prosthetics implanted surgically for cosmetic augmentation or post-mastectomy restoration, addressing aesthetic preferences and medical needs while incorporating advancements in biocompatible materials to improve safety and natural appearance. This market engages stakeholders such as plastic surgeons, hospitals, clinics, and manufacturers focused on innovation to meet diverse patient requirements across global healthcare systems, emphasizing regulatory compliance and patient outcomes in both elective and reconstructive procedures.

Key Insights

- As per the analysis shared by our research analyst, the Breast Implants market is expected to grow at a CAGR of 7.54% during the forecast period of 2026-2034.

- In terms of revenue, the Breast Implants market size was valued at about USD 2.93 billion in 2025 and is expected to reach USD 5.62 billion by 2034.

- The Breast Implants market is driven by rising demand for cosmetic surgeries and increasing breast cancer incidences.

- Based on the type, the silicone implants segment dominated the market with a share of 83% in 2025 due to their natural feel and lower rupture risk compared to alternatives.

- Based on the shape, the round segment dominated the market with a share of 80% in 2025, owing to its versatility in providing a fuller upper breast appearance preferred in cosmetic procedures.

- Based on the application, the cosmetic surgery segment dominated the market with a share of 74% in 2025 as it caters to aesthetic enhancements driven by body image trends.

- Based on the end user, the hospitals segment dominated the market with a share of 55% in 2025 given their role in complex reconstructive surgeries post-cancer.

- North America dominated the market with a share of 35% in 2025 due to high cosmetic procedure rates and advanced healthcare infrastructure supporting reconstructions.

Growth Drivers

- Rising Demand for Cosmetic Surgeries

The increasing focus on aesthetic enhancement and body positivity is fueling demand for breast implants, as more individuals seek procedures to improve self-confidence and appearance, supported by social media influence and celebrity endorsements that normalize cosmetic interventions. This trend is particularly strong among younger demographics prioritizing personalized beauty standards.

Additionally, advancements in surgical techniques and implant designs reduce recovery times and risks, making procedures more accessible and appealing, thereby expanding the market through greater patient acceptance and repeat consultations.

- Increasing Breast Cancer Incidences

The growing prevalence of breast cancer globally necessitates reconstructive surgeries, driving implant demand as patients opt for restoration post-mastectomy to regain normalcy and psychological well-being. This is amplified by awareness campaigns and improved screening leading to earlier detections.

Furthermore, insurance coverage for reconstructions in many regions encourages uptake, fostering collaborations between oncologists and plastic surgeons to integrate implants into comprehensive cancer care plans, sustaining market growth.

- Technological Advancements in Implants

Innovations such as cohesive gel and textured surfaces enhance safety and natural outcomes, attracting patients with concerns over traditional options. These developments include biocompatible materials reducing complications like capsular contracture.

Moreover, regulatory approvals for new formulations boost confidence, enabling manufacturers to differentiate products and capture premium segments, contributing to overall market expansion through R&D investments.

Restraints

- Health Risks and Complications

Potential issues like implant rupture, infection, and capsular contracture deter patients, leading to hesitation and preference for non-invasive alternatives. This is heightened by media coverage of adverse events.

Regulatory warnings and recalls further erode trust, requiring extensive patient education and safety protocols to mitigate impacts on market adoption.

- High Procedure Costs

The expense of surgery and implants limits accessibility, particularly in emerging markets where out-of-pocket payments dominate. This restraint affects lower-income groups seeking cosmetic enhancements.

Economic fluctuations exacerbate this, prompting delays in elective procedures and necessitating financing options or cost reductions to broaden market reach.

Opportunities

- Emerging Markets Expansion

Rising disposable incomes in Asia and Latin America present growth avenues, as urbanization and western beauty influences drive cosmetic procedure adoption. This includes medical tourism hubs offering affordable surgeries.

Capitalizing on this involves local manufacturing and partnerships to navigate regulations, unlocking new revenue streams in underserved regions.

- Innovative Product Developments

The introduction of customizable and bioengineered implants offers differentiation, appealing to patients desiring personalized solutions with minimal risks. This focuses on ergonomic designs and fat grafting hybrids.

Such innovations attract investments, fostering collaborations with tech firms for smart monitoring features, enhancing market competitiveness.

Challenges

- Stringent Regulatory Approvals

Complex FDA and international standards delay product launches, increasing development costs and timelines for manufacturers. This includes rigorous clinical trials for safety validation.

Adapting to varying global regulations demands compliance expertise, potentially hindering small players' market entry.

- Public Perception and Stigma

Societal judgments around cosmetic surgery can limit demand, especially in conservative cultures where natural beauty is prioritized. This affects marketing strategies.

Overcoming this requires awareness initiatives emphasizing psychological benefits and safety, gradually shifting perceptions for broader acceptance.

Report Scope

Report Attribute |

Details |

Market Size 2025 |

USD 2.93 Billion |

Projected Market Size in 2034 |

USD 5.62 Billion |

CAGR Growth Rate |

7.54% CAGR |

Base Year |

2025 |

Forecast Years |

2026-2034 |

Key Market Players |

Allergan, Mentor Worldwide LLC, Sientra Inc., Establishment Labs S.A., GC Aesthetics, POLYTECH Health & Aesthetics GmbH, HansBiomed Co. Ltd., Groupe Sebbin SAS, Laboratoires Arion, Silimed, and Others. |

Key Segment |

By Type, By Shape, By Application, By End User, and By Region |

Major Regions Covered |

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Purchase Options |

Request customized purchase options to meet your research needs. Explore purchase options |

Market Segmentation

The Breast Implants market is segmented by type, shape, application, end-user, and region.

Based on Type Segment, the breast implants market is divided into silicone implants, saline implants, and others. The most dominant segment is silicone implants, leading due to their realistic texture and durability that mimic natural breast tissue, driving the market by satisfying patient preferences for aesthetic outcomes in both cosmetic and reconstructive procedures thus boosting surgeon recommendations and overall adoption; the second most dominant is saline implants, favored for their adjustable volume during surgery and perceived safety in case of rupture, contributing to market growth by offering cost-effective options in regions with budget constraints and supporting diverse surgical needs.

Based on Shape Segment, the breast implants market is divided into round, anatomical, and others. The most dominant segment is round, commanding the market because of its ability to provide enhanced cleavage and fullness preferred in augmentation, propelling growth through high demand in cosmetic applications where symmetry is key; the second most dominant is anatomical, chosen for its teardrop shape offering natural contours in reconstruction, aiding market expansion by addressing post-mastectomy needs and improving patient satisfaction in therapeutic settings.

Based on Application Segment, the breast implants market is divided into cosmetic surgery, reconstructive surgery, and others. The most dominant segment is cosmetic surgery, dominating owing to rising aesthetic trends and social influences encouraging enhancements, driving the market via increased elective procedures and innovative marketing; the second most dominant is reconstructive surgery, essential for cancer survivors seeking restoration, supporting growth through medical necessities and insurance reimbursements.

Based on End User Segment, the breast implants market is divided into hospitals, cosmetology clinics, and others. The most dominant segment is hospitals, leading as they handle complex cases, including reconstructions, boosting the market with integrated care and advanced facilities; the second most dominant is cosmetology clinics, facilitating outpatient augmentations, contributing to expansion via specialized aesthetic services and patient convenience.

Recent Developments

- In September 2024, Establishment Labs Holdings Inc. received FDA approval for Motiva SmoothSilk Ergonomix and Round breast implants, expanding options for augmentation and revision surgeries.

- In May 2025, Johnson & Johnson MedTech launched MENTOR MemoryGel Enhance Breast Implants, designed for post-mastectomy reconstruction with improved aesthetics and comfort.

- In October 2023, GC Aesthetics partnered with Bimini Health Tech to enhance global breast reconstruction offerings through innovative implant technologies.

- In January 2023, CollPlant Biotechnologies Ltd. collaborated with Stratasys to develop regenerative breast implants using rhCollagen-based BioInks and 3D printing.

Regional Analysis

- North America to dominate the global market

North America leads the breast implants market with the United States as the dominating country, where high disposable incomes and cultural emphasis on aesthetics drive cosmetic procedures, supported by advanced surgical infrastructure and insurance for reconstructions, while leading manufacturers innovate to meet FDA standards, fostering a robust ecosystem that caters to diverse patient demographics seeking enhancement or restoration.

Europe follows with Germany dominating, benefiting from a strong focus on medical tourism and regulated cosmetic practices that ensure safety, integrated with public health systems covering reconstructions, while growing awareness of body positivity encourages procedures, backed by skilled surgeons and research in implant materials enhancing regional market stability.

Asia Pacific is expanding rapidly, led by China due to rising urbanization and western beauty influences boosting demand for augmentations, aided by affordable medical tourism and local production reducing costs, while increasing breast cancer awareness promotes reconstructions, creating opportunities in a youthful population eager for aesthetic improvements.

Latin America shows growth with Brazil at the forefront, known for its vibrant cosmetic surgery culture and high procedure volumes, where accessible clinics and skilled professionals attract international patients, supported by economic growth enabling more elective surgeries focused on body contouring.

The Middle East & Africa region progresses with South Africa leading, emphasizing reconstructive needs amid health initiatives, while urban centers adopt cosmetic trends, aided by investments in healthcare facilities that improve access to safe implants for diverse socio-economic groups.

Competitive Analysis

The global Breast Implants market is dominated by players:

- Allergan

- Mentor Worldwide LLC

- Sientra Inc.

- Establishment Labs S.A.

- GC Aesthetics

- POLYTECH Health & Aesthetics GmbH

- HansBiomed Co. Ltd.

- Groupe Sebbin SAS

- Laboratoires Arion

- Silimed

The global Breast Implants market is segmented as follows:

By Type

- Silicone Implants

- Saline Implants

- Others

By Shape

- Round

- Anatomical

- Others

By Application

- Cosmetic Surgery

- Reconstructive Surgery

- Others

By End User

- Hospitals

- Cosmetology Clinics

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Industry Major Market Players

The global Breast Implants market is dominated by players:

Allergan

Mentor Worldwide LLC

Sientra Inc.

Establishment Labs S.A.

GC Aesthetics

POLYTECH Health & Aesthetics GmbH

HansBiomed Co. Ltd.

Groupe Sebbin SAS

Laboratoires Arion

Silimed

Copyright © 2025 - 2026, All Rights Reserved, Facts and Factors